By Abraham Finberg, Simon Menkes, Rachel Wright No Comments

Although Rhode Island is the USA’s smallest state, it has traditionally taken an out-sized dislike for cannabis and its users. It first banned cannabis in 1918 and, up until recently, had some of the strictest mandatory minimum sentences for large-scale possession, sentencing those with more than 5 kg (11 lbs) to 20 years’ imprisonment and fines of between $25,000 and $100,000.

Rhode Island’s Change of Heart

These days, however, the Ocean State has turned over a new leaf. It legalized medical cannabis in 2006, and on May 25, 2022, legalized adult use sales as well. Starting in December 2022, Rhode Island residents could purchase cannabis from five of the six medical cannabis dispensaries across the state which have also been approved to sell to adults.

Over the course of 2023, the state is expected to issue licenses for an additional 28 dispensaries, including a portion reserved for social equity applicants and worker-owned cooperatives. At the same time, 33 cities and towns across Rhode Island voted to determine whether cannabis businesses would be allowed in their jurisdiction. 25 of these municipalities ended up approving these measures.

Social Equity

Like many retail-legal states, Rhode Island has enacted social equity support for cannabis licensees. The state is divided into six retail license zones, and within each zone, one retail license will be reserved for a social equity applicant and one for a worker-owned cooperative. In addition, the state’s cannabis legislation provides for a $1 million fund to help support the social equity license recipients. Funded by all fees collected from adult-use cannabis businesses, this assistance fund will provide grants, promote job training and workforce development, and administer programming for restorative justice. The legislation also establishes a process whereby individuals may have their misdemeanor or felony convictions for cannabis possession expunged.

How Tax-Friendly Toward Cannabis is Rhode Island?

The Ocean State still has a way to go to be considered a truly cannabis-friendly state. For one thing, the state is forcing both individuals and corporations to conform to Internal Revenue Code section 280E which disallows deductions and credits for expenditures connected with trafficking in controlled substances under the Controlled Substances Act, schedule 1 or 2. This means cannabis companies will only be permitted to reduce their sales by cost of goods sold when determining their taxable income on their state tax returns unless they decide to take more aggressive tax positions. For example, with a conservative IRC 280E tax position, a cannabis dispensary would only be allowed to deduct the cost of the product purchased and the cost to transport the product to the dispensary, while disallowing such significant expenses as rent and payroll. All cannabis businesses must forgo expense deductions related to selling, general and administrative expenses, as they are disallowed under the tax code under this traditional method. Rhode Island has also disallowed cannabis businesses from taking an R&D tax credit as a result of conformity with federal tax law.

In addition, Rhode Island is requiring retailers to collect 10% state cannabis excise tax plus 3% local cannabis excise tax from its customers, along with the standard 7% sales tax. Good news: sales tax is not calculated on the excise tax collected (unlike California, which does impose tax-on-tax). Medical sales are subject to sales tax but not to excise tax, and excise tax is not charged on cannabis accessories. Excise tax, like sales tax, must be remitted to the state by the dispensary on or before the 20th of the following month.

In Summary

Rhode Island has taken a big step forward from its anti-cannabis past by legalizing adult use sales and by supporting equity applicants as well as the expungement of past criminal convictions for many of those victimized by the war on cannabis. While Rhode Island’s excise taxes are not the worst we’ve seen, the state’s support of 280E will make it a lot harder for cannabis businesses to thrive.

Have you ever been to the DMV, only to be turned away because you didn’t have the countless forms of identification needed? Sometimes it feels like no amount of ID or proof of residence is enough, whether it’s your 2nd grade report card or an electric bill from 25 years ago.

That feeling is what it’s like for anyone working in compliance; regardless of industry. Banks are no different. They need to possess compliance documents such as Consolidated Reports of Condition and Income and other Federal Financial Institutions Examination Council (FFIEC) reports that work like the laundry list of documents you need to get a driver’s license or get your car registered.

The same can be said for newly licensed and legal cannabis companies. They often need state and local inspection documents, federal background checks and a list of other documents that make a CVS receipt look minuscule in comparison.

Historically, across all industries, the whole process of gathering and providing these sorts of documents can turn into a bit of a charade. Many companies do the bare minimum to check the compliance box and achieve certifications. Various teams and stakeholders try to skate through the compliance process by providing answers that reflect what they think the enterprise customer wants to see (vs. the reality).

In order to achieve long term growth, financial institutions (FIs) and cannabis companies alike need to start executing compliance plans. FIs are always seeking new growth and revenue opportunities, and cannabis companies are constantly under the scrutiny of regulators. Identifying new solutions that can help companies grow quickly while also maintaining compliance should be an essential part of the roadmap.

Financial Institutions and Cannabis

Many think that financial institutions and cannabis businesses would be on opposite ends of any spectrum. Banking is a mature and established industry, while legal cannabis is a new, fast moving and constantly evolving space. So, on one side, there is a risk averse fiscally conservative and traditional business model, and on the other side is an industry that is outside of the mainstream.

Let’s look at this perception from a different angle though. What is true is that both industries are highly regulated and must comply with the rules placed upon them by regulators; and if their house isn’t in order, the consequences can be disastrous (Read: Massive fines or even losing the ability to operate). CRBs and FIs deal with the security and dual control of inventory, and making sure customers are properly identified and of legal capacity to conduct business. In most cases, both are small businesses within their respective communities.

Moreover, each of the industries are forced to navigate nearly-constant regulatory change, making the act of complying with applicable regulations a moving target. For most of these types of businesses, regulatory compliance is cited as one of the largest (and most expensive) challenges they face in day-to-day operations.

Compliance as Revenue Protection

When financial institutions make the decision to offer services to the cannabis industry, they naturally look at the market opportunity to determine whether the effort associated with the increased compliance obligations outweigh the potential benefits. Traditionally, compliance is viewed as a cost center, but in reality, it’s a revenue protection center. As the old saying goes; “an ounce of prevention is worth more than a pound of cure.” Compliance is that prevention.

Cannabis companies need to demonstrate reliability and a history of compliance in order to attract investors and accumulate capital

Failing to fully comply and meet regulatory compliance standards can cost organizations billions. Having a trusted system of compliance established should not be looked at as a cost-sucking measure for businesses, when it really is negligible when the cost of getting it wrong is far more substantial. Setting up a truthful and transparent compliance program isn’t just the right thing to do, it also protects revenue.

As the cannabis industry continues to grow, navigating around pain points is becoming increasingly expensive for the companies participating in it, many of whom are still struggling to turn a profit. Specifically, an IDC forecast shows global revenue from GRC solutions growing from $11.3 billion in 2020 to nearly $16.2 billion by 2025. And the average business hires and spends upward of $50,000 to $200,000 on consultants to manage compliance. It’s not uncommon for companies to dedicate five to 10 people working on compliance every week for hours and months on end.

Many in the banking industry are worried about forging into a stigmatized stream of revenue like cannabis, but with the right compliance solutions in place, they can have peace of mind. These solutions guarantee that revenue from cannabis is done legally by analyzing where each dollar came from, and denying those that don’t meet the minimum criteria. Having visibility into cannabis-related business (CRBs) accounts that do the enhanced due diligence is the only way to operate.

