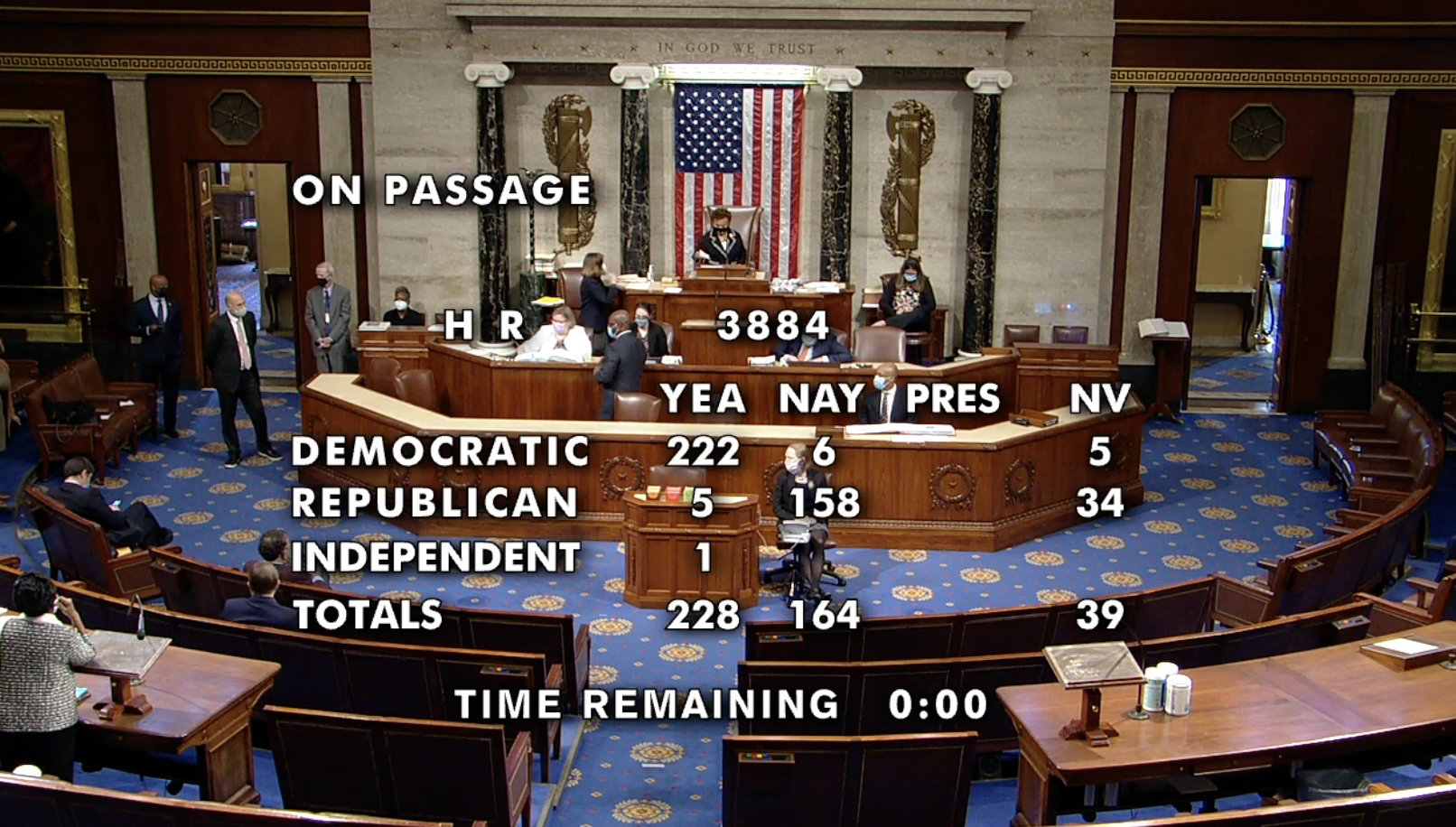

Here we are again, crossing our fingers, hoping that the Senate will approve the passage of the Secure and Fair Enforcement Banking Act (SAFE Banking Act). This Act would provide banks with regulatory protections, allowing them to offer critical financial services to cannabis businesses without risking the loss of their banking charter.

As the 2024 elections loom, the stakes have never been higher for passing the SAFE Banking Act.

