By Abraham Finberg, Rachel Wright, Simon Menkes No Comments

In a move that Old Guard California Cannabis viewed with bittersweet appreciation, the Department of Cannabis Control on January 1, 2022 announced it would waive license fees for those cannabis companies impacted by the War on Cannabis. Many pre-2017 operators experienced persecution by law enforcement including confiscation of inventory. For those who refused to admit defeat and remained in or returned to the business of cannabis, this significant fee waiver feels something like an apology.

As we move through Year 2 of the Equity Fee Waiver, it’s important for all cannabis companies to review their history and their current operations to see if they qualify for this significant reduction in expense. Instead of arrest or conviction, a cannabis business may also qualify through its eligible owner’s income level or location of residence. Since this is a fee waiver for small businesses, a maximum yearly revenue level of $5 million is also a requirement.

For those Qualified Equity Licensees who have already received a fee waiver, it’s important to remember that this is a yearly process, and that they must continue to submit a request for equity fee relief at least 60 calendar days before the annual expiration date of their license.

Who Qualifies for the Equity Fee Waiver?

Gross Revenue: Your cannabis business must have no more than $5 Million gross revenue per year.

Equity Ownership: At least 50% of your business must be owned by people who have only ONE of these three characteristics:

Have experienced a cannabis conviction or arrest, or

Have a lower income level, or

Reside in a neighborhood affected by the criminalization of cannabis (as defined by the DCC)

Arrest or Conviction

The DCC requires that the equity individual have been convicted or arrested for cannabis crimes before November 8, 2016. Crimes must have been sale, possession, use, manufacture or cultivation. The equity individual may also be eligible if an immediate family member was convicted or arrested for cannabis crimes and the equity individual themselves lived in a California county with drug arrest rates that were higher than the state average drug arrest rates.

Residence in a Neighborhood Affected by Criminalization of Cannabis

If an equity individual seeks to qualify by location of residence, they must have lived in the qualified location for at least 5 years between 1980 and 2016. The location must have higher than state average drug arrests and be in the top 25% nationally for unemployment and poverty. The DCC provides an interactive map to check your location for these requirements.

Worth the Trouble

Again, your business needs to be below $5 million annual gross revenue, and at least 50% of the ownership needs to have only 1 of 3 disadvantaged characteristics: cannabis arrest or conviction, or lower income level, or residence in an affected neighborhood.

While it will definitely take time to apply for the Equity Fee Waiver, the savings in zeroed-out license fees can certainly make it worthwhile. In addition, qualifying for the Equity Fee Waiver makes a business eligible for other state equity tax advantages including the California Equity Tax Credit. (See our article on the CETC here.)

By Abraham Finberg, Rachel Wright, Simon Menkes No Comments

Cannabis companies representing 45% of California’s cannabis sales are pushing a bill that will crack down on non-paying customers. Well known operators, including Kiva, Lowell Farms, Nabis and Sunderstorm, recently formed Financial Stability for California Cannabis (FSCC) and moved to support Assembly Bill 766.”

The bill, nicknamed “The Cannabis Credit Protection Act,” would require a cannabis licensee to pay for goods and services sold or transferred by another licensee no later than 15 days following the final date set forth in the invoice. If full payment is not received by that date, the seller would be required to report this to the Department of Cannabis Control (DCC), which in turn would notify the delinquent buyer and begin disciplinary proceedings. The buyer would be prohibited from purchasing any other cannabis products on credit until the delinquent invoice was paid. In addition, the DCC would be empowered to issue a penalty (unspecified), taking into account “the frequency and gravity of the licensee’s [past] failure to pay outstanding invoices”.

In a letter of support for AB 766, the FSCC stated, “This culture of nonpayment that has emerged in California’s cannabis market leaves businesses across the entire industry and supply chain – as well as ancillary businesses that support legal cannabis operators – with outstanding balances and unpaid invoices sometimes totaling hundreds of thousands of dollars…This ballooning debt bubble in the cannabis industry will only continue to grow without proper oversight, putting the entirety of the state’s supply chain at risk of collapse and impacting state revenue decline even further.”

Opponents of the bill acknowledge the problem of non-payment in the industry, but feel AB 766 is too heavy handed and is “ripe for abuse.” In a blog post for the international legal firm Harris Bricken, cannabis attorney Griffen Thorne writes, “[L]icensees who are reported would be legally prohibited from buying goods or services on credit from other licensees until they pay the invoices for which they were reported in full … The person making the report has to give the DCC almost no information in order to make the report. There is no hearing. There does not even seem to be an opportunity to contest the report. The second a report is made, the other side loses its rights to buy goods on credit – presumably even under preexisting contractual arrangements with third parties. This seems like an obvious due process concern and ripe for abuse.”

The number and amounts of unpaid cannabis product invoices have ballooned over time and have driven California cannabis vendors to take such extreme measures. Collections and outstanding receivables are a symptom of an industry struggling under heavy taxes and competition from illegal operations that pay no taxes whatsoever, and which now account for over 60% of all cannabis sales within the state.

In order to ascertain the current status of AB 766, 420CPA reached out to Assemblymember Phil Ting (D-San Francisco), co-sponsor of the bill along with FSCC, the Cannabis Distribution Association, California Cannabis Industry Association and the California Cannabis Manufacturers Association. We corresponded with Tania Dikho, Ting’s Legislative Director. Ms. Dikho informed us that the bill was heard in the Assembly Appropriations Committee on May 18, but it was not passed.

“It’s a 2-year bill meaning we can’t act on it until this legislative year is over, so the bill will not have another hearing [and we] can’t make any changes to it until next year,” explained Ms. Dikho.

The 2-year status is a tenuous one. The bill must be approved by the Assembly and make its way to the Senate between early January 2024 and January 31, 2024 or it may no longer be acted upon and will die a legislative death.

Businesses that would like to voice their opinion for or against AB 766 should contact their state legislative representatives.

By Abraham Finberg, Simon Menkes, Rachel Wright No Comments

On January 27 this year, Matthew Lee, General Counsel for the Department of Cannabis Control, sent a letter to Senior Assistant Attorney General Mollie Lee requesting an opinion on whether “medicinal or adult-use commercial cannabis activity … between out-of-state licensees and California licensees, will result in significant legal risk to the State of California under the federal Controlled Substances Act.”

The eight-page letter, itself a detailed legal opinion in favor of interstate cannabis commerce, states strongly that the legal risk to California of such commerce is insignificant. The DCC hopes the AG will help authorize the state to negotiate agreements with other states, allowing their cannabis companies to do business with each other. Such agreements, the letter says, “would represent an important step to expand and strengthen California’s state-licensed cannabis market.”

Prices for wholesale cannabis in California have plummeted in the last year: a pound of packaged flower is wholesaling in the $1,200 to $1,400 per pound range compared with $1,700-$1,900 a pound at the beginning of 2022, a year-over-year decrease of about 25%-30%. With many growers struggling and many others forced to enter the illicit market to get a sustainable price for their product, the DCC believes opening up interstate opportunities for California growers will provide much-needed support for their large cultivation industry.

Additionally, this request by the DCC should serve as a roadmap for other states to follow in order to move interstate cannabis commerce forward through state legislatures since it appears that federal progress in legalizing cannabis has become mired in inaction.