By implementing purpose-built compliance management solutions, financial institutions are able to unlock new revenue streams and scale cannabis banking operations. Meaning that as cannabis continues to gain mainstream momentum, and becomes less scrutinized locally and federally, these FIs that take part will be ahead of the curve.

Looking Ahead

With recent movement towards legalization in the House, cannabis investors are optimistic about the industry’s future. So how can the cannabis market overcome these hurdles and remain highly profitable?

To start with, CRBs must have greater access to accredited financial institutions like banks and credit unions. Owning bank accounts, obtaining credit cards, and applying for small business loans is essential to growth. Providing CRBs with access to proper financial support and compliance control is crucial for the cannabis market to continue to thrive.

Federal legislation such as the SAFE Banking Act is currently thought of to be the silver bullet that will open the floodgates for CRBs and FIs to work together. But in reality, this is a myth, as the SAFE Banking Act will simply make the current compliance rules stricter.

To be a first mover FI in your area, businesses must start by implementing a scalable, verifiable cannabis banking program. The real customers and financial opportunities are out there, and are even greater than what you might have modeled given the growth of the industry. The ability to do this today is real.

Benjamin Franklin famously advised fire-threatened Philadelphians in 1736 that “an ounce of prevention is worth a pound of cure.”

With industry growth and maturation comes increased opportunities and challenges. As the cannabis business matures and spreads into new geographic regions, the industry can take advantage of larger markets; however, it also faces increased risk and litigation across a myriad of its operations. This article identifies some of those growing pains along with suggesting how to avoid the more obvious and typical types of issues before they become a problem.

Contracts/Commercial Agreements

One source of emerging trends in cannabis litigation notes that about 1/3 of litigation in 2022 could be classified broadly as commercial disputes. As the various state laws allow for expansion of legal cannabis operations into more states, operators will enter into more commercial agreements to grow and scale operations across the United States.

I am surprised by how many companies do not adequately document their commercial agreements. A host of issues too numerous to discuss in depth here should be addressed in a commercial agreement depending on the type of transaction. In short, make sure agreements are in writing, signed and include an effective date. They should be complete and unambiguous, allocating responsibilities and risk as intended.

Fundraising

When fundraising, whether as debt or equity, a company must comply with complicated and technical U.S. and applicable state securities laws. These laws and regulations require either the registration of the securities offering, which is very expensive, or an applicable exemption from a registration. Failure to comply could lead to lawsuits filed by investors trying to recoup all their money, even if they have no damages, along with possible fraud claims or fines and penalties imposed by applicable federal or state agencies.

Landlord-Tenant disputes

When renting commercial real property, create agreements that address the major issues in writing in case of disputes with property owners. Understanding the lease terms and requirements, as well as tenant rights and duties under state and local law, are essential. Pay attention to lawful uses, minimum term and renewal options, operating expenses and tax requirements, tenant default issues, base rent and other rental charges, common area maintenance charges, maintenance and repair, tenant improvement requirements and allowances, sublet and assignment, and requirements for the refund of the security deposit.

Employment

A common area of misunderstanding that leads to disputes is the law governing employee relations. Companies often misclassify employees, creating valid claims for past due benefits, fines and other damages for failure to classify correctly. In California, for example, correctly classifying a worker as an independent contractor is difficult. Some common mistakes to avoid include:

Designating non-exempt workers as exempt and misclassifying employees as independent contractors.

Failure to pay required minimum wages or overtime.

Not providing required meal and rest breaks.

Failure to keep accurate time records for non-exempt workers.

Inaccurate and noncompliant payroll records (aka “wage statements”) with all the required information.

Improperly administering leaves of absence, especially for employees with medical conditions or disabilities.

Not carefully documenting performance issues by using performance reviews, or “writing up” poor performance, etc.

Failure to have a written employee handbook covering important policies such as vacation and required conduct, as well as misapplying those policies, can lead to disputes. Pay attention to state and local employment laws that apply at the different stages of development and growth.

Intellectual Property

Protecting the company’s intellectual property is important to maintain the goodwill and value of a business. Carefully evaluate the requirements for any patent, trademark, copyright, and/or trade secret protection and come up with a plan to implement and monitor the applicable intellectual property assets. Do not disclose possible patentable intellectual property and inventions before filing a provisional patent application, or the ability to obtain patent protection will be destroyed. Before using a tradename or trademark in commerce, investigate if anyone else is using a similar name for similar goods and services. Failure to do so could lead to claims for infringement and a judgement requiring the company to stop using its preferred name or logo after investing time and money in creating the brand. Consider registering at the state and federal level the name and logo to secure your rights in the brand. What and where a cannabis company can register its brand name and logo for protection are currently limited, so be advised registration can be tricky.

Trade secret protection attaches to valuable information not readily ascertainable by lawful means, such as a formula, pattern, method, device, compilation, program, technique, or process that is secret. Protection afforded to trade secrets does not expire if the information is kept secret. For instance, the Coca-Cola formula has been kept secret for over 100 years, thus maintaining its value. Companies must also implement and maintain appropriate measures to protect the inadvertent disclosure of the information in order to maintain an asset’s status as a trade secret. Before disclosing any confidential information, make sure to have a proper written confidentiality agreement in place with the recipient, or you may lose the protection afforded by trade secret law.

Hiring the right workers to develop valuable intellectual property is important to the success of any business. Make sure to have employees and contractors assign their interests and ownership rights to the work they create, and develop a written invention-assignment agreement in favor of the company to avoid ownership disputes. Interests in copyrightable works created by service providers must be assigned in a written agreement. Failure to do so could diminish the company’s value.

Taxes & Licensing

Sometimes a business unavoidably gets behind in paying its taxes. Failure to pay taxes on time leads to penalties and fines and possible expensive audits by the tax authorities. In addition, personal liability can attach to directors and officers for failure to pay employment taxes. Cannabis companies may have several licensing requirements as well that are important to track to stay in good standing.

Insurance

Adequate insurance is a must-have for every business. Conduct a periodic checkup of the company’s insurance coverage. Consider directors’ and officers’ insurance, general commercial liability and property, products liability, workers’ compensation, employment practices liability coverage, cybersecurity, and business interruption insurance. Those types of coverage are important protections for the risks related to any business that sells a product or service, has employees, deals with the public, or could lose income from unanticipated events like fire, natural disasters and civil interruptions. Discuss your particular insurance needs with a qualified insurance broker, as one size does not fit all.

Consult with Qualified Legal Counsel

Consult with legal counsel to analyze and prepare for the risks noted in this article and other common legal issues to protect the company’s assets, avoid disputes and build and maintain company value. Otherwise, you may find that, as old Ben Franklin noted, you’ll spend many pounds to try to cure problems that could have been avoided with just an “ounce of prevention.”

By Dennis Anding, CPA, Renee Sorrels, CPA No Comments

A utility study can help cannabis growers, cultivators and processors identify opportunities for sales and use tax savings by exposing potential refunds. Thirty-five states currently allow a sales tax exemption for utilities used in manufacturing or processing activities. Thirty-four states have published guidance that provides for a formal utility study process while one state, Mississippi, does not have formal guidance. For Mississippi, the process is to work with the state contacts to secure the exemption.

