As Germany begins to enter a summer where life seems ever more normal, there are fairly major shakeups underway in the German cannabis market. These are structural but will have a profound impact on the entire market going forward.

A Mass Of Distribution Licenses It is an interesting metric to understand that before 2015, there were no specialty cannabis importer/distributors in Germany. As of July 2020, there are rumors that this number has now shot to close to 80 (either licensed or in the process to become licensed). That is a huge number. So was the last amazing number (40) as of the beginning of this year. Just the previous estimate would mean, literally, 1 specialty cannabis distributor for every 2 million Germans. That obviously is not sustainable. What it does indicate is the huge surge of interest in medical cannabis not to mention acceptance, as well as the amount of money actually now beginning to slosh around in the domestic market.

And that spells good news for both patients and insurers. The rest of the industry, however, will be under further pressure to reduce cultivation and operation costs to meet the challenge.How many of these distributors will survive is another question, particularly in an environment where the government is looking for just one to fulfil the needs of all of Germany’s pharmacies from what is grown domestically. This does not of course mean the end of specialty distribution. Indeed, far from it. There is not enough cannabis entering the market, presumably this fall, that is grown here to even come close to meeting demand.

No surprises here. This has been one of the enduring criticisms of the entire process, if not the bid itself since 2017.

However, one thing this does mean is that distribution fees, like pharmacy fees for processing the plant before them, are finally hitting a price adjustment phase.

This is also going to be good not only for patients, but also health insurers.

For all the standardization of the industry, including fees and mark-ups, one of the strangest things about the German cannabis market is how widely cannabis prices can differ even between pharmacies. This is as true of flower as it is of dronabinol.

The Wholesale Price Of Medical Cannabis Is Dropping Again, no surprise here, the government will end up buying more cannabis than contracted for under the original bid. This was actually anticipated in the language of the contract that currently exists between the government and the three bid winners. Namely, an automatic 50% reduction in price is mandated for any cannabis sold beyond the 120% agreed upon qualities.

Photo: Ian McWilliams, Flickr

The growers domestically, in other words, who won the bid will be under a severe price restriction. This may have been the ultimate strategy of the government to begin with (namely to attract foreign capital and expertise but then begin to reign in the sky-high prices of medical cannabis so far.)

This means that the price of €2.30 a gram will undoubtedly fall. Where it will float is anyone’s guess, but right now it appears on course to hit about €1.87. Or about the same price that other governments across Europe (notably Italy) had previously negotiated with the big Canadian cannabis companies (notably on this one, Aurora’s military contract in Italy).

Implications For The Import Market With domestic producers under the gun, this also means that all imports will begin to feel the price squeeze too. And that will also have a significant impact on point of sale cannabis prices.

And that spells good news for both patients and insurers. The rest of the industry, however, will be under further pressure to reduce cultivation and operation costs to meet the challenge.

Techniker Krankenkassen (or TK as it is also frequently referred to) is one of Germany’s largest public or so-called “statutory” health insurance companies. It is companies like TK that provide health insurance to 90% of the German population.

TK is also on the front lines of the medical cannabis discussion. In fact, TK, along with other public health insurers AOK and Barmer, have processed the most cannabis prescriptions of all insurers so far in the first year after the law change. There are now approximately 15,000 patients who have received both a proper prescription and insurance approval coverage. That number is also up 5,000 since the beginning of just this year.

In a fascinating first look at the emerging medical market in Germany, TK, in association with the University of Bremen, has produced essentially the first accessible report on approvals, and patient demographics for this highly stigmatized drug.

Because it is in German, but also contains information critical to English-speaking audiences in countries where the medical issue is being approached more haphazardly (see the U.S. and Canada), Cannabis Industry Journal is providing a brief summary of the most important takeaways from TK’s Cannabis Report.

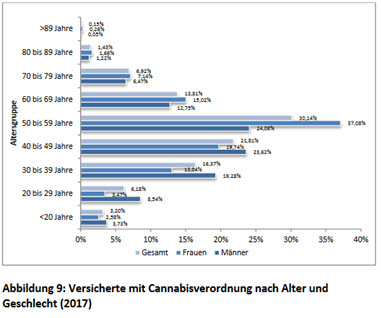

Patient demographics from the report

Most Patients Are Women

This is not exactly surprising in a system where symptomology rather than ability to pay is the driver of authorizations and care. This is also exactly the opposite trend when it comes to gender at least, that emerged in Colorado on the path to medical legalization circa 2010-2014. While chronic pain is still the most common reason for dispensation, the drug is going mostly to women, not men, in their forties, fifties and sixties.