The DCC cited new state legislation, Senate Bill 1326, which took effect on January 1, 2023, and which allows interstate agreements for both export AND import of cannabis. This is important because other states would not be inclined to enter an agreement with California if they could only receive (import) cannabis into what may be an already glutted market.

In drafting their letter, the DCC chose to side-step some “thorny” issues, including avoiding having the Attorney General delve into any discussion regarding the federal illegality of cannabis.

While many states to the east, including New York, New Jersey and Connecticut, are opening up their states to adult-use cannabis consumption, California is paving the way forward for the future of interstate cannabis commerce. The DCC’s letter is a bold move to support and strengthen California’s cannabis industry and will likely be watched closely by other cannabis states and the nation as a whole.

Jushi Holdings is a large multi-state operator with a massive national footprint and a presence in key markets, including Pennsylvania, Illinois, Virginia, Massachusetts, Nevada, Ohio and California.

About a year and a half ago, Aaron Green interviewed Andreas “Dre” Neumann, Chief Creative Director of Jushi Holdings to learn about his journey to the cannabis industry, Jushi’s market presence, brand development and key trends in the marketplace.

This time around, we’re checking in with Neumann to hear about his progress since the last time we spoke. In this interview, we delve deep into the world of creative influence, brand building, technology, what Neumann is working on now and what he is excited about in the future.

Cannabis Industry Journal: It’s been a while since our readers have heard from you. What’s new at Jushi? What Are you currently working on?

Dre Neumann: When I joined Jushi, we were building the foundation and laying the groundwork for a lot of the things we’re doing right now. One of them of course is our online pre-order platform. We have been focused on connecting all the dots in our vertically integrated markets to make sure our retail experience is really fine-tuned and represents what a diverse range of cannabis consumers find helpful and truly enjoy. In my time at Jushi, I have gained a much better understanding of the average cannabis consumer through constantly analyzing data from our retail spaces, and I very much look forward to analyzing more robust data that’s coming in through our new smartphone app.

Andreas Neumann, Chief Creative Director of Jushi Holdings

The data we have now is allowing us to look at what product developments are most important for us to move forward with and what product categories we should be focusing most on. Because we may be on the cusp of a recession, the consumer value of our product is that much more crucial. With the introduction of new categories of fast-acting edibles and unique and exciting genetics and types of flower, we are paying close attention to how we can innovate in ways that will both excite our current customers and attract new customers to our brands.

Jushi is interesting because the company really came together from two key pieces: the first being our strong financial and management backbone, and the second, the powerful creative team that I am a part of. We have such a special focus on the quality of products, with the goal of creating high-quality and consistency across our house of brands.

We have had a lot of acquisitions, which have played out very successfully over time, but early on, through these acquisitions, we found there were products and procedures that weren’t up to our standards. It takes time to fix those things from a quality, genetics and consistency perspective, and I’m thrilled to say we’re really getting there. Notably, we felt the need to improve our edible fruit chew brand, and we poured a ton of time into reinventing and relaunching simple, but high-quality, organic, 100% real-fruit chews.

Now, we are really seeing the value in our three retail brands and the unique attributes of our branded flower, pre rolls, vapes and edibles. Also, we have been really focusing on improving sustainability as we move towards using much more sustainable, standardized mylar packaging across our product suite. This packaging not only reduces our carbon footprint, as mylar is a much more sustainable, recyclable and lightweight material, but also offers us more real estate to express Jushi’s personality through artwork on packaging and allows us to display our products with a larger presence in stores.

CIJ: You mentioned Jushi’s new app and you sound so excited about it. Tell us more: how are you using the data to analyze what your customers want?

The Jushi app, The Hello Club (THC)

Neumann: When we were building our online platform, we knew we needed to better understand our customers. What we found was that the most important marketing tools in cannabis are promos – specifically promos through text messaging. Our loyalty program has become our biggest channel to reach consumers, as we have over 200,000 people we can reach with a simple text message. The big problem with texting campaigns, however, is that mobile phone carriers can limit your deliverability if you don’t have the right verbiage and messaging. So working with and figuring out how to deliver the right message to our customers can be very challenging.

Our smartphone app, The Hello Club (THC), came about as a natural progression of our customer loyalty program. Our team has a lot of experience working in UX and UI, so we were able to dive right in and build the app through Apple. We really took our time to build something that would add value to our customer, and it’s paid off. For instance, starting out we launched an exclusive weekly deal only available in the app. So, guess what happens? Just yesterday, on the 15th of November alone, 11,000 people downloaded the app.

Their retail location in Alexandria, Virginia

The app will be something that we play around and experiment with as more and more customers download it. It provides us with a platform to be creative and have fun with our customers, where we can launch exclusive events and strain drops and grant exclusive access to our products before they’re available to the general public.

The Hello Club was completely designed from scratch. It allows customers to choose their local, preferred store, with the ultimate goal of it becoming the central hub of their cannabis needs. The data we get from the app is so vast and there are so many opportunities on the horizon – we have only just scratched the surface. In the future, as we look to enter new markets, we’re excited to utilize the customer data from our app to guide us in deciding what to sell and where and create unique retail experiences tailored to each market. As we’re just in version 1.0, there’s tons of untapped potential ready to be unearthed and applied.

CIJ: Around this time last year you said that PA was the most important market for y’all. Tell me about the states that Jushi does business in. Are you paying particular attention to any market more now given the midterm elections?

Neumann: Yes, so Pennsylvania is still our most important market today, mainly because we have so many retail locations in the state (18). Pennsylvania is interesting because it’s also the site of Jushi’s first acquisition ever. I think the inevitable move from medical to recreational in the state will be extremely significant; it will be one of the greatest transitions in cannabis history. Because of our footprint and brand presence in Pennsylvania, we are in an excellent position for when adult use comes online.

The Palm Springs retail location

We call Virginia the sleeping giant because it’s a market we have really cornered. We will have six stores in northern Virginia, close to Washington D.C., in areas with large populations, very diverse demographics and a lot of young people. Our retail locations in the state are freestanding buildings with ample parking – key attributes that benefit customers and lift sales, as we found from the data we collected in Pennsylvania. Virginia has incredible potential because we have made such a formidable early presence with our vertically integrated, IKEA-sized grow operation there. We have applied our findings from other states to Virginia, and we’re thrilled about the opportunity for us to showcase high-quality products in this market.

California is such a tough market to be in, as it’s the most competitive cannabis market in the world, with some of the most discerning customers, so operators often fear entering the market. But it’s proven to be great for R&D for us, and we continue to learn how to navigate and work in this competitive market through our Palm Springs, Grover Beach and Santa Barbara retail locations. By necessity, we’ve been particularly creative with our marketing and operational strategies to carve a place in the market; we have to show people we have better products and a better experience, which is very difficult with stringent regulations in places like Palm Springs. So California, for us, continues to be a proving ground where we are learning how to be as competitive as possible, and this benefits Jushi as a whole.

The cannabis beverage market is expected to reach $2 Billion by 2026 and is growing at a rapid pace. In Canada, the market share of infused beverages grew nearly 850% since 2020, according to a recent Headset report, the trend is expected to follow in the States. Some traditional beverage companies are hesitant to jump in due to the niche branding and supply chain models needed to capture significant market share. Other adult beverage companies such as Vita Coco and Pabst are dipping their toes into the cannabis beverage market to capture early market opportunities.