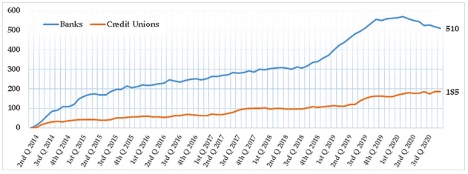

Cannabis Legalization is On the Rise

As of August 2023, 40 states, four territories and the District of Columbia have legalized medical or adult use cannabis. While some states have moved more slowly, the entire West Coast (including Nevada and Colorado) has voted to pass laws allowing the sale and purchase of adult use cannabis. Most of the East Coast has followed suit; New York, Pennsylvania, New Jersey and Massachusetts have all voted to regulate cannabis. It has become evident that the majority of U.S. citizens are now comfortable with legalized cannabis (156 million people live in jurisdicitons that have legalized adult use).

Banking Roadblocks for the Cannabis Industry

Under current federal policy, banks and other large financial institutions face regulatory restrictions that make it challenging to provide the most basic services to local cannabis companies, regional cannabusinesses and MSOs (Multi-State Operators).

Federal anti-money laundering laws and related record-keeping regulations, such as the Bank Secrecy Act (BSA), have presented complex compliance protocols that prevent banks from meeting the business needs of local growers, manufacturers and dispensaries. Local cannabis business owners are therefore put in a difficult position, as they must balance daily business activity against the potential dangers of operating as a cash-only business.

How Would the SAFE Banking Act Help Banks Serve the Cannabis Industry?

The proposed SAFE Banking Act would protect banks from federal penalties for offering their services to cannabis businesses in states with regulated cannabis industries. Critically, the bill would shield banks from losing their deposit insurance. Without reform through the SAFE Banking Act, financial institutions will remain essentially prohibited from working directly with legal cannabis companies.

Policymakers may need to introduce the Act as a stand-alone bill that outlines clear objectives and specifically addresses the issue from a public safety perspective. Cannabis is a hot-button issue, so adding additional legislation will muddy the water and make it easier for Senate members on the fence to vote against the bill.

Cannabis industry representatives and political allies must be strategic in navigating the bill’s potential passage and take the process step by step. First, the SAFE Banking Act must pass to allow cannabis businesses the opportunity to stabilize, grow and prosper. As the sector grows stronger and more accepted by mainstream America, more progressive bills can be introduced and will have a greater chance of successful passage in the House and Senate.

The SAFE Banking Act is an Issue of Public Safety

Every day the Senate chooses to sit on their hands, they put more Americans in harm’s way. This is unacceptable.

Because dispensaries and other cannabis businesses must process daily transactions without basic banking services, they often accumulate large amounts of cash. Dispensaries are, therefore, frequent targets for criminals. Even as the cannabis industry matures and contributes significant tax dollars to State coffers, banks and financial institutions have no choice but to sit with their hands tied, watching with horror as organized criminals literally take aim at dispensary staff.

The passage of the SAFE Banking Act is literally life and death for many cannabis industry employees. How many workers and customers must suffer harm before the Senate wakes up and passes this critical bill? Regardless of their stance on cannabis, members of the Senate must do their jobs, heed the will of the American people and pass the SAFE Banking Act to rectify this increasingly dangerous situation for the good of their constituents.

Spring is a time of renewal, growth and planting. While many gardeners focus on traditional crops, there is a growing community of cannabis enthusiasts who are also embracing the opportunity to cultivate their own cannabis plants.

Research from New Frontier Data reveals that approximately 3 million people worldwide grow their own cannabis at home, resulting in a staggering yield of approximately 11 million pounds of smokeable flower each year. This number is projected to reach 15 million pounds annually by 2030. Amidst all the excitement around planting and growing, it is essential not to overlook the indispensable foundation of all cannabis plants: the seeds.

The Power of Cannabis Seeds

Affordable and versatile, cannabis seeds provide growers with the ability to cultivate specific strains tailored to their health and wellness needs. These seeds are typically the size of a peppercorn, characterized by an ovular shape tapering to a pointed end. While seeds can vary in color and striation, they typically exhibit a brown hue. Unfertilized seeds, on the other hand, appear off-white and are considerably smaller in size.

Economic Impact

These tiny powerhouses enable growers to cultivate customized strains, while also contributing to the economic growth of the global seed market.

The global cannabis seeds industry was valued at $1.3 billion in 2021, according to Allied Market Research. Experts predict that this figure will surge to $6.5 billion by 2031. Notably, North America accounted for more than 80 percent of the global seed market in 2021.