Generally, the exemption includes the purchase of electricity, natural gas and water and typically applies to the percentage of electricity, natural gas and water used or consumed within the manufacturing process as defined by state statutes and regulations. However, in some states purchased electricity, natural gas and water might be 100% exempt if certain usage percentages are met or exceeded. Facilities that grow, cultivate and process cannabis generally use significant kilowatt hours of electricity in the manufacturing process, and this exemption can result in sizeable tax savings. Without the proper analysis, unwary taxpayers might unknowingly leave significant utility savings on the table.

How to qualify

To qualify for the exemption, states require eligible taxpayers to perform a utility study to analyze the usage of utilities within the manufacturing process versus the taxable use of utilities (such as in general and administrative and office areas). Some states have a predominant use provision under which if 51% or more of an electric or gas meter is used in manufacturing then 100% of the meter’s tax is exempt, while many other states will exempt only the exact percentage of qualified usage as calculated by the utility study.

Some states require the study to be conducted by a third-party provider. Texas requires that the utility study be performed by a certified professional engineer. Taxpayers that engage a third party to conduct a utility study would be wise to consider completing a cost segregation analysis on their facility at the same time, as the two analyses together could bring extra value and savings.

Study process

An energy analysis and comparison should help establish the qualified utility usage percentage used in claiming the sales tax exemption. Once the usage percentage has been calculated in the respective state, it makes sense to review invoices from utility vendors to quantify any sales and use tax overpayment amount.

Refunds for sales and use taxes previously paid can then be requested directly from the state taxing authorities or any vendors retroactively back to the state’s open statute of limitations (typically three to four years). Taxpayers should also establish the exemption prospectively to obtain the benefit of not paying sales and use tax on the amount of manufacturing usage on future invoices. An updated exemption analysis might be needed every three to four years, depending upon the applicable state rules, or when the processing area undergoes a significant update, such as adding new machinery and equipment to the facility or removing machinery and equipment from the facility.

Other sales and use tax refund opportunities

In addition to the exemption on qualified utilities, many states extend the manufacturing exemption to qualified machinery, equipment, and consumables. Generally, to qualify the equipment must cause a physical or chemical change upon the product and be predominantly or directly and exclusively used in the manufacturing process. The exemption may apply to supplies and consumables that are used or consumed in the process as well. Agricultural exemptions are also available for cannabis growers, cultivators, and processors to potentially qualify for.

Qualified organizations only. Independence and regulatory restrictions may apply. Some firm services may not be available to all clients. Given the continued evolution and inconsistency of various state and federal cannabis-related laws, any company should seek competent legal advice relating to its involvement in the cannabis industry, including when considering a potential public offering as a cannabis-related company.

Mergers and acquisition activity in the cannabis space tripled from 2020 to 2021, and that pace is on track to continue in 2022. With big players entering the global cannabis market, we’re fielding more questions about mergers and acquisitions of cannabis businesses.

In this guide, we look at the evolution of the U.S. cannabis industry and some best practices and considerations for M&A deals in this environment.

The New Reality of Cannabis M&A Activity

The industry has evolved since adult use cannabis was first legalized in some U.S. states in 2012. More cannabis companies have a professional infrastructure—legal, financial and operational—with executive teams and board members ensuring the organization establishes proper governance procedures. Investors and private equity firms are showing more interest, and some cannabis companies have celebrated their first IPOs on the Canadian Securities Exchange (CSE).

At the same time, we are seeing a kind of “market grab” by multistate operators (MSOs) looking to acquire various licenses and expand their market share. MSOs tend to understand the current state of the market. For example, in California and some other states, there is a surplus of cannabis on the market for various reasons, partially due to so-called “burner distribution”—rogue distributors using licenses to buy vast amounts of legally grown cannabis at wholesale prices and selling the product on the black market, thereby undercutting retailers and other legal cannabis businesses. Another reason for the surplus is simply the entrance of many legal cultivators into the market over the past year.

Due to these trends, MSOs are interested in acquiring the outlets to be able to sell the surplus cannabis within California and other new markets.

Transferring Cannabis License Rights

One of the biggest challenges to M&A activity in the cannabis sector is the difficulty of transferring or selling a cannabis license.

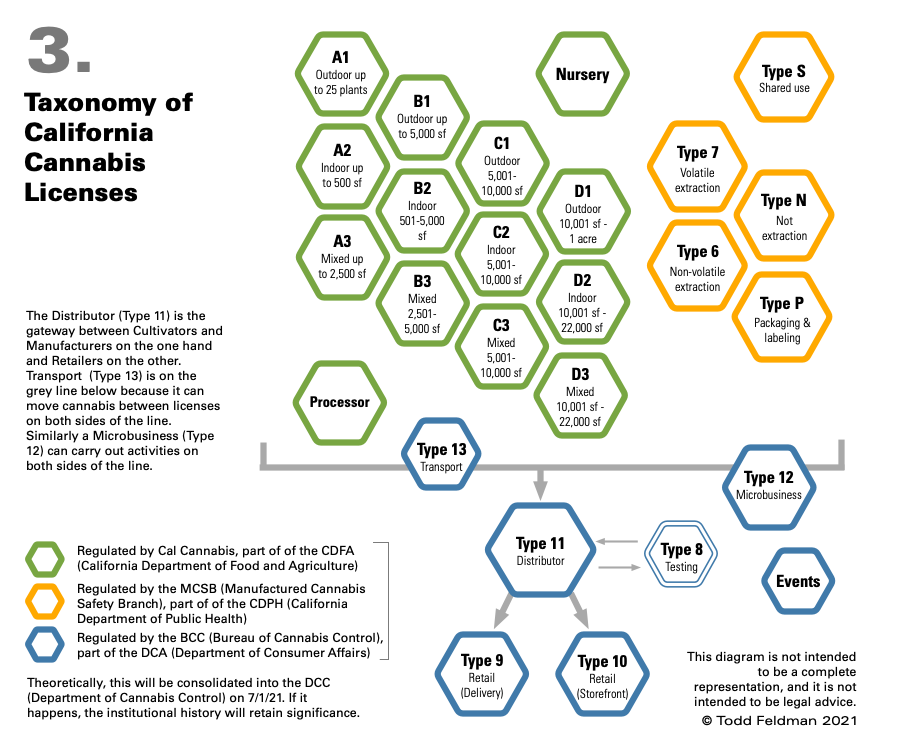

Different types of cannabis licenses in California

Cannabis licenses are not expressly transferable or assignable under California law and many other states. However, the parties involved aren’t without options. For example, a business that is sold to a new owner may be able to retain its existing cannabis license while the new owner’s license application is pending, as long as at least one existing owner is staying on board. At the state license level, a change of up to 20% financial interest does not constitute a change in ownership, although the Bureau of Cannabis Control (BCC) must be notified and approve the change.

This process can take a while—often a year or more—since licensing involves overcoming hurdles at the local level as well as the state level with the BCC. It’s crucial to talk with legal counsel about the particulars of the license and location early in the process to best structure the terms of the agreement while complying with state and local requirements.