Sales and marketing agencies like Petalfast, with a core team stemming from the natural foods and beverage industries, have already started cracking the code for cannabis brands by implementing systems straight out of those industry’s playbooks. This includes disrupting the CA market by becoming the first to implement a traditional three-tier distribution model.

We caught up with Jason Vegotsky, CEO of Petalfast to learn more about the cannabis beverage distribution market. Prior to Petalfast, Jason was Chief Revenue Officer at KushCo Holdings (now Greenlane Holdings), a role he took on after selling his butane supply company to KushCo.

Aaron Green: How did you get involved in the cannabis industry?

Jason Vegotsky, CEO of Petalfast

Jason Vegotsky: I began my career in wine and spirits distribution, but I always knew I wanted to work for myself. My first foray into launching a business, raising capital and brand building was through my beef jerky company, Lawless Jerky, which I built and sold after five years. Drawing on my food and beverage experience, I quickly entered and understood the cannabis market. I launched a company called Summit Innovations that sold butane to producers making oil. I eventually sold Summit to KushCo Holdings, Inc. (now known as Greenlane Holdings, Inc.) and became their President and Chief Revenue Officer. Through that experience, I began to notice gaps in the cannabis distribution model. Petalfast was built to fill that gap, providing clients with exceptional go-to-market strategies, leading to increased revenue and customer loyalty.

Green: How does experience in natural foods and traditional beverages translate to the cannabis industry?

Vegotsky: The route-to-market strategy is similar to that of cannabis, and the industry can benefit from the knowledge and experiences of those who work in natural foods and beverages. The extensive regulatory history and long-standing distribution models of these industries can provide a framework that those in the cannabis industry can capitalize on.

Green: What is the current distribution model for the majority of cannabis beverage companies today?

Vegotsky: Cannabis beverage companies face significant regulatory hurdles regarding distribution. Transportation restrictions, state-by-state differences in THC serving sizes and packaging requirements, retail display and storage limitations, and consumer adoption are just a few examples of what cannabis beverage brands run into when looking to enter, compete or scale in a given market.

At Petalfast, we offer a tiered distribution model, and our clients get phenomenal distribution through our logistics partner, Nabis. Products are circulated to all of California’s dispensaries and delivery services, allowing brands to focus on what matters most: creating the highest quality cannabis products on the market.

Green: What is a three-tier distribution model? Why do you think the cannabis beverage market is ripe for this model?

Vegotsky: The three-tier distribution model is commonly deployed by alcohol and other traditional food and beverage companies as it provides each tier to scale their operations and focus on their specific services. The three tiers include the brand, the wholesaler (sales + distribution), and the retailer in this distribution model. Because cash flow is such a significant challenge in the cannabis industry, adding an extra tier by separating your distribution and sales is advantageous to brands as it decreases overhead and allows brands to have the ability to scale.

Green: What are the opportunities for smaller brands looking to carve out a niche?

Vegotsky: One of the benefits of working in an emerging market is the opportunity to get in on the ground floor, learn as much as possible about the industry and find where gaps exist. Brand building in this space requires a deep understanding of the consumer and the overall culture — something that most brands are still trying to crack. If a smaller brand can effectively target a base within a distinct product category, it can be very effective in scaling within its niche.

Green: With big players from adult beverages dipping their toes in the cannabis beverage space, is consolidation inevitable?

Vegotsky: At a certain level, yes. Well-established companies will seek out acquisitions of smaller, successful companies, especially ones that are capital constrained, but buyers need to be aware that capital alone will not be enough. The culture of cannabis is very different from alcohol or other adjacent beverage categories, so the success of these big players in adult beverages will be linked to their ability to locate and understand the consumer and implement branding strategies accordingly. Adult beverage companies entering the cannabis market must also realize that the flow of product to retailers is not the same as in alcohol, so they will need to adjust accordingly. The cannabis-infused beverage market is expected to reach $2 billion by 2026, so alcohol companies looking to join this movement should start exploring their options now.

Green: What trends are you following in cannabis beverages? What does the future of cannabis beverages look like?

Vegotsky: Canna-tourism has grown to a $17 billion industry. With the rise in cannabis-infused beverages, we’re seeing an increase in creative consumption offerings, from tastings and food and beverage pairings to dispensary tours and bud-and-breakfasts.

Cannabis beverages are attractive to newcomers as they allow for easier control of the effects. Businesses that provide an experience similar to that of a wine or brewery tour can capitalize on new consumers looking to explore the benefits of cannabis in a controlled environment.

The modern consumer is also more health conscious, and with the increased availability of legal cannabis, many are replacing alcoholic beverages with the plant. There has been a reported decrease in alcohol consumption since the 1980s, and many now believe cannabis is safer than alcohol. This belief is especially prevalent among younger generations, leading to more users incorporating cannabis-infused beverages into their daily lives. How we socialize or unwind at the end of the day will start to look different, and brands will become market leaders by speaking to the varied needs of consumers.

Green: How does the industry get there?

Vegotsky: For one, federal decriminalization and removing cannabis as a Schedule I drug on the controlled substances list would help. Cannabis companies don’t have access to the traditional marketing playbook to promote their brands due to TV advertising and social media restrictions. To build brand awareness, businesses should focus efforts on the retail level. Engaging with consumers in-store allows brands to grab their attention and drive faster sales until other avenues open up. At Petalfast, we decided to invest in field and trade marketing to bring brands to life at the retail level. We do this better than anybody else, and we do it at scale.

Mergers and acquisition activity in the cannabis space tripled from 2020 to 2021, and that pace is on track to continue in 2022. With big players entering the global cannabis market, we’re fielding more questions about mergers and acquisitions of cannabis businesses.

In this guide, we look at the evolution of the U.S. cannabis industry and some best practices and considerations for M&A deals in this environment.

The New Reality of Cannabis M&A Activity

The industry has evolved since adult use cannabis was first legalized in some U.S. states in 2012. More cannabis companies have a professional infrastructure—legal, financial and operational—with executive teams and board members ensuring the organization establishes proper governance procedures. Investors and private equity firms are showing more interest, and some cannabis companies have celebrated their first IPOs on the Canadian Securities Exchange (CSE).

At the same time, we are seeing a kind of “market grab” by multistate operators (MSOs) looking to acquire various licenses and expand their market share. MSOs tend to understand the current state of the market. For example, in California and some other states, there is a surplus of cannabis on the market for various reasons, partially due to so-called “burner distribution”—rogue distributors using licenses to buy vast amounts of legally grown cannabis at wholesale prices and selling the product on the black market, thereby undercutting retailers and other legal cannabis businesses. Another reason for the surplus is simply the entrance of many legal cultivators into the market over the past year.

Due to these trends, MSOs are interested in acquiring the outlets to be able to sell the surplus cannabis within California and other new markets.