Benefits for Home Growers

According to New Frontier Data, 70 percent of home growers purchase seeds and cultivate cannabis for the sheer enjoyment of the process while 52 percent find it to be a convenient option. In addition to these advantages, numerous research studies highlight the multiple health benefits of growing one’s own crops, including reduced stress levels, decreased anxiety and increased exposure to the outdoors. Some innovative chefs have even begun incorporating cannabis seeds into their culinary creations, further expanding the versatility and appeal of these seeds.

Seed Safety Considerations

Given that cannabis seeds form the foundation of the entire cannabis industry, it is crucial to understand the various options for obtaining them. One increasingly popular method is through online seed banks, such as Rocket Seeds. However, it is important for those new to purchasing seeds online to thoroughly research the legalities surrounding these transactions. Cannabis seeds are subject to legislation similar to other cannabis products such as flower, concentrates and edibles. The legality of purchasing seeds varies depending on the state in which one resides. It is vital to check local legislation before making any decisions. In states where adult use cannabis is legal, buyers only need to be 21 years or older to order seeds online. Conversely, in states where adult or medicinal use is not permitted, purchasing seeds online remains completely illegal.

Purchasing Seeds Online

Selecting a reputable online seed bank is critical. Ensure that the chosen seed bank has positive customer reviews, offers quality customer service and provides germination guarantees. Researching the available strains, payment options and shipping policies is also essential. It is advisable for beginners to start small by purchasing only a few seeds at a time. Prior to planting, conducting thorough research is necessary, as there are numerous variables to consider and a steep learning curve to navigate. Fortunately, abundant resources are available to assist in this journey. For example, we offer valuable advice on getting started. Additionally, individual seed manufacturers, as well as online resources and apps like Seedtracker, provide guidance and support.

Continued Growth

The U.S. legal cannabis market is projected to exceed $31.8 billion in annual sales by the end of 2023, according to leading cannabis research firm Brightfield Group. Furthermore, they anticipate that within five years, the market will surpass $50 billion in annual sales. Amidst this flourishing industry, it is important to recognize that seeds form the backbone of this expansive market.

As the cannabis industry continues to thrive and expand, it is crucial to acknowledge the fundamental role played by seeds. These tiny powerhouses enable growers to cultivate customized strains, while also contributing to the economic growth of the global seed market. By recognizing the benefits of growing one’s own cannabis and taking proper precautions when purchasing seeds, individuals can partake in this exciting and rapidly growing industry while savoring the rewards of their own harvests.

As the cannabis industry experiences a significant shift toward general acceptance and mainstream adoption, new modes of operation are popping up everywhere. The evolution and expansion of the industry beg for constant innovation, and the integration of NFTs and cryptocurrencies as payment options is at the crossroads between tech and cannabis.

Crypto and NFTs have grown in popularity in recent years. Non-fungible tokens are an interesting asset in the art and collectibles world, while cryptocurrency has made a name for itself by providing a unique kind of financial independence. More and more payment processors are embracing these new payment methods, and the cannabis industry is also slowly welcoming them.

In order to fully understand the cannabis-crypto connection, Swaroop Suri, founder of Melee Dose, a cannabis brand that’s been embracing NFTs and crypto as payment options, shared some insights. Their innovative approach to creating unique cannabis experiences with technology and creative branding makes them a pioneer of this movement.

What’s Happening with Cannabis and NFTs?

NFTs and cryptocurrency are exciting developments in an industry that carries the reputation for having a rocky relationship with the banking industry. The legal gray area surrounding the connection between cannabis businesses and the banking industry has given way to an onslaught of challenges, with many banks shunning cannabis because of its federally illegal status. While traditional banking can limit cannabis companies’ access to basic financial services, the decentralization that’s characteristic of blockchain opens up many doors.

In recent years, different brands have tested the waters by using cryptocurrencies and NFTs to enhance marketing and offer alternate payment options. While it’s still early in the game, trends are starting to appear.

Bitcoin quickly became one of the more popular cryptocurrencies

One of these trends is using NFTs in marketing and branding, creating unique digital assets that can be collected. This gives an air of exclusivity, creates more immersive experiences, and helps forge a brand identity. NFTs are often a great tool to engage with customers and create a sense of community.

Melee Dose recently started integrating NFTs from Bored Ape Yacht Club (BAYC) into product packaging and branding. This has allowed the brand to offer unique experiences, foster community engagement, enhance storytelling and demonstrate adaptability to an ever-changing world.

“This collaboration merges the worlds of fashion, art and technology, providing our customers with exclusive “IRL” products incorporating digital assets and driving brand affinity”, says Swaroop Suri. “By embracing the digital revolution and connecting with the influential BAYC community, we aim to redefine consumer experiences and build lasting relationships with our audience.”