Even Chronically Ill Patients Are Still not Getting Covered

This data is super interesting on the ground for both advocates and those who are now pushing forward on “doctor education” efforts that are springing up everywhere. The only condition for which cannabis was approved 100% was for patients suffering from terminal cancer pain from tumours. In other words, they were also either in hospice or hospital where this kind of drug can be expedited and approved quickly. Other conditions for which the drug was approved were both at far lower rates than might have been expected (see only a 70% approval rate for Epilepsy and a 33% approval rate for Depression).

Conditions and degrees of coverage chart from the report

Expect approval rates to change, particularly for established conditions where the drug clearly helps patients, even if there are still questions about dosing and which form of cannabis works best, along with improved research, data and even patient on boarding.

Also expect interesting data to come out of this market for patients with ADHD (or ADHS).

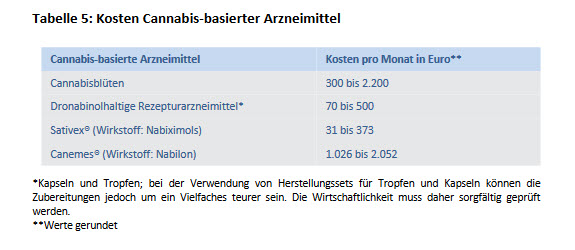

Imported Cannabis Is Very Expensive

A table showing the different medicines prescribed in Germany

TK and other public health insurers are also on the front lines of another issue not seen in any other legalizing cannabis country at the moment. An eye-wateringly high cost per patient. The biggest reason? Most of the medical cannabis in the market is being imported. This will change when more cannabis begins to enter the market from other EU countries (see Spain, the Baltics and Greece) and, yes, no matter how many elements of the German government are still fighting this one when it begins to be cultivated auf Deutschland.

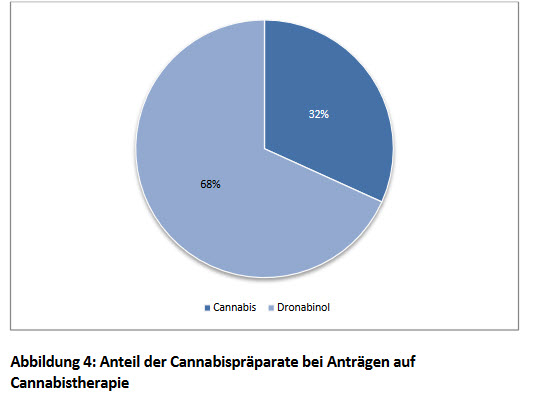

Most German Patients Are Still Only Getting Dronabinol

If there was one thing that foreign investors should take a look at, it is this. One year after legalization, just over 1/3 of those who actually qualify for “medical cannabis” are in fact getting whole plant medication or a derivative (like Sativex).

This means only one thing. The market is continuing to grow exponentially over at least the next five to ten years.

Most German Patients Are Still Only Getting Dronabinol

Munich, Germany- In a darkened movie studio on the east end of town, the Digital Insurance Agenda or DIA, the largest insurtech conference in the world, kicked off its annual event in mid-November. The sold-out event attracted about 1,000 top insurance executives from 40 countries and all six continents.

CannabisIndustryJournal attended from the perspective of investigating the overall status of digitalization in the industry. However, there were a couple of things we were on the hunt for. The first was to see how and where blockchain has begun to penetrate the industry. This revolutionary processing and identification layer of digital communications is coming – and fast – to the insurance industry everywhere.

All image credits: MedPayRx (Instagram)

We were also there of course to see if cannabis was anywhere on the agenda. Digitized or not.

By way of disclosure, I am also a high tech entrepreneur with my own insurtech, blockchain-based start-up that we are in the process of launching. MedPayRx is intended to be the first insurance product that will help patients access their meds facing nothing but their co-pay and help insurers automate the approvals process for all prescription drugs and medical devices.

By definition, in Germany, this includes medical cannabis.

