The news is intriguing in a world overwhelmed with pandemic news. THC Global, a Canadian-Aussie company now raising money and signing global deals, has just bought a “clinic network” of 30 prescribing physicians that will be able to supply up to 6,000 Australian patients this year.

In doing so, this entity is clearly beginning to establish a pattern of expansion in a new medical market not seen so far outside of Canada. Namely being able to obtain the all-important prescription for one’s brand at the doctor or prescriber’s office which is affiliated with a certain producer. Pharmacies and dispensaries downstream have no discretion for any other product to sell if the brand is written right on the prescription itself.

And this marks a new step in an industry frustrated with the high prices and high levels of red tape in other international environments where more widespread medical cannabis reform has come.

The Situation in Germany Germany represents, so far at least, the destination market of choice for Canadian cannabis firms (for the last several years at least). This is for several very sound business reasons (at least in theory).

Photo: Ian McWilliams, Flickr

The German medical market is the largest in Europe. Health reforms which swept the country at the time of reunification also created a system that is in its own way a hybrid of the more European (and British) NHS and American healthcare. Namely, 90% of the German population is on the system, but it is tied to employment and income. Freelancers, even of the German kind, must use private healthcare as must all non-passport foreigners. If you make over a certain amount of money (about $65,000), you must also pay for private healthcare. As the cannabis revolution rolls forward, many cannabis patients are caught in changing rules and a great reluctance by public health insurers to allow fast entry of any new drug, including this one. This is based on “science” but also cost.

Bottom line? Yes, the market is lucrative and growing, and yes, cannabis is covered under public health insurance, but the ability of any producers to be able to maintain a reliable, steady market of “prescribers” is highly limited. Furthermore, unlike anywhere else in the world, pharmacists play an outsized role in the process – namely because there are no chains (more than four brick and mortar outlets are verboten). Prices and availability vary widely across the country.

There are also no “online” drug stores where patients can send prescriptions in the sense that this vertical has developed in other countries.

Hospital dispensation is, for all the obvious reasons, highly expensive and generally prohibitive for the long term, if not serving much larger numbers of patients.

The Problem in the UK Like Germany, the UK decided to launch medical “cannabis” – or at least cannabinoid-related drugs under the purview of the NHS, but there are several issues with this.

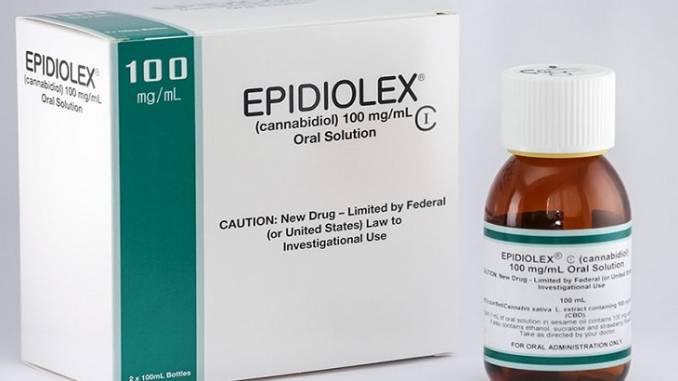

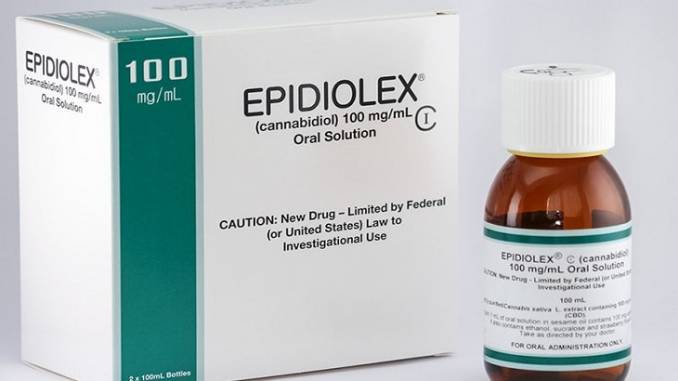

The problems start with the fact that the system remains a monopoly for one British company, GW Pharmaceuticals. The medication produced by them, including Sativex and Epidiolex is expensive and does not work for many patients that it is produced “on label” for (such as MS or childhood epilepsy).

And then of course, the largest group of cannabis patients anywhere (chronic pain) have been explicitly excluded from the list of conditions cannabis can be prescribed for under public health guidelines in the UK. This, like Germany, has created a highly expensive system where those patients who obtain the drug on a regular (and legal basis) have to have both private healthcare and obtain help through private clinics. While there are several chain clinics now forming in the UK, this is not the same thing as “buying” patients in the thousands – the model seen in Canada from the beginning of 2014.