Crypto Payments Aren’t Futuristic Anymore

Payment is another trend to look out for. Cryptocurrencies are becoming more accepted in many big industries, including cannabis. With traditional banks limiting access to banking services, crypto allows cannabis companies to offer decentralized and secure payment options.

Cryptocurrency offers more enhanced privacy than traditional payment methods, which is great for those who want to stay under the radar. Lower transaction fees are another plus, as a decentralized system is more flexible. The speed of crypto payments is also an enticing feature, as payments are usually processed more quickly than traditional payment methods.

Swaroop Suri, Founder of Melee Dose

So, how are brands accepting crypto as payment? Is it safe? Melee Dose started accepting cryptocurrency payments on their e-commerce store by partnering with Coinbase Payments, a leader in the crypto industry with a strong reputation and ease of integration.

Cryptocurrency may seem perilous to those who don’t know much about it, but siding with the right company can help ease those fears. Addressing concerns about crypto volatility, Suri “opted for a feature provided by Coinbase Payments that allows for immediate conversion of cryptocurrency payments into our local currency, ensuring stable revenue despite market fluctuations.”

By working closely with reliable payment partners like Coinbase Payments and implementing necessary features, companies like his are able to successfully overcome crypto roadblocks, providing customers with increased flexibility and convenience.

The Future of Crypto, NFTs & Cannabis

The future of integration between cannabis, crypto and NFTs is exciting and always on the move, meaning there are opportunities constantly arising and challenges ahead we have yet to tackle. As cannabis legalization continues to evolve, we might expect changes in regulatory frameworks that impact how cryptocurrency is used in the industry. While we can’t say what those changes might be, the fact that NFTs and crypto have become mainstream indicates a clear adoption, as the industry finds ways to integrate them. From blockchain integration and creative marketing to payment options and immersive experiences, they are here to stay.

Swaroop Suri and his team might’ve gotten in on the game early, but they know the future is expansive: “It’s possible that NFTs could become a significant part of cannabis marketing strategies in the future,” He says. “The cannabis industry can use NFTs in various ways, such as tracking crops and using intellectual property to promote products through packaging artwork, which is what our team at Melee Dose has accomplished.”

NFTs won’t stop there. “There is a possibility to use NFTs for establishing VIP programs that offer exclusive discounts and access”, Suri says. “The ownership of an NFT could grant special privileges and perks to customers when shopping with an e-commerce company, fostering a deeper connection with the brand and community and leading to customer loyalty in the long run.” NFTs offer diverse possibilities for cannabis brands to improve their marketing techniques and get creative.

When it comes to crypto payments, brands will surely continue to add crypto as an option in addition to merchant processors. Highly-regulated industries like cannabis can find many benefits in crypto, as experienced by Suri: “Accepting cryptocurrency can mitigate some of these issues by providing an alternative payment option that is not subject to the same restrictions as traditional payment methods.”

Final Thoughts

The excitement surrounding crypto and NFTs is understandable, and as the cannabis industry introduces new opportunities for those who are at the intersection of these two global forces, companies everywhere are changing their relationship with technology.

There are other brands hopping onto the this train as well. Household cannabis brands and popular companies like Plain Jain, Highland Pharms, American Green and Pharma Hemp are just some of the many that have begun accepting crypto as payment.

As the industry continues to evolve and grow, staying ahead of the curve and embracing technology with critical thinking and environmental consciousness is key. As a new, dynamic and exciting space with as many opportunities as it is filled with challenges to tackle down the road surrounds us, the one thing we know for sure is that this is just the beginning.

Have you ever been to the DMV, only to be turned away because you didn’t have the countless forms of identification needed? Sometimes it feels like no amount of ID or proof of residence is enough, whether it’s your 2nd grade report card or an electric bill from 25 years ago.

That feeling is what it’s like for anyone working in compliance; regardless of industry. Banks are no different. They need to possess compliance documents such as Consolidated Reports of Condition and Income and other Federal Financial Institutions Examination Council (FFIEC) reports that work like the laundry list of documents you need to get a driver’s license or get your car registered.

The same can be said for newly licensed and legal cannabis companies. They often need state and local inspection documents, federal background checks and a list of other documents that make a CVS receipt look minuscule in comparison.

Historically, across all industries, the whole process of gathering and providing these sorts of documents can turn into a bit of a charade. Many companies do the bare minimum to check the compliance box and achieve certifications. Various teams and stakeholders try to skate through the compliance process by providing answers that reflect what they think the enterprise customer wants to see (vs. the reality).