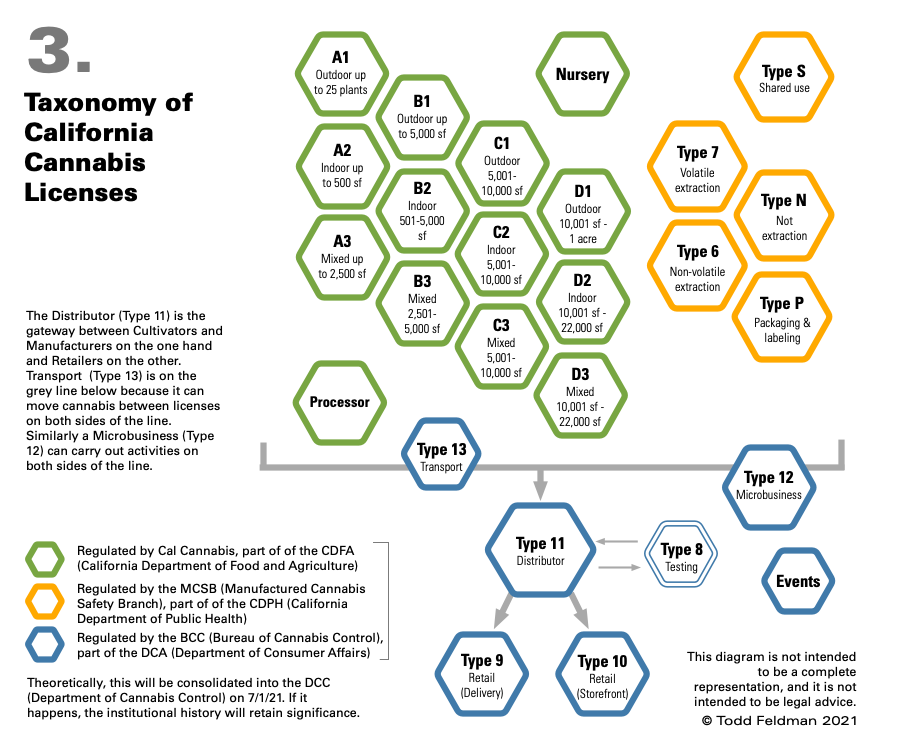

Transferring Cannabis License Rights

One of the biggest challenges to M&A activity in the cannabis sector is the difficulty of transferring or selling a cannabis license.

Different types of cannabis licenses in California

Cannabis licenses are not expressly transferable or assignable under California law and many other states. However, the parties involved aren’t without options. For example, a business that is sold to a new owner may be able to retain its existing cannabis license while the new owner’s license application is pending, as long as at least one existing owner is staying on board. At the state license level, a change of up to 20% financial interest does not constitute a change in ownership, although the Bureau of Cannabis Control (BCC) must be notified and approve the change.

This process can take a while—often a year or more—since licensing involves overcoming hurdles at the local level as well as the state level with the BCC. It’s crucial to talk with legal counsel about the particulars of the license and location early in the process to best structure the terms of the agreement while complying with state and local requirements.

Seeking a Tax-Free Reorganization in the Cannabis Space

In many cannabis mergers and acquisitions, the goal is to accomplish a tax-free reorganization, where the parties involved acquire or dispose of the assets of a business without generating the income tax consequences that would result from a straight sale or purchase of those assets.

IRC Section 368(a) defines various types of tax-free reorganizations, including:

In a stock-for-stock reorganization, all of the target company’s stock is traded for a portion of the stock of the acquiring parent corporation, and target company shareholders become minority shareholders of the acquiring company.

Often, it’s tough to meet the requirements to qualify for this type of tax-free reorganization because at least 80% of the target stock must be paid for in voting stock of the acquirer.

Additionally, companies may be saddled with too much debt. If the acquirer assumes that debt, it may be classified as consideration paid to the seller and therefore disqualify the transaction as a tax-free reorganization.

In other M&A deals, the acquiring corporation may be unwilling to assume the debt of the target corporation—perhaps because showing these items on its balance sheet would impact its debt-to-equity and other financial ratios.

Rather than acquiring the target company’s stock, the acquirer may purchase its assets. In a stock-for assets exchange, the buyer must purchase “substantially all” of the target’s assets in exchange for voting stock of the acquiring corporation.

A stock-for-assets format offers the buyer the benefit of not having to assume the unknown or contingent liabilities of the target. However, it’s only feasible if the acquirer purchases at least 80% of the fair market value of the target’s assets AND all or virtually all of the deal consideration will be stock of the acquirer.

Tax Consequences Arising from Sale of Assets

If the sale price doesn’t consist primarily of the buyer’s stock, the transaction may be a standard asset sale. This leads to very different tax results.

If the seller is a C corporation, it will typically face double taxation—paying tax once on the sale of assets within the corporation and again when those profits are distributed to shareholders. If the target company has net operating losses (NOLs), it can use those NOLs to offset the tax hit.

If the seller is an S corporation, it won’t have to pay corporate tax on the transaction at the federal level. Instead, shareholders will pay tax on the gain on their individual returns.

For the buyer, the benefit of an asset sale is that the assets acquired get a “step-up basis” to their purchase price. This is beneficial from a tax perspective, as the buyer can depreciate the assets and may be able to claim accelerated or bonus depreciation to help offset acquisition costs.

The subsidiary merges into the target company before liquidating,

The target company then becomes a subsidiary of the acquirer, and

The target company’s shareholders receive cash.

Structuring the deal this way may work to overcome the hurdle of transferring the license but may not qualify as a tax-free reorganization.

Bottom Line

The circumstances and motivations for mergers and acquisitions in the cannabis industry are diverse. As a result, there is no one-size-fits-all approach to structuring the transaction. In any event, it’s crucial to start the process early and seek advice from legal counsel and tax advisors to minimize the tax burden and ensure that both parties to the transaction get the best deal possible. If you need assistance, contact your 420CPA strategic financial advisor.

By Erik Paulson, Josh Swider, Zachary Eisenberg 5 Comments

Fraud

The THC content you see on a label when you walk into a dispensary? There is a very good chance the number is false.

In every state with regulated cannabis, there is a requirement to label the potency of products so consumers can make informed purchasing and medicating decisions. The regulations usually state that the THC/cannabinoid content on the label must be within a particular relative percent difference of the actual tested results for the product to be salable. In California, that threshold is +/- 10%.

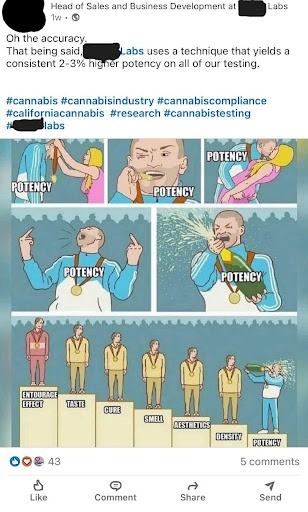

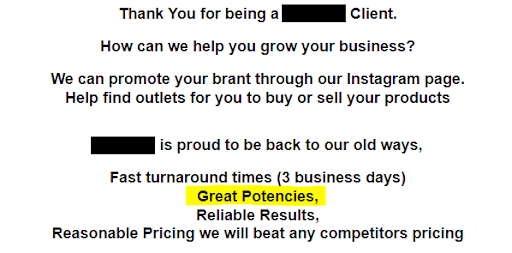

The problem is, with all the focus on THC percentage in flower and concentrate products, enormous pressure has been placed on cultivators and manufacturers to push their numbers up. Higher numbers = higher prices. But unfortunately, improving their growing, extraction and formulation processes only gets companies so far. So, they proceed to ‘lab shop’: giving their business to whichever lab provides them the highest potency.