Ultimately, our mission is to take the paper and the pain of all reimbursement out of the prescription process. At present, as anyone with a chronic condition knows, many medications and medical devices must be paid for out of pocket first and then reimbursed via a claims process that is paper-based, laborious and expensive. This is not a model that works for anyone. Certainly not poor and chronically ill patients who face this process at least monthly. And certainly not insurers who are now facing higher drug costs if not more claims reimbursements for the same from an aging population.

In a country like Germany where 90% of the population is covered by public health insurance, the situation also poses quandaries of a kind that are rocking the fundamental concept of inclusive public healthcare.

The Impact of Digitalization On The Insurance Industry

As one insurance executive and speaker mentioned from the stage during DIA, there are few industries that are more universally despised than insurance in general. And few verticals where the existing mantra is “you cannot do it worse.” The insurance industry is well aware of that. Further, for all insurances that are not “mandatory” the competition is fierce for consumers’ bucks. Particularly in places like Europe where insurance is also seen as a kind of savings scheme.

If you are a private insurer, of any kind, or offering services to both end consumers and B2B services, you are out of the game if you are not now thinking how to streamline and upgrade all aspects of your business in the digital era. There are many start-ups now tackling what is euphemistically called “cloud2cloud” integrations.

What does that mean?

According to DIA co-founders Reggy de Feniks and Roger Peverelli, the influence of tech in general is here to stay and is now driving widespread innovation across the industry. “The DIA line-up and the massive response among the audience show that insurtech is now mainstream,” says de Feniks. “This edition clearly showed the…ever growing attention for artificial intelligence, machine learning and other shapes of advanced analytics.”

“Platform thinking, thinking beyond insurance and creating new insurtech enabled services will be the next challenge for insurers,” added Peverelli.

Subtext? Insurers want your data. They want to use tech to analyse and understand it. The technology is here. But is the regulation? Specifically, in an industry that wants to know everything about you, how is privacy understood and implemented with revolutionary tech?

A Cloud-Based Future

Paper is rapidly becoming an old-fashioned concept in insurance, much like it has in banking. And like banking, insurance has a strong “financial” side to it. Germans, for example, tend to use insurance policies as retirement accounts, (the idea of a 401K is almost unheard of here). And by far, the most dynamic and digitalized part of the industry tends to be in areas unrelated to healthcare.

Some of the most interesting start-ups at DIA were actually weather-based.

The challenges of these types of insurtechs of convincing both regulators and the industry that such services are not only feasible but needed, pale in comparison however, to the challenge now facing all public health insurers.

And while they were certainly present at DIA, this industry segment was underrepresented at the November gathering. There is a reason for this. The real threat to consumer medical privacy is only growing, not receding in an era where data can be seamlessly transferred globally and digitally.

For that reason, blockchain has many uses and applications in this part of the vertical.

MedPayRx – even as a pre-seed start-up, was not, even this year, the only blockchain-based service we found in attendance at DIA. Next year look for even more.

Blockchain might be the next new “buzzy” tech, but in the insurance industry, there is a real reason for it.

What Was The Response To A Cannabis-Themed “Insurtech?”

As readers in the United States know, health insurance and cannabis is a loaded subject. And while insurance services are beginning to be available as high-risk commercial services for the industry, inclusive health insurance is still off the table because of the lack of federal reform.

Other places, however, the issue is taking a fascinating turn. And in Germany, right now, the situation so far has shaped up to be cannabis vs. public health insurance. It is a mainstreaming trial drug in other words. For that reason, beyond any lingering but rapidly fading stigma, it is a fertile time to be in the middle of it, with a tech solution.

It is also perfect timing from the digitalization and privacy perspective. Unlike the U.S., Germany in particular has tended to keep its insurance services, certainly on the health front, undigitalized because of privacy concerns. That is no longer feasible from a cost perspective. It is also increasingly one that has to be dealt with from a tech and regulatory one.

Why Is CannabisIndustryJournal At DIA?

My nametag identifying me as both “media” and of a certain green source, was the source of endless discussion with everyone I talked to. Many attendees were extremely curious about why a cannabis industry publication was at an insurance conference. And most people, certainly the non-Germans in attendance, were unaware that per federal law, cannabis is now, at least in theory, covered by public health insurance here.