In order to achieve long term growth, financial institutions (FIs) and cannabis companies alike need to start executing compliance plans. FIs are always seeking new growth and revenue opportunities, and cannabis companies are constantly under the scrutiny of regulators. Identifying new solutions that can help companies grow quickly while also maintaining compliance should be an essential part of the roadmap.

Financial Institutions and Cannabis

Many think that financial institutions and cannabis businesses would be on opposite ends of any spectrum. Banking is a mature and established industry, while legal cannabis is a new, fast moving and constantly evolving space. So, on one side, there is a risk averse fiscally conservative and traditional business model, and on the other side is an industry that is outside of the mainstream.

Let’s look at this perception from a different angle though. What is true is that both industries are highly regulated and must comply with the rules placed upon them by regulators; and if their house isn’t in order, the consequences can be disastrous (Read: Massive fines or even losing the ability to operate). CRBs and FIs deal with the security and dual control of inventory, and making sure customers are properly identified and of legal capacity to conduct business. In most cases, both are small businesses within their respective communities.

Moreover, each of the industries are forced to navigate nearly-constant regulatory change, making the act of complying with applicable regulations a moving target. For most of these types of businesses, regulatory compliance is cited as one of the largest (and most expensive) challenges they face in day-to-day operations.

Compliance as Revenue Protection

When financial institutions make the decision to offer services to the cannabis industry, they naturally look at the market opportunity to determine whether the effort associated with the increased compliance obligations outweigh the potential benefits. Traditionally, compliance is viewed as a cost center, but in reality, it’s a revenue protection center. As the old saying goes; “an ounce of prevention is worth more than a pound of cure.” Compliance is that prevention.

Cannabis companies need to demonstrate reliability and a history of compliance in order to attract investors and accumulate capital

Failing to fully comply and meet regulatory compliance standards can cost organizations billions. Having a trusted system of compliance established should not be looked at as a cost-sucking measure for businesses, when it really is negligible when the cost of getting it wrong is far more substantial. Setting up a truthful and transparent compliance program isn’t just the right thing to do, it also protects revenue.

As the cannabis industry continues to grow, navigating around pain points is becoming increasingly expensive for the companies participating in it, many of whom are still struggling to turn a profit. Specifically, an IDC forecast shows global revenue from GRC solutions growing from $11.3 billion in 2020 to nearly $16.2 billion by 2025. And the average business hires and spends upward of $50,000 to $200,000 on consultants to manage compliance. It’s not uncommon for companies to dedicate five to 10 people working on compliance every week for hours and months on end.

Many in the banking industry are worried about forging into a stigmatized stream of revenue like cannabis, but with the right compliance solutions in place, they can have peace of mind. These solutions guarantee that revenue from cannabis is done legally by analyzing where each dollar came from, and denying those that don’t meet the minimum criteria. Having visibility into cannabis-related business (CRBs) accounts that do the enhanced due diligence is the only way to operate.

By implementing purpose-built compliance management solutions, financial institutions are able to unlock new revenue streams and scale cannabis banking operations. Meaning that as cannabis continues to gain mainstream momentum, and becomes less scrutinized locally and federally, these FIs that take part will be ahead of the curve.

Looking Ahead

With recent movement towards legalization in the House, cannabis investors are optimistic about the industry’s future. So how can the cannabis market overcome these hurdles and remain highly profitable?

To start with, CRBs must have greater access to accredited financial institutions like banks and credit unions. Owning bank accounts, obtaining credit cards, and applying for small business loans is essential to growth. Providing CRBs with access to proper financial support and compliance control is crucial for the cannabis market to continue to thrive.

Federal legislation such as the SAFE Banking Act is currently thought of to be the silver bullet that will open the floodgates for CRBs and FIs to work together. But in reality, this is a myth, as the SAFE Banking Act will simply make the current compliance rules stricter.

To be a first mover FI in your area, businesses must start by implementing a scalable, verifiable cannabis banking program. The real customers and financial opportunities are out there, and are even greater than what you might have modeled given the growth of the industry. The ability to do this today is real.

As the former CEO of Partner Colorado Credit Union (PCCU), Sundie Seefried has been in the credit union space for 39 years. Established in 2015, Safe Harbor Financial is now a leading provider for banking and financial services in the cannabis industry.

Seefried founded Safe Harbor as a cannabis banking program for PCCU, and since then it has withstood scrutiny of 16 separate federal and state exams. Entering its ninth year as a cannabis banking program, they have almost 600 accounts in 20 states and have processed over $14 billion in transactions for the cannabis market. In September, Safe Harbor began trading on Nasdaq under the symbol SHFS. The company has also announced a definitive agreement to acquire Abaca, an industry-leading cannabis financial technology platform.