Seeking a Tax-Free Reorganization in the Cannabis Space

In many cannabis mergers and acquisitions, the goal is to accomplish a tax-free reorganization, where the parties involved acquire or dispose of the assets of a business without generating the income tax consequences that would result from a straight sale or purchase of those assets.

IRC Section 368(a) defines various types of tax-free reorganizations, including:

In a stock-for-stock reorganization, all of the target company’s stock is traded for a portion of the stock of the acquiring parent corporation, and target company shareholders become minority shareholders of the acquiring company.

Often, it’s tough to meet the requirements to qualify for this type of tax-free reorganization because at least 80% of the target stock must be paid for in voting stock of the acquirer.

Additionally, companies may be saddled with too much debt. If the acquirer assumes that debt, it may be classified as consideration paid to the seller and therefore disqualify the transaction as a tax-free reorganization.

In other M&A deals, the acquiring corporation may be unwilling to assume the debt of the target corporation—perhaps because showing these items on its balance sheet would impact its debt-to-equity and other financial ratios.

Rather than acquiring the target company’s stock, the acquirer may purchase its assets. In a stock-for assets exchange, the buyer must purchase “substantially all” of the target’s assets in exchange for voting stock of the acquiring corporation.

A stock-for-assets format offers the buyer the benefit of not having to assume the unknown or contingent liabilities of the target. However, it’s only feasible if the acquirer purchases at least 80% of the fair market value of the target’s assets AND all or virtually all of the deal consideration will be stock of the acquirer.

Tax Consequences Arising from Sale of Assets

If the sale price doesn’t consist primarily of the buyer’s stock, the transaction may be a standard asset sale. This leads to very different tax results.

If the seller is a C corporation, it will typically face double taxation—paying tax once on the sale of assets within the corporation and again when those profits are distributed to shareholders. If the target company has net operating losses (NOLs), it can use those NOLs to offset the tax hit.

If the seller is an S corporation, it won’t have to pay corporate tax on the transaction at the federal level. Instead, shareholders will pay tax on the gain on their individual returns.

For the buyer, the benefit of an asset sale is that the assets acquired get a “step-up basis” to their purchase price. This is beneficial from a tax perspective, as the buyer can depreciate the assets and may be able to claim accelerated or bonus depreciation to help offset acquisition costs.

The subsidiary merges into the target company before liquidating,

The target company then becomes a subsidiary of the acquirer, and

The target company’s shareholders receive cash.

Structuring the deal this way may work to overcome the hurdle of transferring the license but may not qualify as a tax-free reorganization.

Bottom Line

The circumstances and motivations for mergers and acquisitions in the cannabis industry are diverse. As a result, there is no one-size-fits-all approach to structuring the transaction. In any event, it’s crucial to start the process early and seek advice from legal counsel and tax advisors to minimize the tax burden and ensure that both parties to the transaction get the best deal possible. If you need assistance, contact your 420CPA strategic financial advisor.

The cannabis industry operates in a legal gray area between federal restrictions and state legalization in a constantly changing regulatory environment. Maintaining payroll and HR compliance is a burden cannabis companies face that grows exponentially with geographic expansion of the workforce.

Würk allows cannabis companies to manage payroll, human resources, timekeeping, scheduling and tax compliance, minimizing compliance risks in the ever-changing cannabis regulatory environment. The company uses its expertise and trusted partnerships to provide guidance on 280E tax law, accounting and banking. Its platform is designed to scale nationally with the growth of the industry while incorporating the local laws and regulations unique to individual states. Their clients include Cresco Labs, Canndescent and NUG.

We caught up with Scott Kenyon to ask about Würk’s approach to human capital management, challenges facing cannabis businesses and industry trends. Scott sat on the Board of Würk before becoming its CEO and chairman. Prior to Würk, Scott held leadership roles at Dell and Phunware.

Aaron Green: How did you get involved in the cannabis industry?

Scott Kenyon, CEO and Chairman of Würk

Scott Kenyon: My wife and I were early investors in a few companies in Colorado and Nevada. From early on (this was back in 2015) we learned the hard way of cannabis and how difficult it is to run these businesses, especially in those early days. We’ve progressed a ton over the years, but it’s still very difficult to run cannabis businesses.

I joined Würk about five years ago as a board member. I came on as CEO at the beginning of 2021 after our founder and previous CEO Keegan Peterson, who was an early trailblazer in the industry, passed away. So, I’ve been CEO at Würk for about 18 months.

Green: Tell me about Würk and the main problems you’re trying to solve.

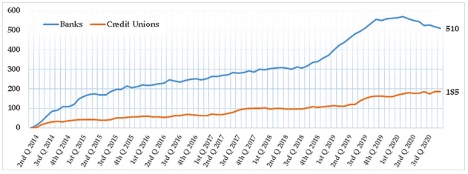

Kenyon: Early on we were focused on establishing getting out of the cash business for these cannabis companies. Allowing them to pay payroll, taxes and be tax compliant electronically was a huge early advantage for us as a company. Now, fast forward seven years later and a lot of different banks (credit unions) are in the industry and that is allowing people to move money. So, that’s not as big of an advantage for us anymore, but early on that was huge.

Our advantage now is the scars on our back, for lack of a better phrase, from what we’ve gone through over the last seven years. We anticipate. We prevent. And most importantly we’ve seen all those problems for our customers. Last year, a big thing of mine was being “Smokey the Bear.” We want everybody to be Smokey the Bear: prevent fires and prevent issues for our customers. When I came in, we were the world’s best firefighters. I didn’t want that title. I wanted to prevent issues for our customers. That takes you from being a vendor to a partner.

If you look at it, on our platform we have 80% of the enterprise cannabis market, about 60% of the mid-market and then low single digits in the small business space. We have that market share because we provide invaluable experience and guidance to our customers. The biggest MSOs have different challenges from a “Joseph and Scott” dispensary, or a “Mary and Jane” grow facility. We’re able to adapt to all those different segments.

At the core of our product, we offer payroll services and what we call HCM – human capital management. That’s everything from scheduling, applicant tracking systems processing and paying your payroll taxes. So, we have the full gamut of product offerings that any type of HCM or HRIS software system does, whether you’re outside of cannabis or inside of cannabis, we’re offering the same thing.

Green: How does Würk differ from say a Professional Employer Organization (PEO)?

Kenyon: We aren’t a PEO. We don’t manage employees. At a high-level, a PEO is basically managing HR for these companies. Our platform enables HR professionals to go out there and do that. PEOs are more popular down in the small business space, because people are not at the scale to hire an HR team. We’re similar in that we’re processing payroll and have all the software that these companies need, but we’re different in that we’re not running their HR for them.

Green: How do you work benefits into the mix?

Kenyon: We leave it to the client, and we integrate their benefits provider into our platform so it’s an easy one-stop shop. We have single sign-on for a lot of our integrations. For the HR organizations, we want them to log into our platform and everything they need will be there.

Green: How is SAFE banking going to affect the HR industry in cannabis?