There are roughly 50 Department of Cannabis Control (DCC) licensed labs in the state, and competition is fierce to maintain market share in a maturing and plateauing industry. Whereas competition used to be healthy and revolved around quality, turnaround time and customer service, now it’s essentially become a numbers game. As a result, many labs have sacrificed their scientific integrity to chase what the clients want: higher THC potency results without contaminant failures. The practice has become so prevalent that labs openly advertise their higher potency values to gain customers without fear of recourse. Here are two examples:

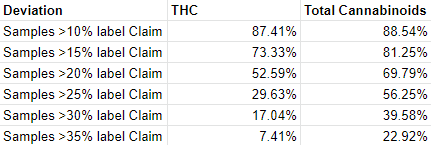

Over a year ago, a few labs fed up with what was happening got together to determine the extent of the potency inflation issue. We proactively purchased and tested over 150 randomly chosen flower samples off dispensary shelves. The results were staggering. Eighty-seven percent of the samples failed their label claims (i.e., were >10% deviant of their labeled values), with over half of the samples >20% deviant of their labeled THC values (i.e., over 2x the legal permitted variance). Additionally, our labs found multiple cases of unreported category 1 pesticides in some of the analyzed samples at multiple times the legal limit – a significant public health concern. The deceit was not limited to small cultivators trying to get by but also some of the industry’s biggest brands.

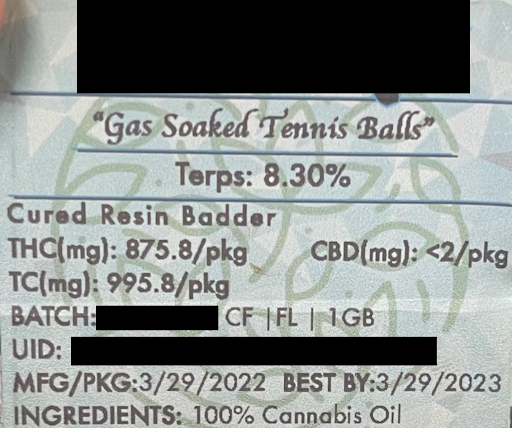

The same issues and economic conditions are in play for concentrates. Manufacturers of these products also hunt for the highest D9 THC values because wholesale prices for distillate are determined by THC content: <86% for the lowest value, 86-88%, 88-90% and >90%, with a new price point for over 94%. As a result, consumers can walk into a dispensary and find concentrates like the one shown below that report>99% total cannabinoids (>990mg/g) and contains almost 10% additional terpenes. You don’t have to be an analytical chemist to realize those numbers add up to well over 100%, which is physically impossible.

Blame

Everyone can agree that the system is broken, but who is at fault? Should the blame be placed on dispensaries, many of whom use THC % as their only purchasing or marketing metric? Or on cultivators, manufacturers and distributors, who seek the highest results possible rather than the most accurate ones? Or on the labs themselves, who are knowingly reporting inflated results?

Ultimately, the individual businesses are acting in their own self-interest, and many are participating in this practice simply to stay afloat. Dispensaries can’t reasonably be expected to know which results are inflated and which are not. Cultivators and manufacturers feel obligated to use labs that provide them with the highest results; otherwise, they’re putting themselves at a disadvantage relative to their competitors. Likewise, labs that aren’t willing to inflate their numbers have to be ready to watch customers walk out the door to maintain their principles – an existential dilemma for many.

The primary reason why potency inflation has become so prevalent is that there have been no negative repercussions for those that are cheating.

The axiom is true – don’t hate the player, hate the game. Unlike most businesses, testing labs operating with integrity want meaningful regulations and oversight to assure a level playing field. Without them, the economics force a race to the bottom where labs either have to inflate more and more or go out of business. Since 2016, the DCC (formerly BCC) has taken zero meaningful actions to discourage or crackdown on potency inflation— not a single recall of an inflated product or license suspension of an inflating lab— so predictably, the problem has gotten progressively worse over time.

So, to answer the question above – who is at fault for our broken system? The answer is simple: the DCC.

Inaction

In the Fall of 2021, we began engaging with the DCC to address the industry’s potency inflation concerns. The DCC requested we provide them with direct evidence of our accusations, so we collected and shared the flower data mentioned above. The Department tested the same batches off the shelf and confirmed our results. Somehow not a single recall was issued – even for the batches containing category 1 pesticides.

We pushed for more accountability, and DCC Director Nicole Elliott assured us steps were being taken: “The Department is in the process of establishing a number of mechanisms to strengthen compliance with and accountability around the testing methods required of labs and will be sharing more about that in the near future.”

Instead, we got a standardized cannabinoid potency method (mandated by SB 544) that all labs will be required to use. On the surface, a standardized methodology sounds like a good thing to level the playing field by forcing suspect labs into accepting generally accepted best practices. In reality, however, most labs already use the same basic methodology for flower and concentrate cannabinoid profiling and inflate their results using a variety of other mechanisms: selective sampling, using advantageous reference materials, manipulating data, etc. Furthermore, the method mandated is outdated and will flatly not work for various complex matrices such as gummies, topicals, beverages, fruit chews and more. If adopted without changes, it would be a disaster for manufacturers of these products and the labs that test them. Nevertheless, the press release issued by the DCC reads as though they’ve earned a pat on the back and delivered the silver bullet to the potency inflation issue.

Here are a few more meaningful actions the DCC could take that would help combat potency inflation:

Perform routine surveillance sampling and testing of products off of store shelves either at the DCC’s internal lab or by leveraging DCC licensed private labs.

Recall products found to be guilty of extreme levels of potency inflation.

Conduct in-person, unannounced audits of all labs, perhaps focusing on those reporting statistically higher THC results.

Conduct routine round-robin studies where every lab tests the same sample and outliers are identified.

Shutdown labs that are unable or unwilling to remediate their potency inflation issues.

For some less disciplinary suggestions:

Remove incentives for potency inflation, like putting a tax on THC percentage

Set up routine training sessions for labs to address areas of concern and improve communication with the DCC

Fight

Someone might retort – who cares if the number is slightly higher than it should be? No one will notice a little less THC in their product. A few counterpoints:

Consumers are being lied to and paying more for less THC.

Medical cannabis users depend on specific dosages for intended therapeutic effects.

Ethical people who put their entire lives into cultivating quality cannabis, manufacturing quality products and accurately testing cannot compete with those willing to cheat. If things get worse, only the unethical actors will be left.

Labs that inflate potency are more likely to ignore the presence of contaminants, like the category 1 pesticides we found in our surveillance testing.

This single compound, delta-9 THC, is the entire reason why this industry is so highly regulated. If we are not measuring it accurately, why regulate it at all?

We will continue to fight for a future where quality and ethics in the cannabis industry are rewarded rather than penalized. And consumers can have confidence in the quality and safety of the products they purchase. Our labs are willing to generate additional surveillance data, provide further suggestions for improvement in regulations/enforcement, and bring further attention to this problem. But there is a limit to what we can do. In the end, the health and future of our industry are entirely in the hands of the DCC. We hope you will join us in calling on them to enact meaningful and necessary changes that address this problem.