Seefried has seen it all in the cannabis banking world. We wanted to get her thoughts on some current events, the future of cannabis banking and lending, and what the next few years might hold in store for an industry ready to grow.

Cannabis Industry Journal:Tell us a bit about yourself. What is your background and how did you find yourself in the cannabis industry? How did you get to become president and CEO of SHF?

Sundie Seefried, President & CEO of Safe Harbor Financial

Sundie Seefried: I’ve been in banking in the credit union space since 1983. I became CEO of Partner Colorado Credit Union in 2001 and stayed there for 21 years. Everything I do, I have a very conservative nature just from being in the banking world and doing things methodically and building good foundations that endure long term. In 2014 when FinCen issued guidance, I was supposed to retire, and I had dinner with some old friends that were attorneys who couldn’t get bank accounts for their clients in the cannabis industry. They asked me to help and I looked into it for them. I assumed the regulator would shut me down but he didn’t; he actually encouraged me to move forward and look further into things. As I educated the board, we saw just how unsafe Colorado was and the serious need for the community to figure things out with respect to banking and cannabis. Coming from that credit union perspective, I said I think we can do this, let’s try and I’ll go through the third parties necessary. And that’s how we got into this, just looking to try and help solve Colorado’s problems and get banking access for cannabis companies.

CIJ: Tell me about your company’s mission. What is your financing strategy in cannabis and of the companies you do business with, what do you look for most?

Seefried: Our mission remains the same, and that is to normalize banking in the cannabis industry as much as possible. Because the black market still exists, the issue becomes sorting the legal entities out from the illicit actors in the industry. We know that the illicit market is trying to hide amongst the legal environment, which really makes things difficult for upstanding cannabis businesses. We can normalize banking by making sure we help legitimize the compliant entities and sort out the bad actors. We really only want to work with legitimate players with licenses, who are fulfilling expectations on the regulatory level and have no problems with compliance. We have been able to do that on the depository side.

We have always been a low-cost provider and our clients count on that. As we move into the lending part of the industry, we’re looking to do the same thing. There are lenders who charge one-to-three percent per month, 18 to 36 percent per year. We, on the other hand, are targeting more of an eight to thirteen percent annual rate. More of a conservative approach. Real debt underwriting. No extremely high interest rates. We look for the collateral, we look for well-organized businesses and solid documentation. Those are the businesses we are trying to bring into the fold and offer them normal loans. Cannabis will always have a premium on it simply because it is illegal at the federal level and there are additional hoops we have to jump through. Because of the potential forfeiture and seizure, if there are bad actors, etc., it really behooves any clients coming to us to also place their depositary services with us so we can prove their legitimacy and provide loans to them.

CIJ: Let’s talk about the Canopy Growth news. They announced they are pulling the trigger on acquiring Wana Brands, Acreage Holdings and Jetty Extracts, under the Canopy USA holding company and ahead of federal legalization. On the surface, it looks like they are bypassing a lot of the hurdles American cannabis companies currently face with financial red tape. As a foreign company trading on the NASDAQ dealing with a schedule 1 substance, do you expect Canopy to have a significant, some would say unfair, competitive advantage with their early entry? Or is this perhaps more of a rising tide lifting all boats scenario? What effect will this have on the current market landscape?

Seefried: I find it a very interesting move on their part. Certainly, they have a big advantage in comparison to other companies. The consolidation in the industry is moving so quickly. Other players will keep up with this just as fast as Canopy is moving in. That’s my opinion in terms of what I see in the consolidation area of the market. I think what it really hurts is small businesses. My heart goes out to them. So many of them worked so many years to build excellent small companies with boutique shops, and this whole move will really change that part of the industry.

I see a lot of these small players, non-vertically integrated companies, being impacted in a negative way due to such mass consolidation and the entry of foreign businesses. We need to get more competitive on a global level in order for our companies to grow and thrive. This happened back in 2018, when so many companies started doing those reverse takeovers onto the Canadian Securities Exchange and suddenly, they were putting tens of millions of dollars into the U.S. market. People didn’t see that as a competitive disadvantage for American companies, but now this move by Canopy may really show that we have to look at things more globally.

CIJ: Biden’s announcement regarding the scheduling review for cannabis has a lot of industry folks very hopeful that federal legalization is closer to a reality than before. Do you share their optimism?