Kenyon: It’s going to be great for the industry, obviously. For HR specifically, it’s going to bring in more providers of payroll and more competitors for us for sure. But also it’s going to bring in more providers of services that can come in and offer that right now because of the federal illegalization.

Green: How does 280E affect your business and your customers?

Kenyon: We don’t guide people around 280E because that’s a tax specific matter. We refer them to their tax experts. We process payroll tax, which is different than what 280E affects. I think 280E was a big challenge, it’s still a big challenge, but that’s mostly because people didn’t really understand it. I think 280E was a problem five to seven years ago. In the last two years most companies are very familiar with it. That doesn’t mean 280E is the right thing. I think 280E is an awful thing. And while I think I hope SAFE banking is the first thing to fall legislatively, I think 280E has a good chance of getting across first.

On any given day my opinion on which will go first changes. I just want something to get across the line.

Green: What are some unemployment and payroll challenges your customers face?

Kenyon: We really watch unemployment changes and changes in job descriptions or job codes. For example, if an unemployment rate changed, and that unemployed person moved to a different place, which happened a lot during COVID, that company needed to report that and they needed to collect the appropriate charges or taxes there.

Green: What geographies are you in right now?

Kenyon: As of January 1, we had people on our platform in 46 states and just under 600 different jurisdictions. So, even though cannabis isn’t legal in all those states, big companies have employees across the United States.

Green: How do you help your users manage compliance across multiple jurisdictions? That must be a complex undertaking.

Kenyon: Our platform automatically plugs into the states that have electronic notifications around laws, which most states do. In our tax department, we have certain group members that are experts, let’s say, in the west coast. So, we assign people to certain regions to ensure that they have the best knowledge.

From our support piece, where a lot of our customers come in, somebody might say, “Hey, I have a unique question for Utah” and we’ll say we have a person that is specialized in Utah, but we don’t force them there, we just give them the option. But in our tax queue, we actually direct the customer like, “Hey, here’s a Massachusetts Question, so that goes to a particular person because they are our Massachusetts expert.”

Green: How do you deal with timekeeping issues like overtime?

Kenyon: Well, our system does that automatically. Let’s say they’re working overtime in a state that’s difficult to keep time for like California. In the state of California, if they’re working overtime on a Saturday or Sunday or a holiday, that’s a whole different calculation than working longer on a Thursday night. So, our platform is made to automatically calculate that for our customers. There’s no manual adjustments or coaching happening there. We just follow the state law based on where the employees are.

Green: Are you seeing any unionization of employees within the cannabis industry?

Kenyon: There’s unionization in many of our states, I don’t know the exact number, but California being the biggest, there’s a lot of union representation. Illinois is probably the second biggest union state on our platform. I’m assuming New York will be once it becomes adult use.

Green: How does Würk approach cybersecurity?

“Cannabis customers don’t want to buy on the illicit market. They want to buy from a trusted source. It just takes time to make that happen.”Kenyon: Well, we approach it very seriously and I recommend everybody take cybersecurity seriously. We test our internal systems regularly. We test our employees through phishing scams. And we’re always just trying to educate our team on the risk that we have.

I can’t share specifically the prevention steps that we’re taking, but I can tell you we partner with some of the biggest experts and make sure that we’re following everything that they’re recommending. More importantly, we’re testing for human failures, because where most failures happen is with people.

Green: What trends are you following in the industry right now?

Kenyon: Any type of activity in Congress is going to be huge for this industry. So that’s something I always keep abreast of. The next thing that comes down the line which is tied to that is interstate commerce: How is interstate commerce going to really come into play? And how does that change this industry?

Within the industry, the big question is how do we combat the illicit market? Over the last five years, I’ve heard all kinds of different ideas. But in the end, I think we have to out-innovate the illicit market, and that’s what I’m most excited about.

There are new product categories, beverage being one that is starting to gain traction. How are these new products and new variations of the cannabis plant able to treat and help people in ways that we’ve never thought of? That’s part of out-innovation. I was reading an article today about new terpenes that were discovered and how 100 products could come from each one of those new terpenes. I think we’re just still at the tip of the iceberg of product innovation.

How do we fight the illicit market? I think that is just through coming up with new products that treat different illnesses and ailments, that allow customers to get away from pharmaceuticals. Cannabis customers don’t want to buy on the illicit market. They want to buy from a trusted source. It just takes time to make that happen. They’re not going to do it when there’s a huge price difference, but they will do it when there’s a huge product difference. And right now, our products are very similar to what you can find on the illicit market. You can find vapes, you can find gummies, you can find all that in the illicit market. We’ve got to out-innovate the illicit market.

Green: What in your personal life are you most interested in learning about?

Kenyon: I am the father of two teenagers right now and I really like to learn how to be a better parent to them because it’s really frickin’ tough!

Despite the US making cannabis regulations challenging to navigate, the industry is snowballing toward profitability. New Jersey legalized adult use cannabis on April 21 this year. One month earlier, The Garden State began accepting applications for Class 5: Retailers, Dispensing and Delivery.

Although New Jersey isn’t shy about its licensing requirements and standards, many people want to know how retailers can stay in the game for the long run. So, let’s talk about risk management considerations New Jersey retailers need to know.

Top Risks Cannabis Retailers Face in New Jersey

Regardless of what kind of retailer you operate —medical or adult use — it’s critical to know what you’re up against. The following are the most common risks we’ve watched cannabis retailers face daily in New Jersey, making a customized risk management strategy necessary.

Theft

Like other retailers, New Jersey cannabis retailers are vulnerable to theft. Unfortunately, theft can come from various angles, such as in-store, in-transit and insider crime. Besides cannabis retailers typically having a well-stocked inventory, it’s not uncommon for them to have more cash on hand than most other businesses.

Although the SAFE Banking Act could positively impact the cannabis industry, it’s in a notorious stall yet again. Briefly, the SAFE Banking Act would no longer allow financial institutions, such as banks and credit card companies, to refuse to do business with cannabis companies. However, cannabis retailers must operate in a cash-only environment, for now, forcing them to make bank runs multiple times a day. We probably don’t have to explain how enticing a significant inventory and fat bank bags look to criminals.

Cybersecurity

Since the onset of the global health crisis, the cyber liability landscape has nearly spun into a death spiral. In other words, cybercriminals sat on the edge of their seats during the pandemic, waiting to pounce on anything that looked slightly vulnerable. Remote workers, small businesses, and emerging industries were hard-hit.

It’s no surprise that New Jersey cannabis retailers face many cybersecurity risks through their point of sale (POS) systems. Additionally, retailers often gather and store personal information, such as email addresses, credit card numbers, shipping addresses, etc. Hackers and cybercriminals gravitate to this vital data rapidly.

Property Damage

In addition to the risk of theft, as mentioned above, cannabis retailers must protect their property from losses. Without adequate protection, damage to equipment or buildings could add up to high out-of-pocket costs. Consider the damage a weekend office fire or late-night vandalism would cause. If property damage occurs, retailers must figure out how to sustain business operations while recovering from the loss simultaneously. As a result, New Jersey retailers must protect their property and maintain business continuity.