The market has a lot of potential, in other words, but like Germany, via very different paths to market than seen in Canada, in particular.

Why Is Canada Different? The development of the medical market came through federal change in the law around the turn of the century. Namely, after patients won the right to grow for themselves, via Supreme Court legal challenge, patient collectives gradually formed to grow and sell cannabis that was more “professionally” cultivated. This, in turn, became the right of private companies and indeed household names in the Canadian market saw buying patient pools as their path to financing on the equity markets as of 2014.

This is not widely popular within the industry. Indeed, the last legal challenge mounted by the industry to ban non-profit patient collectives fell apart in 2016 – the year that the larger Canadian companies began to look abroad to Europe.

It is also undoubtedly why, beyond the red tape they face in Germany and the UK if not across Europe, Canadian firms are looking to hybridize a model which worked well for them at least in the early days of capitalization of the private industry. And maybe Australia will be “it.” Stay tuned.

Europe continues to be the new frontier of medical and wellness developments in the cannabis industry, with various sources predicting that Europe will become the world’s largest legal cannabis market over the next 5 years. Key related statistics, include:

A population of over 740 million (over double US and Canada combined)

Total cannabis market estimated to be worth up to €123 billion by 2028 (€58bn medical cannabis (47%), €65bn recreational cannabis (53%))

Over €500 million has been invested in European cannabis businesses (including significant expenditure in research and development, manufacturing and distribution)

To reiterate this belief, this month, hundreds of industry experts and delegates will be attending Cannabis Europa in Madrid, to discuss the expansion of cannabis across Europe and the challenges facing the industry across the member states of the EU and the UK.

Global mainstream leans to European strength

Since late 2018, major global operators have made substantial moves into the cannabis sector. Anheuser-Busch InBev, the world’s largest beer company and maker of Budweiser, entered into a partnership to research beverages infused with two types of cannabis. Constellation, owner of Corona beer, announced a commitment for $4 billion investment in Canadian cannabis company Canopy Growth. BlackRock Inc, through five actively managed BlackRock funds, has invested into Curaleaf Holdings Inc, a dispensary operator, for a not too insignificant investment sum of $11 million (as at March 2019). Such international investments prove that cannabis has moved from the fringes and into the mainstream.

When considering the impact of mainstream cannabis, it should be recognised that major European countries have approved or are planning on implementing, legalisation of medicinal cannabis. The UK, Germany, Italy and the Netherlands already have legal systems in place for medicinal cannabis and France and Spain are currently reviewing key legislative reform to align themselves with international practices. At present the German market is the third largest cannabis market (in terms of size) behind the US and Canada.

Member states of the EU, pre-Brexit

In addition to medicinal cannabis, several key European countries have systems in place, or are developing systems, or considering the reform of existing systems, to approve cannabis with THC content at a recreational level. The Netherlands already has a system and Luxembourg’s health minister in August 2019 announced the intention to legalise cannabis for Luxembourg residents. The Luxembourg government is lobbying EU member states to follow suit.

Whilst the EU has a labyrinth of laws in relation to edible CBD (as a novel food) which make the regulatory landscape complex, there has been an explosion of CBD products for vaping and cosmetics. Of course, with each of these products being subject to different local laws (some aligned between EU members states) in relation to vaping and cosmetic related regulations. The Brightfield Group has predicted a 400% increase in the European CBD market (including vaping liquid) from $318m in 2018 to $1.7 billion by 2023. There is also an expansion into applications for CBD with animals with many US manufacturers of CBD-infused pet food.

The European Parliament’s health committee has been calling for properly funded scientific research and there are motions to establish policies to seek to incentivise member states to advance the studies of medical cannabis, with a priority on scientific research and clinical studies – the first step necessary to drafting legislation, designed to better support the industry.

Where does the UK sit within cannabis?

Medicinal cannabis famously saw a legalisation, of sorts, by the then Secretary of State, Sajid Javid, who provided the authorisations for prescriptions for the high profile cases of Billy Caldwell and Alfie Dingley. Subsequently, on 1 November 2018, this was codified into law by an amendment to Schedule 2 of the 2001 Misuse of Drugs Regulations. This allows clinicians to prescribe cannabis as an unlicensed medicine.

There have, of course, been some high profile licensed medicines. The UK company, GW Pharmaceuticals, is the largest exporter of legal medical cannabis in the world, cultivating medical cannabis for production of cannabis-based medicines (e.g. Epidiolex & Sativex). Epidiolex (manufactured by subsidiary Greenwich Biosciences) became the first cannabis-derived medicine approved for use in the US for treatment of seizures caused by Lennox-Gastaut and Dravet syndromes (both severe forms of epilepsy).