Seefried: Closer than before, yes. But how close? I am not convinced it will happen quickly. If they are really going to consider rescheduling or descheduling, everything happens in Washington very incrementally. Eight years and seven attempts at the SAFE Banking legislation and still no movement on that front. Tomorrow, we’re going straight to legalization? I have a hard time swallowing that one. I just don’t see that big of a jump all at once. I think it is interesting coming just before the midterms and votes are really needed now more than ever.

What Biden did was a great start. Especially for those people in prison for possession. The interesting part of it is, we are very serious about people who have used it, but the people who have sold it and are in prison might be in the same situation. Given how the laws worked for so long, just based on the amount of cannabis you had could get you automatically labeled as a dealer, which isn’t the case for a lot of incarcerated folks.

The fact is, the social equity and justice issue, who do you free or who do you not free from prison, is a very difficult issue to get through. I think it is a great step forward and it will help some people who were treated unjustly, but there is still a lot of work to be done.

“I believe we’ll start seeing pressure from the global market on the United States to move things along a little faster in our own country.”As far as rescheduling, if they go from a Schedule I drug to a Schedule II drug, that will do no good, but it certainly is a bone to throw to the industry if you want to look like you are making some progress. Schedule II is still subject to 280E tax code so it will only do so much. If they want to make things more equitable and actually level the playing field, they have to do something about the 280E issue hindering every cannabis business in the country.

As far as full legalization, I am not optimistic because of all the players that need to be involved. Full legalization will require a change to the IRS tax code 280E as well as other tax issues. I think there are too many players: The DOJ, FinCen, the DEA, the FDA, the IRS. All of these agencies will have to agree on full legalization and moving forward in unison. The DEA is trying to fight illicit actors and illicit drugs. FinCen is trying to follow the money to find illicit actors. As long as there is an illicit market it will make their job tough, and on top of all of that, we have politics in play. That is just my take on legalization. It is going to be a much more complex problem than just legalizing the plant and moving on. Rescheduling seems like lower hanging fruit, but they will have to move it higher than a Schedule II.

CIJ: With the midterm elections here, there are a number of legalization measures in a handful of states, along with political control of Congress on the ballot. How do you think a Republican or Democrat controlled Congress will affect cannabis legalization progress?

Seefried: I just finished doing some lobbying in September in DC and spoke to some Senator offices in person, and I heard a lot of interesting topics being discussed. One of the things that keeps popping up is that social equity and justice is a huge issue. If we can’t solve this injustice in our system that has been going on for decades and decades, maybe they’ll hold banking legislation hostage. You can’t correct 50-60 years with one piece of legislation. Everything has to be incremental, unfortunately, so there will be some give and take there. I think that was a primary focus, especially with the Democrats and I do think it is a worthy cause.

On the Republican side, economically improving our competitive advantage as a country. They are starting to see the jobs being created and the tax revenue coming in and the growth of the industry. They will have to make that decision at some point in time whether they are going to leave the American cannabis industry behind or allow them to compete on a global level. I really think everything will move slowly and continue as it has happened in the past.

I believe we’ll start seeing pressure from the global market on the United States to move things along a little faster in our own country.

CIJ: As we inch closer to 2023, what do you expect the next year to offer for the cannabis financing market?

Seefried: I would say, with or without legislation, they’re finding greater access to banking. And the reason they are getting better access to banking is because none of us have been prosecuted for simply engaging in cannabis banking. I think we have set a precedent over the past eight years, not only us but other service providers in the industry and that we are not being prosecuted.

I see more financial institutions entering the market slowly. The second reason access to capital and banking will increase is because every financial institution in the country wants that lending relationship. In order to get there, they want to start with the depository relationship, and they don’t want smaller players presently doing it and getting all of those relationships before they enter the market. I think the competitive nature of the financial industry to land that lending relationship is going to force them into the game sooner than later.

Despite the US making cannabis regulations challenging to navigate, the industry is snowballing toward profitability. New Jersey legalized adult use cannabis on April 21 this year. One month earlier, The Garden State began accepting applications for Class 5: Retailers, Dispensing and Delivery.

Although New Jersey isn’t shy about its licensing requirements and standards, many people want to know how retailers can stay in the game for the long run. So, let’s talk about risk management considerations New Jersey retailers need to know.

Top Risks Cannabis Retailers Face in New Jersey

Regardless of what kind of retailer you operate —medical or adult use — it’s critical to know what you’re up against. The following are the most common risks we’ve watched cannabis retailers face daily in New Jersey, making a customized risk management strategy necessary.