Medical insurance that treats cannabis just like “any other drug” is a discussion at the forefront of the medical community in Europe. Even if not at health insurance industry events like DIA. Yet. In the last year, in fact, Dutch insurers have started refusing to cover the drug as the German government moved forward on mandating coverage.

In other places, like Australia, Israel and Canada, the conversation is also proceeding, albeit slowly within the context of public health coverage.

However compliance and tracking of the drug itself, not to mention the need for research on how cannabis interacts with other drugs mandates a consideration of how digital health records, privacy and tracking can exist in the same conversation. And further, can be accessed by the insurance industry, the government and policy makers as reform moves into its 2.0 iteration – namely federal recognition of the drug as a legitimate medicine.

We at MedPayRx think we have one answer. And next year, we hope to present from the stage as we continue to move forward with engaging the insurance industry here on all such fronts. Not to mention helping move the conversation forward in other places. And of course, launching services.

Germany is proceeding down the path to officially grow its own medical cannabis crops. Medical use became legal this year, along with a federal mandate for cheap access. That means that public health insurance companies, which cover 90% of Germans, are now firmly on the hook if not front line of the cannabis efficacy issue. As such, Germany’s medical market is potentially one of the most lucrative cannabis markets in the world, with a total dollar amount to at least challenge, if not rival, even California’s recreational market. Some say Canada’s too.

However, before “home grow” enthusiasts get too excited, this legislative move was an attempt to stymie everything but commercial, albeit medical production. Not to mention shut off the recreational discussion for at least another four years.

How successful that foray into legalization will be – especially given the chronic shortages now facing patients – are an open question. Not to mention other infrastructural issues – like doctor unfamiliarity with or resistance to prescribing cannabinoids. Or the public insurers’ so-far reluctance to cover it even though now federally mandated to do so.

Regardless, Germany decided to legalize medical use in 2017 and further to begin a sanctioned domestic cultivation for this market. The decision in the Bundestag to legalize the drug was unanimous. And the idea to follow UN regulations to establish this vertical is cautiously conservative but defendable. Very predictably German in other words.

Since then, however, the path has been far from smooth. Much less efficient.

Trouble in Germany’s Medical Cannabis Paradise

In April the government released its tender bid. And no matter how exciting it was to be in the middle of an industry who finally saw a crack of light, there were also clouds to this silver lining that promised early and frequent thunderstorms on the horizon.

By the time the tender bid application was due in June, it was already clear who the top firms were likely to beIn fact, by the end of the ICBC conference, which held its first annual gathering in Berlin at the same time the bid tender was announced, the controversy was already bubbling. The requirements of the bid, for a laughably small amount of cannabis (2,000 kg), mandated experience producing high qualities of medical marijuana in a federally legitimate market. By definition that excluded all German hopefuls, and set up Canada and Holland as the only countries who could provide such experience, capital and backlog of crop as the growing gets started.

The grumbling from Germans started then.

However, so did an amazingly public race to gain access to the German market directly – by acquisition or capital expenditures that are not refundable easily (like real estate or even buyouts). The common theme? They were large amounts of money being spent, and made by major Canadian Licensed Producers who had the right qualifications to meet the standards of the bid. In fact, by the time the tender bid application was due in June, it was already clear who the top firms were likely to be. They were the only ones who qualified under the judging qualifications.

And while nobody would commit publicly, news of the final decision was expected by August. Several Canadian LPs even issued press releases stating that they were finalists in the bid. But still no news was forthcoming about the official list.

Delay, Delay and More Delay

A month later, as of September, and there was still no official pronouncement. Nor was anybody talking. BfArM, the regulatory agency that is supervising this rollout as well as the regulation of all narcotic drugs (sort of like a German version of the FDA) has been issuing non-statement statements since the late summer. Aurora, however, one of the top contenders for cultivation here, was quietly issued an ex-im license by both Canadian and German authorities. Publicly, this has been described as an effort to help stem the now chronic cannabis shortage facing patients who attempt to go through legitimate, prescribed channels. On the German side, intriguingly, this appears to be a provisional license. Privately, some wondered if this was the beginning of a backdoor approval process for the top scoring bid applicants for cultivation. Although why that might be remains unclear.