When considering the level of research development and investment in the medicinal field, it is no surprise that the UK is the world’s largest producer and exporter of medical cannabis. Research published by the International Narcotics Control Board indicates that the UK produces over 100,000kg a year of medicinal cannabis.

Previous guidance from the National Institute for Health and Care Excellence (NICE) indicated that further research is required to demonstrate the benefit of medicinal cannabis, citing its cost versus evidenced benefit. However, there is now renewed confidence in the UK following NICE’s approval of two cannabis-based medicines produced by GW Pharmaceuticals, Epidiolex (cannabidiol) oral solution and Sativex (nabiximols), for routine reimbursement through the NHS.

Following the re-categorisation of medicinal cannabis in November 2018, a number of clinics have been established where specialised clinicians can start the process of prescribing cannabis based medicinal products (CBMPs). Whilst this route is not fast, and challenges are well documented as to the satisfaction of prescriptions made in the UK, there is momentum behind the development of this as a means for providing genuine and established medical care. A significant step in October 2019, was the CQC registration of one such cannabis clinic, Sapphire Medical Clinics Limited.

In November 2019, a project backed by the Royal College of Psychiatrists was announced with the aim to be the largest trial on the drug’s use in Europe with a target of 20,000 UK patients.

The UK medicinal cannabis sector is establishing a research-based approach to expand usage in the UK and across Europe.

How North America compares to Europe

Canada

Canada, as a first mover within the cannabis sector, has a multitude of large companies which are well-capitalised and have substantial international footprints. The Canadian exchanges have large listed companies looking to Europe with the intention of acquiring or investing into European operations. As of the date of writing, the 10 largest cannabis companies in Canada have an aggregate market cap of over $23.5 billion (and all registered cannabis companies in Canada having an aggregate market cap of over $46.5 billion).

Listed companies have had a tough time over the last 6-12 months with a slowdown in the market as a natural re-balancing occurs – part of which is due to rapid expansion and heavy investment into cultivation by all the major participants in the market. Over the next 6 -12 months we can expect to see management changes (some of which will be voluntary and some of which will be imposed by institutional pressure) to introduce different skill sets at board and senior management level to facilitate the oversight and leadership necessary for large pharmaceutical companies. Many operations have expanded into highly regulated products and complex supply chains whilst still operating with fundamentally the same team that established the operations with entrepreneurial efforts but, perhaps, a lack of experience in these sectors. The recent announcements by Aurora Cannabis and Tilray demonstrate that these restructurings and costs reductions have already commenced. However, with increased experience at board level and an improvement of profitability focused on sustainable business practices, should come new opportunities on a global scale for these North American operations.

The US

The US market, because of the complexity of state and federal laws not being fully aligned, is closer to its infancy than the Canadian market. This is not too dissimilar to the European market. That said, there are a number of well-funded and quite large US enterprises. A limited number of these, such as Tilray, are looking to expand into Europe.

Many of the companies in the US have, and continue to, expand quickly so we can expect to see a number of mergers and acquisitions. We are likely to witness Canadian and US entities merging with one another with the potential for acquisitions for operations within Europe. It is unlikely that the North American companies will risk their capital through organic growth so would be expected to be identifying “turnkey” solutions.

One of the major challenges facing US companies is the complexity of supply and distribution. This is largely a result of the complexities for state and federal laws interacting with one another as well as international importation and exportation with US states.

How you can invest within the UK and Europe

Developments in the fields of research and development are anticipated to add further weight to the lobbying of government and regulatory bodies across Europe.The UK remains, despite the events of Brexit, a major financial hub for Europe. The London market has seen the growth of several investment and operation cannabis companies. This includes private companies such as; EMMAC Life Sciences Limited and the operations formerly trading as European Cannabis Holdings (now demerged into several new entities including NOBL and LYPHE) as well as publicly listed companies; including Sativa Group PLC (the first publically listed cannabis specific company in the UK) and World High Life Plc, both operating on the NEX Exchange.

The Medical Cannabis and Wellness Ucits ETF (CBDX), Europe’s first medical cannabis ETF fund, domiciled in Ireland, and which has been passported for sale in the UK and Italy, has also caused a renewed stir within the market with a further platform for listed investment.

As the regulatory framework evolves further there is an anticipation that more medicinal cannabis and CBD related enterprises should have the opportunity to list on public exchanges, whether in the UK or in European countries.

Conclusion

Despite a period of slow down following the natural rebalancing of the fast-growing North American markets for the cannabis sector, there is renewed confidence in the expansion of the industry. Developments in the fields of research and development are anticipated to add further weight to the lobbying of government and regulatory bodies across Europe.