How to Customize a Risk Management Strategy

Watch or listen to any news reports and there’s a decent chance that you’ll feel some slight sense of doom and gloom. And sure, a lot is going wrong in our world; however, that doesn’t need to impact how you perceive your businesses. Instead of casting a massive net over every possible risk that you can imagine, we recommend trying the following 5-step approach. Here’s the gist:

Identify: Pinpoint high-level risks that are specific to the cannabis industry. Then, let the process trickle down to focus on company-specific exposures.

Analyze: Determine how badly a particular risk could harm your retail company. How much will this hurt should the “what-ifs” play out?

Evaluate: Categorize risks according to how risk tolerant your company is. Will you avoid, transfer, mitigate or accept the risk?

Track: Use your history or the stats from a similar retailer to map out how you’ve handled the risk over time. Older retailers have an advantage over younger retailers, of course, but you can still get a feel for your risk management style.

Treat: Make good on your evaluation promises by avoiding, transferring, mitigating, or accepting the various risks you identified.

Recommended Insurance for New Jersey Retailers

Sales totals in the first month of New Jersey’s adult use market

The New Jersey Cannabis Regulatory Commission issued detailed requirements for new cannabis businesses. That said, part of the application requirements considered is the plan for companies to obtain liability insurance. Many new retailers opted for a “letter of commitment” as opposed to a certificate of insurance (COI), stating their plans for obtaining the following coverages:

Commercial general liability: Protects cannabis companies against basic business risks.

Product liability: Protects against claims alleging your product or service caused injury or damage.

Property: Reimburses cannabis companies for direct property losses.

Workers’ compensation: Covers employees if they are injured on the job and can no longer work.

In addition to the required insurance coverages, we recommend New Jersey retailers customize their risk management package with these policies:

Crime: Protects your cannabis company against specific money theft crimes.

Cyber: Protects your cannabis company against damages from specific electronic activities.

Directors & officers: Protects corporate directors’ and officers’ personal assets if they are sued.

Employment practices liability: Protects cannabis companies against employment-related lawsuits.

Professional liability: Protects cannabis companies against lawsuits of inferior work or service.

With more states in the US entering the marketplace soon, New Jersey is doing its fair share of the heavy lifting by spearheading the onboarding process. Remember, doing your due diligence at the start pays off in the long run — New Jersey retailers are proving that. Consider teaming with a commercial insurance broker calibrated to the cannabis industry, so you get the most out of your broker, marketplace and the cannabis industry as a whole.

By Abraham Finberg, Simon Menkes, Rachel Wright No Comments

Some states, like California, Colorado and Washington, have welcomed cannabis with open arms while others have taken a while to come to the party (or haven’t gotten there yet). Missouri, whose licensed sales only began in October 2020, is one of the late arrivals.

Perhaps it’s in the nature of the people of the Show Me State to wait for proof that something is a good thing rather than being early adopters. Even Missouri’s nickname came into being as a statement of skepticism when Missouri Congressman Willard Duncan Vandiver, in an 1899 speech in Philadelphia, said, “Your frothy eloquence neither convinces nor satisfies me. I am from Missouri. You have got to show me.” (Not surprisingly, perhaps, Missouri’s state animal is the Missouri Mule).

Missouri legalized the use of medical cannabis on December 6, 2018. Compared to many other states, Missouri’s definition of what constitutes medicinal use is more tightly defined. For example, most medical cannabis states allow “anxiety” as an acceptable condition for a prescription; Missouri does not.1

Current Status of Adult Use Cannabis

St. Louis, Missouri

Missouri is now locked in a battle to legalize adult use cannabis, with the group Legal Missouri 2022, among others, working hard to put the measure on the ballot this year. At the same time, Representative Ron Hicks (R) is pushing to legalize recreational purchases with his Cannabis Freedom Act. “I want the legislature to be able to handle it so that when there are problems and things need to be changed, it can be changed,” Hicks said.2 Missouri Governor Mike Parson (R), who has been against recreational usage, has stated he would “much rather have the legislators have that discussion out here and see if there is a solution other than doing the ballot initiative.” Parson added, “If it got on the ballot, it’s probably going to pass.”3

Cannabis Business in Missouri: Only Cost of Goods Sold Deduction

Missouri has maintained its state tax code to be in conformity with Section 280E of the Internal Revenue Code, which disallows deductions and credits for expenditures connected with the illegal sale of drugs, stating:

No deduction or credit shall be allowed for any amount paid or incurred during the taxable year in carrying on any trade or business if such trade or business … consists of trafficking in controlled substances (within the meaning of schedule I and II of the Controlled Substances Act) which is prohibited by Federal law.4

This is true for both corporation5 and individuals6 in Missouri.

Governor Mike Parson recently vetoed a bill to eliminate conformity with I.R.C. Section 280E. Eliminating conformity would have lowered the tax burden on medical cannabis businesses, and increased Missouri’s competitiveness.7

State Sales and Cannabis Taxes

Missouri taxes retail sales at 4% of the purchase price.8 In addition, Missouri taxes retail sales of medical cannabis another 4% of the retail price.9,10 The medical cannabis tax is collected by dispensary facilities who then remit it to the Department of Revenue using Form 5808.11

Tax compliance is burdensome in Missouri, with dispensaries having to file returns monthly, even when they have no tax to report.12 Missouri also doesn’t allow cannabis businesses to pay their taxes in cash.13

No Tax on Tax

It’s important to note that Missouri doesn’t charges sales tax on cannabis tax nor cannabis tax on cannabis tax (unlike high-tax states like California). Under Missouri’s law, the tax is “separate from, and in addition to, any general state and local sales and use taxes that apply to retail sales.”14 Under Missouri’s sales tax law, “ Tax collected as a part of a sale should not be included in gross receipts.”15 Missouri has not specified whether the medical tax constitutes tax collected as a part of a sale; however, its regulations state that gross receipts from the sale of cigarettes do not include the amount of the sale price that represents the state cigarette tax.16 If the medical tax is analogous to the cigarette tax, gross receipts from the sale of medical cannabis likely excludes the amount paid as medical cannabis tax.

If the Legislature-Sponsored Cannabis Freedom Act Passes

If the Cannabis Freedom Act passes, Missouri will have a number of additional interesting changes. The bill would only allow for double the number of current medical cannabis licensees to serve the adult use market. It would also allow for people with non-violent convictions to petition the courts to have their record expunged (cleared).