Cannabis, we have a problem. Legalizing adult use cannabis in California caused the demand for high-potency cannabis to increase dramatically over the last several years. Today, many dispensary buyers enforce THC minimums for the products that they sell. If smokeable flower products don’t have COAs proving the THC levels are above 20% or more, there is a good chance many dispensaries won’t carry them on their shelves. Unfortunately, these kinds of demands only put undue pressure on the industry and mislead the consumer.

Lab Shopping: Where the Problems Lie

Lab shopping for potency analysis isn’t new, but it has become more prevalent with the increasing demand for high-potency flower over the last couple of years. Sadly, many producers submit valid, certified COAs to the California Bureau of Cannabis Control (BCC), which show two to three times the actual potency value.

At InfiniteCAL, we’ve purchased products from dispensary shelves and found significant discrepancies between the analysis we perform and the report submitted to the BCC by the producer. So, how can this happen? Several factors are creating the perfect storm in cannabis testing.

Problems with Potency

Many consumers still don’t understand that THC potency is not the only factor in determining quality cannabis, and they are unwittingly contributing to the demand for testing and analysis fraud. It is alarming for cultivation pioneers and ethical labs to see producers and profit-hungry testing facilities falsifying data to make it more appealing to the unaware consumer.

Basically, what’s happening is growers are contacting labs and asking, “I get 30% THC at this lab; what can you do?” When they see our COA reporting their flower tested lower than anticipated, they will go to another lab to get higher test results. Unfortunately, there are all too many labs that are willing to comply.

I recently saw a compliant COA that claimed that this particular flower was testing at 54% THC. Understanding cannabis genetics, we know this isn’t possible. Another product I reviewed claimed that after diluting an 88% THC distillate with 10-15% terpenes, the final potency test was 92% THC. You cannot cut a product and expect the potency to increase. Finally, a third product we reviewed claimed 98% total cannabinoids (while only looking at seven cannabinoids) with 10% terpenes for a total of 108% of the product.

These labs only make themselves look foolish to professionals, mislead laymen consumers and skirt under the radar of the BCC with basic mathematical errors.

The Pesticide Predicament

Frighteningly, inflating potency numbers isn’t the most nefarious testing fraud happening in the cannabis industry. If a manufacturer has 1000 liters of cannabis oil fail pesticide testing, they could lose millions of dollars – or have it retested by a less scrupulous lab.

Photo: Michelle Tribe, Flickr

As the industry continues to expand and new labs pop up left and right, cultivators and manufacturers have learned which labs are “easy graders” and which ones aren’t. Certain labs can miss up to ten times the action level of a pesticide and still report it as non-detectable. So, if the producer fails for a pesticide at one lab, they know four others won’t see it.

In fact, I’ve had labs send my clients promotional materials guaranteeing compliant lab results without ever receiving a sample for testing. So now, these companies aren’t just tricking the consumer; they are potentially harming them.

An Easy Fix

Cannabis testing is missing just one critical factor that could quickly fix these problems – checks and balances. The BCC only needs to do one of two things:

Verifying Lab Accuracy

InfiniteCAL also operates in Michigan, where the Marijuana Regulatory Agency (MRA) has already implemented a system to ensure labs are maintaining the highest testing standards. The MRA will automatically flag all COAs which test above a certain percentage and require the product to be retested by multiple labs.

Labs are required to keep a back stock of material. So, when test results come back abnormally high from Lab A, then Labs B, C and D are commissioned to retest the material to compare data. If Lab A reports 40% THC, but the other labs all report 18%, then it’s easy to see Lab A has made an error.

Secret Shopping

By simply buying products off the shelves and having them blind-tested by other labs, it would be simple for the BCC to determine if the existing COA is correct. They already have all the data in Metrc, so this would be a quick and easy fix that could potentially solve the problem overnight.

For example, at InfiniteCAL, we once purchased 30 samples of Blue Dream flower from different cultivators ranging in certified COA potencies from 16% to 38%. Genetically, we know the Blue Dream cultivar doesn’t produce high levels of THC. When we tested the samples we purchased, nearly every sample came back in the mid-teens to low 20% range.

Labs Aren’t Supposed to Be Profit Centers

At InfiniteCAL, we’ve contacted labs in California where we’ve uncovered discrepancies to help find and flush out the errors in testing. All too often, we hear the excuses:

“If I fix my problem, I’ll lose my clients.”

“I’m just a businessman who owns a lab; I don’t know chemistry.”

“My chemist messed up; it’s their fault!”

If you own a lab, you are responsible for quality control. We are not here to get rich; we are here to act as public safety agents who ensure these products are safe for the consumer and provide detailed information about what they choose to put in their bodies. Be professional, and remember you’re testing for the consumer, not the producer.

Part One of this series took a look at how the regulated cannabis market can only be understood in relation to the previous medical market as well as the ongoing “traditional” market. Part Two of the series describes how regulation defines vertical integration in California cannabis.

If you are considering getting involved in California cannabis, imagine the following sentence in ten-foot-tall letters made out of recently ignited $20 bills:

Before you put any money down on property, carefully examine the local cannabis ordinance and tax rates.

This article is written in the form of advice to a newbie cannabis entrepreneur in California, but it will discuss issues that are also of significance to investors, as well as (to various degrees) cannabis entrepreneurs in other states.

Here are seven basic questions that you need to ask about local regulations (in order, except for Number 7).

1. What’s Your Jurisdiction?

If you’re in city limits, it’s the city. If you’re outside city limits, it’s the county.

2. Does the Jurisdiction Allow Cannabis Activities?

If the answer is yes, go to the next question. If the answer is no, pick another jurisdiction.

3. Where Does the Jurisdiction Allow Cannabis Activities?

A zoning ordinance will limit where you can set up shop. The limitation will probably vary by license type.

4. How Does the Local Ordinance Affect Facility Costs?

The short answer is: in many ways. Your local ordinance is a Pandora’s box of legal requirements, especially facility-related requirements.1 Read your local cannabis ordinance very carefully.

Generally speaking, the cannabis ordinance will set out two types of requirements – those that are specific to cannabis and those that apply generally to any business.

Looks great but . . . where are the sprinklers? Does it need a seismic upgrade? How about floor drains? Photo by Wilhelm Gunkel on Unsplash

Cannabis-specific requirements:

Typically incorporate state cannabis laws by reference.

Have significant overlaps with state cannabis laws. For example, the state requires commercial-grade locks and security cameras everywhere cannabis may be found on a given premises. Local ordinances generally include similar requirements – keep in mind that you will need to comply with a combined standard that satisfies both state and local requirements.2

Vary greatly according to type of activity. For example, manufacturers will need to comply with Health & Safety Code requirements that can have a major impact on construction costs.

Vary greatly by jurisdiction when it comes to equity programs.

General requirements:

Include by reference building and fire codes, which can require very expensive improvements. Note that this means your facility will be inspected by the building department and the fire department.

Can include anything from Americans with Disabilities Act (ADA) requirements to city-specific requirements, such as Design Guidelines.

Will be zealously enforced because you’re a cannabis business.