There is an increased push for a public dialogue and consultation in relation to medicinal and recreational cannabis in the UK, backed by several mainstream media platforms. This is likely to be shaped in some parts by national debates in Luxembourg and other European countries as they consider their own domestic laws.

With European parliaments across the EU (including the UK) hopefully having time freed up to discuss other political matters now that Brexit is progressing, the next 18 months should prove an exciting time within the European cannabis sector.

Tilray has long been seen as one of the market leaders in the global cannabis space. They are strategically placed in several critical areas to continue to do well, and put up major competition for just about everyone else (including German market entry first Canopy, plus the other big players in both Canada and Europe) ever since. See Aurora, Maricann and Aphria, to name a few. On the EU front, they are also certainly giving Dutch Bedrocan (with not only existing government contracts, but a newly increased ex-im medical allowance across the open Schengen border) a run for its money. And appear to have broached a monopoly long held by GW Pharma in the UK.

But first things first. Here is a brief list of accomplishments on the corporate CV so far.In the U.S., Tilray just scored a medical trial at the University of San Diego with a pill used to treat a nerve disorder.

Long (relatively speaking) before Europe was on the map for anyone but a couple of Canadian LPs, the company was exporting to Croatia (in 2016). Even the initial hiccups in delivery (a batch arrived in broken bottles), did not stop their foreign expansion plans.

When the first German cultivation bid was due, the company also, at least according to their spokesperson in Berlin at the time, considered applying. However, by late summer last year, Tilray was actually the first to publicly tip their hands that not only were they bowing out of the German tender, but had rather decided to import to Germany from cheaper EU climes. See their production facilities in Portugal. Plus of course a mass distribution deal to German pharmacies via local distribution.

Then there is their social media presence on Leafly, which also competes with Weedmaps as both an information portal and dispensary finder in key markets (California and Canada). TheGerman version of the website (Leafly.de), has created a reality, no matter where the server is located, of also connecting directly to patients in a market still finding its way.

Add all these elements together, and that puts the company behind it all in an unbelievably strong position to continue to gain both market access and market growth in multiple jurisdictions while carefully moving at literally the change if not bleeding edge of the law.

How much long term impact this will have, however remains to be seen. Why? The times are changing fast. And not everyone is following a policy of promotion timed around other large events (see Canadian recreational legalization and the timing of the company’s IPO).

Here is another example: the company’s most touted recent double victory, on each side of the Atlantic. Why? This is a place where cannabis companies are starting to compete. And while notable, particularly in it’s timing, is clearly indicative of the next stage in the development of the legitimate medical cannabis industry– not just Tilray.

Trials As Market Entry Tools

Medical trials in both the United States and Europe right now (including the UK for now at least), are the best way for cannabis companies to enter and gain market share. In the U.S., Tilray just scored a medical trial at the University of San Diego with a pill used to treat a nerve disorder.

Last week, Tilray also announced that they had essentially become the first Canadian LP to successfully challenge GW Pharmaceuticals on its home turf in the UK, even if for now limited to one patient application at a time. That won’t last, nor will such a tight monopoly.From a medical point of view, it is a very positive sign, at least for now.

That cross-Atlantic connection is even more interesting, however, given U.S. market entry recently for GW Pharmaceutical’s product, Epidiolex.

From a medical point of view, it is a very positive sign, at least for now. How it will end up in the future is anyone’s guess, including stock valuation.

Most advocates, of course, still hope for a medical market where patients are not restricted from deciding between the whole plant, oils or even the pharmaceutical products they choose to take.

Tilray of course is also not the only large LP engaged in medical trials. They are going on all over Europe right now (even if not as well strategically publicized). Health Canada is also committing to trials in Canada over the next five years.

However, what this very clearly demonstrates is that the global medical market is now ripe pickings for companies who approach the entire discussion from a “pharmacized” product point of view.Even if that means in Europe, and including for Tilray, entering the German and other medical markets with flower, oils and medical products.

In a fascinating early August conference call with Seeking Alpha, British-based GW Pharmaceuticals finally revealed their retail price point for CBD-based drug, Epidiolex, as it goes into distribution in the U.S.

The ineffectiveness of GW Pharma’s drugs for many patients (along with the cost charged for them) was responsible for pre-empting the entire access discussion in the UK this year. The mother of an epileptic British child tried to import a personal store of cannabis oil (produced by Canadian LP Tilray) only to have it confiscated at the airport this summer. Her son ended up in the hospital shortly thereafter.

The majority of this cost will not be picked up by private health insurers but rather the federal governmentActually, according to industry analysis, this is about 70% more than the price of one comparable drug (Onfi), and slightly more expensive than Banzel, the two competing (non-cannabinoid based) medications now available in the U.S. for this market.