Adult Use Taxes

The Act would allow the Department of Revenue to set an adult-use tax of up to 12%. There would be no such tax on medical cannabis sales.17

Normal Tax Deductions Allowed for Businesses

Licensed businesses would also be able to make tax deductions with the state up to the amount that they’d otherwise be eligible for under federal law if they were operating in a federally legal industry.18

Amendment Added to Act

In a move seen by many as a bid to derail the Cannabis Freedom Act, Representative Nick Schroer (R) amended the Act to bar transgender women from accessing no-interest loans for women- and minority-owned cannabis businesses, adding that only women who are “biologically” female would be eligible for the benefit. In the end, this addition may have the effect of scuttling the bill.19

Multiple Efforts to Place Cannabis on the Ballot

Even if the Act doesn’t pass, there are multiple efforts to place cannabis before the voters, including one by Representative Shamed Dogan (R), the group Legal Missouri 2022, which got medical cannabis passed by voters in 2018, and Fair Access Missouri.20

Comparison to Neighboring Oklahoma

Oklahoma, like Missouri, has not legalized the use of recreational cannabis, only medical cannabis. Also, Oklahoma taxes sales of tangible personal property (except newspapers and periodicals) at 4.5%, which is close to Missouri’s 4%.21 Tax is imposed on gross receipts or gross proceeds.22 Gross receipts (or gross proceeds) = Total amount of consideration, whether received in cash or otherwise. Credit is allowed for returns of merchandise.23

Oklahoma taxes retail medical cannabis sales at 7% of the gross amount received by the seller.24 Like Missouri, it has not specified any exemptions from the medical cannabis tax. Oklahoma’s medical cannabis tax base is the same as Missouri’s. Oklahoma’s medical tax rate is higher than Missouri’s. Therefore, Missouri’s tax treatment of medical cannabis is even better than Oklahoma’s.

Note, however, that Oklahoma has made it explicit that there is no tax-on-tax. “The 7% gross receipts tax is not part of the gross receipts for purposes of calculating the sales tax due, if the tax is shown separately from the price of the medical marijuana.”25

Oklahomans appear to be far more favorably disposed towards cannabis than Missouri, however. 2021 cannabis sales per person in Missouri was approximately $34, while Oklahoma boasted an impressive $210 per person, besting even California, which had $111/per person in cannabis sales.26

The Hidden Opportunity

Although Missouri only began licensed sales in October 2020, the state’s monthly sales has shown a strong upward curve. By the end of June 2021, monthly sales were just above $16 million. That number had shot up to $29 million per month for December 2021, and almost $37 million for April 2022.27 Patient enrollment is also increasing significantly.28

The best move, many experts believe, is to get into the medical market now, before the inevitable happens and adult use is approved. Competition is low at the moment, due to the lack of medical licensed dispensaries in the state. Although obtaining a license can be difficult, the current lack of competition, as well as the opportunity to gain a foothold in the cannabis industry before recreational purchases are approved, could provide a 10 times revenue increase from current medicinal sales levels.

Tyler Williams, founder of St. Louis-based Cannabis Safety and Quality and one of the St. Louis Business Journal’s 2021 40 Under 40, is optimistic about the future of Missouri cannabis. The state, he says, has been left “with only a few cannabis growers and manufacturers with a head start over the impending recreational market that is likely to come within the next couple of years.”29

The Bottom Line

The State of Missouri’s treatment of legal cannabis has been mixed, but the demand for the product by many residents of the state is unquestioned. If an entrepreneur has the foresight to get involved before all the wrinkles of legalization have been resolved, there is a possibility for very strong return on investment.

Update: Governor McKee has signed the Rhode Island Cannabis Act into law, making it the 19th state to legalize adult use cannabis.

In Rhode Island this week, lawmakers voted to approve a bill that would legalize and regulate adult use cannabis. The state’s legislature passed the bill with overwhelming majorities in both the House of Representatives and the Senate.

The House voted 55-16 and the Senate voted 32-6 to approve the Rhode Island Cannabis Act, a bill that allows adults over 21 to possess, purchase and grow cannabis. The legislation contains a provision for automatic review and expungement of past cannabis convictions. Similar to other neighboring states, the bill also allows for allocating tax revenue from cannabis sales to communities most harmed by cannabis prohibition, such as low income neighborhoods.

Rhode Island Gov. McKee

Governor Daniel McKee has expressed support for the bill previously and is expected to sign it into law. According to Jared Moffat, state campaigns manager for the Marijuana Policy Project, Rep. Scott Slater, Sen. Josh Miller and Rep. Leonela Felix are to thank for their leadership in bringing the bill to a vote. “We are grateful to Rep. Scott Slater and Sen.Josh Miller for their years of leadership on this issue. Rhode Islanders should be proud of their lawmakers for passing a legalization bill that features strong provisions to promote equity and social justice,” says Moffat. “We’re also thankful to Rep. Leonela Felix who advocated tirelessly for the inclusion of an automatic expungement provision that will clear tens of thousands of past cannabis possession convictions.”

Among other provisions, the bill establishes a 10% sales tax in addition to the state’s normal 7% sales tax and 3% local sales tax. A quarter of all retail licenses will go to social equity applicants and another quarter of all licenses will be reserved for worker-owned cooperatives. The legislation also includes a “social equity assistance fund” that will offer grant money, job training and social services to communities most impacted by cannabis prohibition.

As the regulated cannabis industry matures, M&A activity is expected to continue accelerating. Whether they are existing licensed businesses looking for acquisition opportunities or new investor groups seeking to enter or expand their positions in the industry, investors should recognize the special due diligence challenges associated with cannabis industry transactions.

Above all, investors should avoid the temptation to omit or short-circuit long-established due diligence practices, mistakenly believing that some of these steps might not be relevant to cannabis and hemp operations. Despite the unique nature of the industry, thorough and professional financial, tax and legal due diligence are essential to a successful acquisition.

Surging M&A activity

Over the past few years, as the cannabis industry matured and the regulatory environment evolved, M&A activity involving cannabis and hemp companies has undergone several cycles of expansion and contraction. Today, the expansion trend clearly has resumed. Although the exact numbers vary from one source to another, virtually all industry observers agree that 2021 saw a strong resurgence in cannabis-related M&A activity, with total transactions numbering in the hundreds and total deal values reaching into billions of dollars. Moreover, most analysts seem to agree that so far, the pace for 2022 is accelerating even more.

Today, many existing cannabis and hemp multistate operating companies are in an acquisitive mood as they look for opportunities to scale up their operations, enter new markets, and vertically integrate. At the same time, the projections for continued industry growth over the next decade have attracted a number of investment funds and private equity groups, which were formed specifically for the purpose of investing in cannabis and hemp businesses.

These two classes of investors often pursue distinctly different approaches to their transactions. Unlike the largely entrepreneurial cannabis industry pioneers now looking to expand, the more institutional investors are accustomed to working with professional advisers to perform financial, tax and legal due diligence as they would for a transaction in any other industry.

Among both groups, however, there is sometimes a tendency to misunderstand some of the transactional risk elements associated with cannabis M&A deals. In many instances, buyers who are generally sensitive to potential legal and regulatory risks will underestimate or overlook other risks they also should examine as part of a more conventional financial and tax due diligence effort.

For example, since much of the value of a licensed cannabis operation is the license itself, investors often rely largely on their own industry understanding and expertise to assess the merits of a proposed acquisition, based primarily on their estimation of the license’s value. This practice provides acquirers with a narrow and incomplete view of the deal’s overall value. More importantly, it also overlooks significant areas of risk.

Because cannabis acquisition targets typically are still quite new and have no consistent earning records, acquirers also sometimes eschew quality of earnings studies and other elements of conventional due diligence that are designed to assess the accuracy of historical earnings and the feasibility of future projections.

Such assumptions and oversights often can derail an otherwise promising transaction prior to closing, causing both the target and the acquirer to incur unnecessary costs and lost opportunities. What’s more, even if the deal is eventually consummated, short-circuiting the normal due diligence processes can expose buyers to significant unanticipated risk down the road.