5. What is the Enforcement Policy?

It may be that your local jurisdiction will give you temporary local authorization after meeting some, but not all, of the requirements. For example, you may be able to begin operations once you’ve provided your city or county with your cannabis permit application, a zoning clearance and a business permit. In this jurisdiction, you would be able to bring your building up to code sometime after you begin operations.

On the other hand, your local jurisdiction may require you to meet every requirement – from cannabis-specific security requirements to general building code and ADA requirements – before you can begin operations. Depending on the type of cannabis business (and facility condition), this might be inconsequential. Or it might mean that you will have to pay more than a year’s worth of rent (or mortgage) before you can start making money.

6. Can You Choose a Facility That Saves You Time and Money?

Of course, you won’t have to spend much time or money bringing your facility up to code if it’s already up to code. How likely it is that you will find such a facility varies wildly according to the type of cannabis activity in question. In general:

Service-side activities (delivery retail, storefront retail, distribution) are in many respects similar to their non-cannabis counterparts. From a facilities standpoint, the major differences come from security requirements. So, it may be possible to save time and money by choosing a facility that is already up to code for a similar use.

Manufacturing activities are trickier, since you will need food-grade facilities and equipment. You may be able to save money by setting up shop in a commercial kitchen.

Extraction with volatile solvents is a special (and particularly expensive) case, since it is inherently dangerous and requires special facilities.

Outdoor cultivation may be relatively unproblematic if it has an appropriate water source.

Indoor cultivation is expensive because of climate-control and lighting requirements. Buildings potentially suitable for large-scale indoor grows frequently come with significant problems. Former warehouses will typically require major power upgrades, while former factories may have inconvenient architecture and/or hidden toxic waste. In all cases, internal reconstruction is likely to be necessary, and will trigger all sorts of building and fire code requirements.

7. What Are the Local Cannabis Taxes?

Cannabis tax rates may be determinative. For example, Oakland imposes a 6.5% gross receipts tax on manufacturers that have gross receipts of less than $5M, and 9.5% on manufacturers that have gross receipts over $5M. In comparison, Santa Rosa only imposes a 1% gross receipts tax on manufacturers.

Local cannabis ordinances and taxes can make or break your business, so you need to understand them before you commit to a location. The seven basic questions listed above are designed to get you started.

This article is the opinion of the author and is not intended to be legal or other advice.

Flower continues to be the dominant product category in US cannabis sales. In this “Flower-Side Chats” series of articles Green interviews integrated cannabis companies and flower brands that are bringing unique business models to the industry. Particular attention is focused on how these businesses navigate a rapidly changing landscape of regulatory, supply chain and consumer demand.

Connected is a vertically-integrated cannabis company based out of Sacramento, CA and one of the most sought-after brands in California and Arizona. Having formed as a legacy operation in 2009, Connected has created a cult-like following over more than a decade in business. According to BDS Analytics, Connected Cannabis and their acquired brand Alien Labs now boasts the highest wholesale flower price in any major legal market – their average indoor flower wholesale price is 2x the CA average – yet also has the highest flower retail revenue.

We spoke with Sam Ghods, CEO of Connected to learn more about his transition from tech to cannabis, how Connected thinks about product and his vision for future growth. Sam joined Connected in 2018 after getting to know the founders. Prior to Connected, Sam was a co-founder at Box where he stayed on for 3 years after their successful IPO.

Aaron Green: How did you get involved in the cannabis industry?

Sam Ghods: I originally came from the tech industry. I co-founded Box, a cloud sharing and storage company, in the mid 2000s with three other friends. We grew that from the four of us to eventually a multi-billion-dollar public offering in 2015. I stayed on a few more years after that until I took some time off trying to decide what I wanted to do next. I looked at a number of different industries and companies, but personally I always had a real passion for artisan and craft consumer goods. It’s a really big hobby of mine. Whether it’s going to Napa or learning about different kinds of premium consumer goods, I really had a deep love and never knew cannabis could be like that.

When I first met Caleb, the co-founder of Connected, he instantly got my attention by telling me that they had been selling out of their product in the volume of millions of dollars a year at more than two times what everybody else was selling for. That really piqued my interest because creating a product that has that level of consumer passion and demand is maybe the single hardest thing about building a consumer goods business. For them to have been so successful in what was a very difficult and gray market to operate in at the time – this was mid 2018 that I was speaking with him and he had been building this company since 2009 – is a really big challenge, and really impressive.

Sam Ghods, CEO of Connected

So, I started spending time with Caleb and the Connected team and learned a lot about the business. Everything I learned got me more interested and more excited. The way that they thought about the product, the way they treated it was with a reverence and level of sophistication I had no idea was possible.

I was so excited to just learn about the space. I mean, honestly, it feels like the internet in the 90’s- The sheer possibility and excitement. The only difference here is that the market already has existed for 100 years plus: the gray and underground markets for this product are actually phenomenally mature. And now we’re lifting up billions of dollars in commerce that’s already occurring and attempting to legalize all of it in one fell swoop, which creates such an interesting set of challenges.

I first got involved as an advisor on fundraising and strategy. And then a few months later, they were looking for a CEO and I joined full time as CEO in September 2018.

Aaron: What trends in the industry are you focused on?

Sam: It may seem basic, but I think product quality in the broader cannabis markets nationally and internationally is really underrated. Because of the extreme weight of the regulatory frameworks in so many different markets, it’s resulting in a lot of product being grown and sold just because it can be by the operators that are doing it. In many markets, they count the number of producers by the handful, instead of being measured in hundreds or thousands like in California or Oregon. And in that kind of environment, you’re not really having competition, and you’re not really able to see the quality that has existed in this category for years and years and years.

That’s one of the things that really sets us apart – the quality is first above all else, as well as the innovation and time that has gone into it, and not many existing brands in the legal market can say that. With some of the “premium” brands on the market, it would be comparable to just jumping into the wine industry one day and thinking that you can become a premium brand, without having any knowledge of the history of the product or the industry itself. At Connected, we have a team that’s been doing this for over a decade. We did a back of the envelope calculation: there’s over one thousand lifetime harvests between our team. We’ve also brought in specialists from Big Ag and other industries to complement that experience.

Cannabis is a very, very difficult plant to grow at a very high level. It’s much more like high-end wine or spirits than other fruit or produce. I think in the cannabis community, that’s extremely acknowledged, and appreciation for that is the reason we get by with the highest prices in the legal market. I think in the broader investor and financial community, this point hasn’t really hit home, because the limited license markets aren’t mature enough, and there isn’t enough competition in many of them.

Our focus is continuing to make the best product we can, which has fed and developed our brands [Connected and Alien Labs] into what they are today. That is our number one focus, and we think it’s pretty unique to the space of not just cultivating a great quality product, but also as far as breeding, pushing the bar higher and higher on what can be done with the genetics of the plant.

Aaron: How do you think about choosing testing labs?

Sam: So, the number one criterion is responsibility and compliance. We must be completely confident that they’re testing accurately, safely and exactly to the specifications of the state. Then from there, it is really cultivating about a partnership. There’s a lot of nuance in the relationship with a testing lab. We note things like: Are they responsive? Are they sensitive to our needs in terms of either timelines or requirements we have? It does come down to timelines and costs to a certain extent, like who’s able to deliver the best service for the best cost, but it really is a partnership where you’re working together to deliver a great product. Reliability and consistency are big pieces as well.