Here is the other (widely unreported) kicker. The majority of this cost will not be picked up by private health insurers but rather the federal government, which is also not negotiating with GW Pharma about that high price (unlike for example what is going on in Europe and the German bid).

Why the difference?

Two reasons. The first is that Epidiolex has obtained “orphan drug” status (a medication for a disease that affects fewer than 200,000 patients in the U.S.) The second is that the majority of the insurance that will be picking up this tab is Medicaid. The patient pool will be unable to afford this. As a result, the bulk of the money will remit not from private insurance companies but rather federal taxpayers. And, unlike in say, Germany, none of this is pre-negotiated in bulk.

What is the price of Epidiolex? $32,500 per patient, per year.

Co-payments are expected to range from $5 to $200 per month per patient after insurance (read: the government) picks up the tab. This essentially means that the company plans to base participation at first at least on a sliding scale, highly subsidized by a government that has yet to reschedule cannabis from a Schedule I in the U.S.

Creating, in other words, a new monopoly position for GW Pharmaceuticals in North America.

A Hypocrisy Both Patients And The Industry Should Fight

The sordid, underhanded politicking that has created this canna monster is hardly surprising given the current political environment in both the U.S. and the U.K. right now. The people who benefit the most from this development are not patients, or even everyday shareholders, not to mention the burgeoning legitimate North American cannabis industry, but in fact highly placed politicians (like British Prime Minister Theresa May). Philip May, the PM’s husband’s firm is the majority shareholder in GW Pharma. Her former drugs minister (with a strong stand against medical cannabis) is married to the managing director of British Sugar, the company that grows GW Pharma’s cannabis stock domestically.

So far, despite a domestic outcry over this in the UK (including rescheduling), there has been no political backlash in the United States over this announcement. Why not?

Look To Europe For A More Competitive Medical Market

This kind of pricing strategy is also a complete no go in just about every other market – including medical-only markets where GW Pharma already has a footprint.

For example, German health insurers are already complaining about this kind of pricing strategy for cannabis (see the Cannabis Report from one of the country’s largest insurers TK – out earlier this year). And this in an environment where the government, in fact, does negotiate a bulk rate for most of the drugs in the market. Currently most German cannabis patients are being given dronabinol, a synthetic form of THC which costs far less.

On top of this, there are also moves afoot by the German government to begin to bring the costs of medical cannabis and medicines down, dramatically. And this too will impact the market – not only in Europe, but hopefully spark a debate in every country where prices are also too high.

The currently pending German cultivation bid for medical cannabis has already set an informal “reference” price of at most 7 euros a gram (and probably will see bid competitors come in at under half that). In other words, the government wholesale price of raw, unprocessed cannabis flower if not lightly processed cannabis oil is expected to be somewhere in the neighbourhood of 3-4 euros per gram come early next year. If not, as some expect, potentially even lower than that.

Processed Cannabis Medicine vs. Whole Plant Treatment

The debate that is really raging, beyond pricing, is whether unprocessed cannabis and cannabis oil is actually “medicine.” At the moment, the status quo in the U.S. is that it is not.

GW Pharmaceuticals, in other words, a British company importing a CBD-based derivative, is the only real “medical cannabis” company in the country, per the FDA. Everyone else, at least according to this logic, is placed in the “recreational camp.” And further, hampered still, with a lack of rescheduling, that affects everyone.

If that is not an organizing issue for the American cannabis industry, still struggling with the many issues inherent in the status quo (from insurance coverage and banking to national distribution across state lines) leading up to the midterms, nothing will be.

In American political lingo, an “October Surprise” is an event or incident that is deliberately planned to impact a political election – usually during a presidential year.

The cannabis industry, of course, is still highly political – starting with reform itself.

So what to make of the fact that over the course of the summer, three major markets have started to align in terms of timing?

Canada, Germany and The UK Moving In Synch?

None of these things were original, publicly planned or announced, of course. During July, the Canadian government finally announced the recreational market start date, the German government issued its new cannabis cultivation bid (due in October), and of course, the British government announced that they would reschedule cannabis and create more access for British patients.Canadian companies, for example, are perfectly poised to enter both markets and dominate the industry

What is in the air? And could this, in any way, be a deliberate cannabis industry power play by political forces in motion right now?

The Canadian-German Connection

Planned or not, it is certainly convenient that the much stalled German cultivation bid will now be due right at the time that the Canadian rec market goes into hyper drive. Why? The largest Canadian LPs are currently dominating the European market. These companies are also widely expected to take home the majority of the tender opportunities and are already producing and distributing across Europe.

For this reason, it is unlikely that there will be any “shortages” in the market in terms of deliverable product. However, larger Canadian cannabis companies have already announced that a certain percentage of their stock will be reserved for medical use (either at home or presumably to meet contract commitments that now stretch globally). Inefficiencies in the distribution network will be more responsible, at least in the short term, for consumer “shortages” rather than a lack of availability of qualified product.