Recurring issues in cannabis acquisitions

The most widely recognized risks in the industry stem from the conflict between federal law and the laws of various states that have legalized cannabis for medical or adult recreational use. The most prominent of these concerns relates to Section 280E of the Internal Revenue Code (IRC 280E).

Although its use is now legal in many states, cannabis is still classified as a Schedule I substance under the federal Controlled Substances Act. IRC 280E states that any trade or business trafficking in a controlled substance must pay income tax based on its gross income, rather than net income after deductions. As a result, cannabis businesses are not entitled to any of the common expense deductions or tax credits other businesses can claim.

The practical effect of this situation is that cannabis-related businesses – including growers, processors, shippers and retailers – often owe significant federal income tax even if they are not yet profitable. Everyone active in the industry is aware of the issue, of course, and any existing operating company or investment group will undoubtedly factor this risk into its assessment of a proposed acquisition target.

The challenge can be exacerbated, however, by other, less widely discussed factors that also affect many cannabis businesses. These issues further cloud the financial, tax and regulatory risk picture, making thorough and professional due diligence even more critical to a successful acquisition.

Several of these issues merit special attention:

Nonstandard accounting and financial reporting practices. As is often the case in relatively young, still-maturing businesses, acquisition targets in the cannabis industry might not have yet developed highly sophisticated accounting operations. It is not uncommon to encounter inadequate accounting department staffing along with financial reporting procedures that do not align with either generally accepted accounting principles or other standard practices. In many instances, company management is still preparing its own financial statements with minimal outside guidance or involvement by objective, third-party professionals. Significant turnover in the management team – and particularly in the chief financial officer position –is also common, as is a general view that accounting is a cost center rather than a value-enhancing part of the management structure.

Such conditions are not unusual in young businesses that are still largely entrepreneurial in spirit and practice. In the cannabis industry, however, this situation is also a reflection of many professional and business services firms’ longstanding reluctance to engage with cannabis operators – a hesitancy that still affects some organizations.

When customary business practices are not applied or are applied inconsistently, acquiring companies or investors should be prepared to devote more time and attention – not less – to conventional financial due diligence. The expertise of professional advisers with direct experience in the industry can be of immense benefit to all parties in this effort.

Restructuring events or nonrecurring items in financial statements. Restructuring events and nonrecurring items are relatively common in many new or fast-growing businesses, and they are especially prevalent among cannabis operations. In many instances, such companies have engaged in multiple restructuring events over a short period of time, often consolidating operations, taking on new debt, and incurring various one-time costs that are not directly related to the ongoing operations of the business.

The inclusion of various nonrecurring items within the historical financial statements can make it much more difficult for a buyer or investor to accurately identify and assess proforma operating results, especially in businesses that have not yet generated consistent profits. Here again, applying previous experience in clearing up the noise in the financial statements can help improve both the accuracy and timeliness of the due diligence effort.

Run-rate results inconsistent with historical earnings or losses. A company’s run rate – an extraction of current financial information as a predictor of future performance – is a widely used tool for creating performance estimates for companies that have been operating for short periods of time or that have only recently become profitable. In cannabis businesses, however, run-rate estimates sometimes can be unreliable or misleading.

Because it is based only on the most current data, the run rate often does not reflect significant past events that could skew projections or recent changes in the company’s fundamental business operations. Because such occurrences are relatively common in the industry, the results of run-rate calculations can be inconsistent with the target company’s historical record of earnings or losses.

Historical tax and structuring risks new owners must assume. Like many other new businesses, cannabis operations often face cash flow and financing challenges, which owners can address through alternative strategies such as debt financing, stock warrants, or preferred equity conversions. Such approaches can give rise to complex tax and financial reporting issues as tax authorities exercise their judgment in interpreting whether these items should be reported as liabilities or equity derivatives. The situation is often complicated further by various nonstandard business practices and the absence of sophisticated accounting capabilities, as noted earlier.

As a consequence, financial statements for many cannabis companies – including a number of publicly listed companies – often contain complex capital structures with numerous types of debt warrants, conversion factors and share ownership options. Although an acquisition would, in theory, clean up these complications, buyers nevertheless must factor in the risk of previous noncompliance that might still be hidden within the organization – a risk that can be identified and quantified only through competent and thorough due diligence.

Not as simple as it seems

On the surface, the fundamentals of the cannabis industry are relatively straightforward, which is one reason it appeals to both operators and investors. For example, participants at every stage of the cannabis business cycle – growing and harvesting, processing and packaging, shipping and distribution, and ultimately marketing and retailing – can readily apply well-established practices from their counterparts in more conventional product lines.

The major exception to this rule, of course, is the area of regulatory compliance, which is still shifting and likely will continue to do so for the foreseeable future. Outside of this obvious and significant exception, however, most other aspects of the industry are relatively predictable and manageable.

When viewed in this light and in light of the continued growth of the industry, it is easy to see why cannabis-related acquisitions are so appealing to existing business operators and outside investors alike. It is also easy to understand why buyers might feel pressure to move quickly to take advantage of promising opportunities in a fast-changing industry.

As attractive as such opportunities might be, however, buyers should take care to avoid shortcuts and resist the urge to sidestep established due diligence procedures that can reveal potential accounting and financial statement complications and the related compliance risks they create. The unique nature of the cannabis industry does not make these practices irrelevant or unnecessary. If anything, it makes professional financial, tax, and legal due diligence more important than ever.

Crowe Disclaimer: Qualified organizations only. Independence and regulatory restrictions may apply. Some firm services may not be available to all clients. Given the continued evolution and inconsistency of various state and federal cannabis-related laws, any company should seek competent legal advice relating to its involvement in the cannabis industry, including when considering a potential public offering as a cannabis-related company.

This website uses cookies so that we can provide you with the best user experience possible. Cookie information is stored in your browser and performs functions such as recognising you when you return to our website and helping our team to understand which sections of the website you find most interesting and useful.

Strictly Necessary Cookies

Strictly Necessary Cookie should be enabled at all times so that we can save your preferences for cookie settings.

We use tracking pixels that set your arrival time at our website, this is used as part of our anti-spam and security measures. Disabling this tracking pixel would disable some of our security measures, and is therefore considered necessary for the safe operation of the website. This tracking pixel is cleared from your system when you delete files in your history.

We also use cookies to store your preferences regarding the setting of 3rd Party Cookies.

If you disable this cookie, we will not be able to save your preferences. This means that every time you visit this website you will need to enable or disable cookies again.

These days, however, the Ocean State has turned over a new leaf. It legalized medical cannabis in 2006, and on May 25, 2022, legalized adult use sales as well. Starting in December 2022, Rhode Island residents could purchase cannabis from five of the six medical cannabis dispensaries across the state which have also been approved to sell to adults.

These days, however, the Ocean State has turned over a new leaf. It legalized medical cannabis in 2006, and on May 25, 2022, legalized adult use sales as well. Starting in December 2022, Rhode Island residents could purchase cannabis from five of the six medical cannabis dispensaries across the state which have also been approved to sell to adults.