Aaron: Industry estimates for illicit market activities are something like 60% of the California market. From your perspective, how do we fix that?

Sam: I think it probably comes down to funding for the efforts to discontinue those activities and opening up the barrier to entry, incentivizing “illegal” operators to make the investment in the cross-over. I think the most successful attempts to tamp it down was when there were initiatives that were well-orchestrated and well-funded, allowing for legacy growers to actually cross over to the “legal” industry. You can’t launch an industry with such an extreme amount of regulation, set a miles-high barrier to entry, and then penalize legacy growers for continuing their business as-is. If the illicit market continues to be fueled by rejection, you’re not going to achieve the tax revenue that you’re expecting to see, that we all want to see. There needs to be an attitude that every dollar put into transitioning illicit markets into regulated markets is returned many times over in tax revenue to the state’s citizens.

Aaron: So, I understand you sell wholesale. Do you sell direct to consumer?“Once they hit the shelves, we blow people away again, beyond their expectations of what they had before.”

Sam: We own and operate three retail stores, so we do sell direct to our consumers, but at this point the majority of our product is sold through third party dispensaries.

Aaron: Do you make fresh frozen?

Sam: We do. On the cultivation side we have indoor, mixed light and outdoor. We fresh freeze a portion of our outdoor harvest every year, and then we use that fresh frozen for our live resin products, for example, our recent live resin cartridge. It creates a vape experience really unlike any other because we are using our regular market-ready flower, but instead we’re taking that flower and actually extracting, not just using the distillate and mixing a batch of terpenes with it. We extract the entire plant’s content across the board, from cannabinoids to terpenoids and everything in between, and then you have our live resin cartridges.

Aaron: How do you think about brand identity and leveraging the brand to command higher prices?

Sam: The cycle we’ve effectively created is that every time we do a release of a new strain or a new batch or harvest, the quality is generally going up. That quality is released under our brands, and then the customer is able to associate that increase in quality and reputation with those brands. Then for our next launch, we have an even bigger platform to talk about the products and to ship and distribute and sell the products. Once they hit the shelves, we blow people away again, beyond their expectations of what they had before. That continuous cycle keeps fortifying the brand and fortifying the product. From our perspective the brand is built 100% on the quality of the product. The product will always be our highest priority and the brand will come downstream from that.

Aaron: Tell me about Alien Labs.

Sam: Alien Labs was an acquisition. It was a company that had built their brand really successfully in the gray market through 2017 and Prop 215 in California and had an incredible level of quality, a really loyal and dedicated fan base, not to mention a tremendous Instagram presence and following, which is where 98% of cannabis marketing happens today. We really loved the spirit of what the founders were bringing to the table. In 2018, we decided basically to join forces with them and bring them on board, creating a partnership where they leverage our infrastructure and the systems and processes we’ve built, but still keep their way of cultivation and their product vision. To this day, Ted Lidie, one of the founders, continues as the lead brand director for Alien Labs.

Aaron: In what geographies do you currently operate?

Sam: Our primary offices and facilities are based out of Sacramento, California, but we have facilities throughout the state. Last year, for the first time we launched operations in a new state, Arizona. As you may know, you’re not allowed to take cannabis products across state lines at all, so if you want consistent product in multiple markets you really have no choice but to rebuild your entire infrastructure in each state you want to open up.

There are many brands that are expanding and launching in more markets more quickly, but they’re doing so by taking product that’s already existing and putting their brand name on it. That is something we’ve decided strategically that we will not do. We’ve spent years building a high level of trust with our customers, so we’re only going to put our brand name on products that are our genetics, our cultivation, our style, our quality of product. When we launched in Arizona, we did it with a facility that we leased and took over and now operate with our staff. We’re replicating the same exact product that you can get in California in Arizona, which is really exciting.

We launched just this past November, which has been incredibly successful. Our dispensary partner Harvest saw lines of dozens of people out the door.“We consider ourselves a flower company first and foremost, so for us, that was a very calculated strategic move.”

Aaron: Any new geographies on the horizon that you can talk about?

Sam: We’re constantly evaluating new opportunities. I don’t have anything particularly specific to announce right now, but I will say we look for states where we believe there’s a competitive environment where the product quality is going to really stand out and be appreciated.

Aaron: Do you notice any differences in consumer trends between California and Arizona that stand out?

Sam: Not too many yet. We don’t have a retail location in Arizona, so we don’t have as much direct contact. However, we have heard consistently that the Connected customer demographics – as you would imagine most interested in our product – are those looking for something special, unique, different and have a really superior quality to everything else out there. We ended up launching in Arizona with the highest price point for flower in the state, and we say that’s just the beginning. The market is still so young and immature, both nationally and internationally, that this category is going to develop into one that’s really taste-driven.

Aaron: What’s next in California?

Sam: Continued growth and product development. We want to keep blowing away our customers with more and more incredible products, different product types and categories. For example, the cartridges were a really big launch for us because we don’t really consider ourselves a vape company. We consider ourselves a flower company first and foremost, so for us, that was a very calculated strategic move. We were only going to launch the product if we could fully replicate what the consumer gets from the flower experience. We are very unlikely to ever release a distillate pen, for example.

Aaron: What are you personally interested in learning more about?

Sam: We, as a society, really don’t know very much about the cannabis plant. Pretty much all meaningful research around cannabis stopped in the early 1900’s with prohibition. In the meantime, we’ve performed millions of dollars of studies and research on almost every other plant that we grow commercially. We understand these plants extraordinarily well. Cannabis science is stuck back in agriculture of early 1900s. The most interesting conversations I have are around how the plant works, how it doesn’t work and the ways in which it is so different from all other plants with which we are familiar. Our head of cultivation comes from Driscolls, the largest berry company in the world, and even he is frequently surprised by the way the cannabis plant reacts to things that are commonly understood in other plants. So, the way the actual plant responds to different environments is truly fascinating and something I think we’ll be learning about for decades and decades to come.

Aaron: Okay, great. That concludes the interview. Thank you, Sam!

This website uses cookies so that we can provide you with the best user experience possible. Cookie information is stored in your browser and performs functions such as recognising you when you return to our website and helping our team to understand which sections of the website you find most interesting and useful.

Strictly Necessary Cookies

Strictly Necessary Cookie should be enabled at all times so that we can save your preferences for cookie settings.

We use tracking pixels that set your arrival time at our website, this is used as part of our anti-spam and security measures. Disabling this tracking pixel would disable some of our security measures, and is therefore considered necessary for the safe operation of the website. This tracking pixel is cleared from your system when you delete files in your history.

We also use cookies to store your preferences regarding the setting of 3rd Party Cookies.

If you disable this cookie, we will not be able to save your preferences. This means that every time you visit this website you will need to enable or disable cookies again.

For those Qualified Equity Licensees who have already received a fee waiver, it’s important to remember that this is a yearly process, and that they must continue to submit a request for equity fee relief at least 60 calendar days before the annual expiration date of their license.

For those Qualified Equity Licensees who have already received a fee waiver, it’s important to remember that this is a yearly process, and that they must continue to submit a request for equity fee relief at least 60 calendar days before the annual expiration date of their license.