Regardless, the connection between these two markets will generate its own interesting dynamics, particularly given the influence of both the Canadian producers and the size of the German medical space on cannabis reform as well as market entry.

The German-British Connection

Germany and the UK are connected historically, culturally, and now on the topic of cannabis reform. While it is unlikely in the short term that German-produced cannabis would end up in the UK, British grown cannabis products are available across Europe, including Germany, in the form of drugs developed by GW Pharmaceuticals.

In the future, given the interest in all things “export” in both economies, this could be a fascinating, highly competitive market space. Whether or not Brexit happens.

The British-Canadian Connection

While not much has emerged (yet) from these two commonwealth countries now embarking on the cannabis journey, it could certainly be an interesting one. This starts with the major competition GW Pharmaceuticals now faces at home from external (Canadian in particular) companies looking to expand their reach across Europe.

Whether Britain Brexits or not could also impact the pace of market development here. Particularly as cannabis supplies can be flown in (via Heathrow), or shipped via the Atlantic, thus missing the Channel crossing point and literally parking lot delays on major motorways.

Canadian cannabis companies could also decide to build production sites as the market matures in the UK.

As it emerged earlier in the year, the UK is also the world’s top cannabis exporter – ahead still of the entire Canadian export market. Do not expect this to last for long after October.

However, in one more intriguing connection between the markets, Queen Elizabeth II in the UK must sign the final authorization for the Canadian recreational market to commence. With a new focus on commonwealth economies,if Brexit occurs, cannabis could certainly shape up to be a major “commonwealth crop.”

Much like tea, for that matter.

The common language between the two countries also makes international business dealings that much easier.

But What Does This All Mean For The Industry?

The first indication of this synching phenomenon may well be simply market growth on an international level unseen so far.

Canadian companies, for example, are perfectly poised to enter both markets and dominate the industry simply because this odd calendrical synching is also very convenient for business,

British companies coming online in the aftermath of rescheduling will also be uniquely positioned, no matter the outcome of the now looming divorce agreement between the parties. Whether the first market beyond domestic consumption is either commonwealth countries or the EU (or both in a best case scenario), the British cannabis market is likely to be even more globally influential than it already is.

The German market may also, depending on the pace of patient growth and cultivation space, become the third big rival, particularly with the near religious fervour all exports are worshipped here.

In the more immediate future, Germany is actually shaping up to be the most international market. Established companies from Canada to Israel and Australia are clearly lining up to enter the market one way or the other. And all that competition is starting to predict a seriously frothy, if not expanding, market starting now with connections that stretch globally.

As August comes to a close, it is clear that it has been one busy quarter for market development – all over the place. Developments in the UK and Germany in particular, however, have been dramatic. In turn, this is also starting to bring other countries online – even as potential producers move in on the market and before real domestic medical reform has occurred (in countries ranging from Turkey to Spain).

And, say no more, Canada finally announced its “due date” in October.

How all three markets will move forward is also very interesting. They are all interrelated at this point, and even more intriguing, increasingly in synch.

This trend is also one advocates should take note of to push forward on further legislative and access issues going forward.

The EU looks poised to hop on the legalization train

In the future, no matter what happens with Brexit, developments in both the UK and Germany will continue to push the conversation forward in the EU, a region that is now the world’s most strategic (and globally accessible) cannabis market. Advocates, particularly in Canada and the U.S. right now, can also do much to support them.

Germany

Events here, while they may seem “slow” to outsiders, are in fact progressing – and as Cannabis Industry Journal has been reporting – quite fast even if the developments haven’t been (initially at least) quite as public. As this ‘zine wrote, breaking the news in July, the Federal German Drugs and Medical Devices Agency (BfArM) quietly posted the revised bid in July on a European tender site after refusing to confirm that it had sent out (undated) cancellation letters to previous hopefuls. Applicants for the new tender have until October 22 to respond. It is expected, given the new focus on “coalitions” that there will be many more applicants from global teams.

Even more interesting is the informal “reference price” that BfArM is appearing to set for bid respondents (7 euros per gram) and the impact of that on all pricing going forward across the continent.

Photo: Ian McWilliams, Flickr

Within a week, it also emerged that the Deutsche Borse, the organization that regulates the German stock exchanges, and working via its third party clearing arm, refused to clear any trades of any publically listed North American cannabis company that are also listed in Germany. This is an interesting development for sure – particularly now. How it will impact the biggest companies (read publicly listed Canadian LPs) is unclear, particularly because they can now raise capital via global capital markets – including the U.S.