Whispered rumours by industry sources that wish to remain anonymous, have suggested that the entire bid is still hanging in jeopardy. Late in the month, rumours began to fly that there were now lawsuits against the bid process. Nobody had much detail. Not to mention specifics. But CannabisIndustryJournal can now confirm in fact that there have been two lawsuits (so far).

The summary of the complaints? It appears that two parties, filing with the “Bundeskartellamt” (or regulatory office focusing on monopolies and unfair business practices) did not think the bid process or scoring system was fair. And both parties also lost.

But as of mid-October, there is still no public decision on the bids. What gives?

Whispered rumours by industry sources that wish to remain anonymous, have suggested that the entire bid is still hanging in jeopardy. Even though the plaintiffs failed, some have suggested that the German government might force a complete redo. Others hint that it will likely be slightly revised to be more inclusive but the regulatory standards must remain. If a redo is in the cards, will the German government decide to increase the total amount of yearly cannabis to be delivered? At this point, it is only calling for 2,000 kg per year by 2019. And that, as everyone knows, is far too little for a market that is exploding no matter the many other obstacles, like insurance companies refusing to compensate patients.

What Is Behind The Continued Delays?

There are several theories circulating the higher levels of the cannabis industry internationally right now even if no one is willing to be quoted. The first is that the total number of successful applicants, including the recent litigants, will be slightly expanded, but stay more or less the same. There is a high standard here for the import of medical cannabis that the Germans intend on duplicating domestically.

The Comprehensive Economic Trade Agreement (CETA – the often controversial free trade alliance between Europe and Canada) is still in the final stages of approval.The second is that the German government will take its time on announcing the final winners and just open the doors to more imported product. This will not be popular with German insurers, who are on the hook to pay the difference. However with Tilray now on track to open a processing facility in Portugal and Canopy now aligned with Alcaliber in Spain, cross-continent import might be one option the government is also weighing as a stop-gap provision. Tilray, who publicly denied in the German press that they were participating in the cultivation license during the summer, just issued a press release in October announcing a national distribution deal to pharmacies with a German partner – for cannabis oil.

But then there is another possibility behind the delay. The government might also be waiting for another issue to resolve – one that has nothing to do with cannabis specifically, but in fact is now right in the middle of the discussion.

The Comprehensive Economic Trade Agreement (CETA – the often controversial free trade alliance between Europe and Canada) is still in the final stages of approval. In fact, on September 19, a prominent German politician, Sigmar Gabriel of the Social Democrats (SPD) made a major statement about his party’s willingness to support Germany’s backing of the deal. It might be in fact, that the German government, which is supportive of CETA, got spooked about the cannabis lawsuits as test trials against not cannabis legalization, but a threat to the treaty itself.

Quality control, namely pesticides when it comes to plant matter, and the right of companies to sue governments are two of the most controversial aspects of this trade deal. And both appear to have risen, like old bong smoke, right at the final leg of closing the cannabis cultivation bid.

Will cannabis be seen as a flagship test for the seaworthiness of CETA? On a very interesting level, that answer may be yes. And will CETA in turn create a different discussion about regulatory compliance in an industry that has been, from the beginning of this year, decidedly Canadian-Deutsch? That is also on the table. And of great concern to those who follow the regulatory issues inherent in all. Not to mention, of course, the industry itself.

Conclusions?

Right now, there are none to be had.

However at present, the German bid process is several months behind schedule as Canadian producers themselves face a new wrinkle at home – the regulation of the recreational crop in the provinces.

It is also clear that there are a lot of questions and not a whole lot of answers. Not to mention a timeline when the smoke will clear.

This website uses cookies so that we can provide you with the best user experience possible. Cookie information is stored in your browser and performs functions such as recognising you when you return to our website and helping our team to understand which sections of the website you find most interesting and useful.

Strictly Necessary Cookies

Strictly Necessary Cookie should be enabled at all times so that we can save your preferences for cookie settings.

We use tracking pixels that set your arrival time at our website, this is used as part of our anti-spam and security measures. Disabling this tracking pixel would disable some of our security measures, and is therefore considered necessary for the safe operation of the website. This tracking pixel is cleared from your system when you delete files in your history.

We also use cookies to store your preferences regarding the setting of 3rd Party Cookies.

If you disable this cookie, we will not be able to save your preferences. This means that every time you visit this website you will need to enable or disable cookies again.