Earlier in the summer, one of the largest public or “statutory” health insurance companies in Germany issued the “Cannabis Report.” It showed that cannabis has now moved out of “orphan drug territory” in Germany, and over 15,000 patients are now prescribed the drug. That said, over 35% of all claims are still being rejected. Most patients at this point, are also women older than 40.

The UK

It seems to be less than coincidence that the other big mover this quarter (and in fact most of the year) has been the UK. These two countries are linked by history and trade more than any other in Europe.

As of October, the country will not only reschedule cannabinoid-derived medicine to a Schedule II drug, but also allow more patients to access it. It is unclear how fast reform will come to a country in the throes of Brexit drama, but it is clear that this discussion is now finally on the table. What is also intriguing about this development is how far and fast this will open the door for other firms to compete, finally, with the monopoly enjoyed by GW Pharmaceuticals in the British Islands since 1998.

In one of the quarter’s biggest coups that stockholders loved but left the domestic industry with few illusions about the fight ahead, GW Pharmaceuticals also announced that it had managed (ahead of all U.S.-based producers and firms and even rescheduling in the U.S.) to gain U.S. federal government approval to import a CBD-based epilepsy drug (Epidiolex) into the United States from the UK and thus gain national distribution.

Canada

While it was more inevitable (and planned for) than developments in Euro markets, Canada also moved forward this quarter. There is now a set date for a recreational market start.

What is even more interesting is that the next formal “steps” in all three markets are now timed to coincide within weeks of each other in October this year.

Canadian producers of course are in the leading position to enter both German and British markets. Further their production centers now springing up all over Europe are supplying both their source markets and will be available for international distribution.

According to a press release, last week GW Pharmaceuticals’ drug Epidiolex received a positive FDA panel review, which is an encouraging and important step towards getting the drug approved by the U.S. Food and Drug Administration and on the market in the United States. Epidiolex is an anti-epilepsy drug, taken in a syrup form, with the main active ingredient being cannabidiol (CBD), and less than 0.1 % THC.

The drug is targeted to treat Dravet syndrome (DS) and Lennox-Gastaut syndrome (LGS) a rare early-onset type of epilepsy found in children, according to Reuters. FDA staff said the drug “reduces seizure frequency in patients with drug-resistant LGS or DS while maintaining a predictable and manageable safety profile.”

GW Pharmaceuticals, founded in 1998 and based in London, is a biopharmaceutical company that has made headlines previously for developing cannabis-derived drugs. Sativex, one of the first drugs they developed, is derived from cannabis, but was not approved by the FDA. It is however available in other parts of the world, such as the EU, Israel and Canada.

If Epidiolex actually gets approval by the FDA, it will be the first-ever cannabis-derived drug available via prescription in all of the United States. According to Justin Gover, chief executive officer of GW Pharmaceuticals, this is a momentous breakthrough for the company. “We are pleased by the Advisory Committee’s unanimous recommendation to approve Epidiolex, which would provide an important treatment option for patients with LGS and Dravet syndrome, two of the most severe and treatment-resistant forms of epilepsy,” says Gover “This favorable outcome marks an important milestone in our company’s unwavering commitment to address the significant unmet need for patients with LGS and Dravet syndrome and our resolve to study Epidiolex under the highest research and manufacturing standards. We look forward to our ongoing discussions with the FDA as it continues to review the Epidiolex NDA.”

According to the GW press release, the Peripheral and Central Nervous System Drugs Advisory Committee of the FDA unanimously recommended supporting the approval of the New Drug Application (NDA) for the drug. That advisory committee is sort of like an independent panel; their unanimous vote doesn’t necessarily mean the drug will get approved, but the FDA takes their decision into consideration when approving new drugs. So this panel recommendation is certainly a good sign and shows this drug could potentially be on the path to FDA approval.

The British Parliament considered a new right last Friday – the right of chronically ill patients to treat their conditions with cannabinoids. The bill to reform the law and allow medical use, the Legalisation of Cannabis (Medicinal Purposes) Bill 2017-19 was also re-read. It was first introduced last October.

While reformers at this point are loath to do any more than publicly hope, events in the UK continue to unfold in favour of reform.

This time, it is in the wake of a highly upsetting and embarrassing incident that further highlights the human toll of prohibition. When the British Home Office (a combination of the State Department, Homeland Security and a few other federal U.S. agencies) refuses cannabis oil to six year-old Britons with epilepsy named Alfie, don’t expect the famed stiff upper lip in response.

Not anymore.Why on earth would a home-grown company deny treatment to a British kid with epilepsy?

Especially not when the rest of the EU is moving forward, Canada and Australia (both countries are a part of the British Commonwealth) are now firmly in the medical camp with Canada moving ahead with recreational use this summer. Not to mention continuing reform on both fronts in many U.S. states. Even with setbacks that include the Trump White House and Justice Department (the recently dismissed federal case in New York being just the latest casualty), recreational reform in California is an international beacon of change that will not go quietly into the night. Not now.

One of the more interesting aspects of the Dingley case in the UK, in sharp contrast, is how fast Parliament responded to the plight of the six-year-old and his mother. Not only has Dingley’s medical import license been reconsidered in Parliament, but the matter appears to have finally galvanized significant numbers of the British elected class to do something about an appalling situation that affects hundreds of thousands, if not millions of Brits too.

Cannabis Medical Refugees

Medical refugee policy, especially around cannabinoids, is at least as controversial as the other kind. In Europe and the rest of the world, just like cannabis reform itself, these are national, not state issues as they have been in the U.S., (where the issue of cannabis patient state “refugees” has nonetheless been an issue for most of this decade).

Outside of the U.S., however, it is still the case that national governments can be embarrassed into reform with the right case (or groups of them).

GW Pharma said their product Epidiolex (for the treatment of childhood epilepsy) is being considered by the European Medicines Agency

That was certainly true in Israel in 2014, when the so-called “15 Families” threatened to emigrate from Israel to Colorado unless the government allowed them to treat their sick kids (federal government policy was changed within a month). Not to mention an internal, state to state migration of families in the United States to Colorado around the same time.

It may also be true in this latest British case. The Home Office has been embroiled in a few embarrassing take backs of late, mostly on the topic of immigration of people. The Alfie-Dingley cannabis case hits both medical cannabis reform and lingering buyer’s remorse over Brexit where the British people actually live (and on topics they actually care about).

Refusing at least medical cannabis rights in the UK might also well tip the scales in favour of a redo on Brexit. Or at least capture the support of people who still dream of that possibility. While the UK is still part of the continent, British citizens also have the right to travel freely, with medical rights intact, to other countries and get treatment. The British are no strangers to this idea (in fact, many British retirees end up in Spain and Greece for precisely this reason). Add cannabis to the mix, and current British policy looks even more out of step with reality and the wishes of the British people. Even the older, more conservative and “middle class” (read: American working if not blue-collar class) ones.

Local Production and Prohibition

And then of course, there is this irony. GW Pharmaceuticals, one of the oldest, cannabis companies in the world, is located in the UK. It even grows its own crops there, and has a special license from the British government to do so.

Worse, in this particular situation, it also is busy bringing several cannabinoid-based anti-epileptic drugs (for children and adults) to the market.

Why on earth would a home-grown company deny treatment to a British kid with epilepsy? And how could a government grant a license to a company to develop the plant for profit, but not a child who desperately needs the drug to live?

In a move that seems more than coincidence, GW Pharma also reported this week that their product Epidiolex (for the treatment of childhood epilepsy) is being considered by the European Medicines Agency, while a separate drug also bound for the epilepsy market called GWP42006 had just failed a Phase IIa trial for focal seizures.

The business press of course, has mostly reported that the only impact of this development so far of course, is that the company took a hit on share price.

It might do a bit more than that. Starting with legislative reform and ending with the sparking of significant home-grown (and legal) competition.

The combined impact of a failed trial in Eastern Europe by the only British company licensed and qualified to produce medicinal cannabinoids for any reason, and the plight of a British boy at home who needs precisely this kind of drug (and has so far been denied it), might in fact be the tinder match that lights political and market reform if not the development of a cannabis industry (finally) in Great Britain.

This website uses cookies so that we can provide you with the best user experience possible. Cookie information is stored in your browser and performs functions such as recognising you when you return to our website and helping our team to understand which sections of the website you find most interesting and useful.

Strictly Necessary Cookies

Strictly Necessary Cookie should be enabled at all times so that we can save your preferences for cookie settings.

We use tracking pixels that set your arrival time at our website, this is used as part of our anti-spam and security measures. Disabling this tracking pixel would disable some of our security measures, and is therefore considered necessary for the safe operation of the website. This tracking pixel is cleared from your system when you delete files in your history.

We also use cookies to store your preferences regarding the setting of 3rd Party Cookies.

If you disable this cookie, we will not be able to save your preferences. This means that every time you visit this website you will need to enable or disable cookies again.

The problems start with the fact that the system remains a monopoly for one British company, GW Pharmaceuticals. The medication produced by them, including Sativex and Epidiolex is expensive and does not work for many patients that it is produced “on label” for (such as MS or childhood epilepsy).

The problems start with the fact that the system remains a monopoly for one British company, GW Pharmaceuticals. The medication produced by them, including Sativex and Epidiolex is expensive and does not work for many patients that it is produced “on label” for (such as MS or childhood epilepsy).