Theft

Like other retailers, New Jersey cannabis retailers are vulnerable to theft. Unfortunately, theft can come from various angles, such as in-store, in-transit and insider crime. Besides cannabis retailers typically having a well-stocked inventory, it’s not uncommon for them to have more cash on hand than most other businesses.

Although the SAFE Banking Act could positively impact the cannabis industry, it’s in a notorious stall yet again. Briefly, the SAFE Banking Act would no longer allow financial institutions, such as banks and credit card companies, to refuse to do business with cannabis companies. However, cannabis retailers must operate in a cash-only environment, for now, forcing them to make bank runs multiple times a day. We probably don’t have to explain how enticing a significant inventory and fat bank bags look to criminals.

Cybersecurity

Since the onset of the global health crisis, the cyber liability landscape has nearly spun into a death spiral. In other words, cybercriminals sat on the edge of their seats during the pandemic, waiting to pounce on anything that looked slightly vulnerable. Remote workers, small businesses, and emerging industries were hard-hit.

It’s no surprise that New Jersey cannabis retailers face many cybersecurity risks through their point of sale (POS) systems. Additionally, retailers often gather and store personal information, such as email addresses, credit card numbers, shipping addresses, etc. Hackers and cybercriminals gravitate to this vital data rapidly.

Property Damage

In addition to the risk of theft, as mentioned above, cannabis retailers must protect their property from losses. Without adequate protection, damage to equipment or buildings could add up to high out-of-pocket costs. Consider the damage a weekend office fire or late-night vandalism would cause. If property damage occurs, retailers must figure out how to sustain business operations while recovering from the loss simultaneously. As a result, New Jersey retailers must protect their property and maintain business continuity.

How to Customize a Risk Management Strategy

Watch or listen to any news reports and there’s a decent chance that you’ll feel some slight sense of doom and gloom. And sure, a lot is going wrong in our world; however, that doesn’t need to impact how you perceive your businesses. Instead of casting a massive net over every possible risk that you can imagine, we recommend trying the following 5-step approach. Here’s the gist:

Identify: Pinpoint high-level risks that are specific to the cannabis industry. Then, let the process trickle down to focus on company-specific exposures.

Analyze: Determine how badly a particular risk could harm your retail company. How much will this hurt should the “what-ifs” play out?

Evaluate: Categorize risks according to how risk tolerant your company is. Will you avoid, transfer, mitigate or accept the risk?

Track: Use your history or the stats from a similar retailer to map out how you’ve handled the risk over time. Older retailers have an advantage over younger retailers, of course, but you can still get a feel for your risk management style.

Treat: Make good on your evaluation promises by avoiding, transferring, mitigating, or accepting the various risks you identified.

Recommended Insurance for New Jersey Retailers

Sales totals in the first month of New Jersey’s adult use market

The New Jersey Cannabis Regulatory Commission issued detailed requirements for new cannabis businesses. That said, part of the application requirements considered is the plan for companies to obtain liability insurance. Many new retailers opted for a “letter of commitment” as opposed to a certificate of insurance (COI), stating their plans for obtaining the following coverages:

Commercial general liability: Protects cannabis companies against basic business risks.

Product liability: Protects against claims alleging your product or service caused injury or damage.

Property: Reimburses cannabis companies for direct property losses.

Workers’ compensation: Covers employees if they are injured on the job and can no longer work.

In addition to the required insurance coverages, we recommend New Jersey retailers customize their risk management package with these policies:

Crime: Protects your cannabis company against specific money theft crimes.

Cyber: Protects your cannabis company against damages from specific electronic activities.

Directors & officers: Protects corporate directors’ and officers’ personal assets if they are sued.

Employment practices liability: Protects cannabis companies against employment-related lawsuits.

Professional liability: Protects cannabis companies against lawsuits of inferior work or service.

With more states in the US entering the marketplace soon, New Jersey is doing its fair share of the heavy lifting by spearheading the onboarding process. Remember, doing your due diligence at the start pays off in the long run — New Jersey retailers are proving that. Consider teaming with a commercial insurance broker calibrated to the cannabis industry, so you get the most out of your broker, marketplace and the cannabis industry as a whole.

Like this article and want to see more? Subscribe to our free newsletter here The cannabis industry could receive a significant boost if the recently introduced Capital Lending and Investment for Marijuana Businesses (CLIMB) Act passes Congress. The bipartisan bill was introduced by Rep. Troy A. Carter, Sr., a Democrat from Louisiana, and Rep. Guy Reschenthaler, a Republican from Pennsylvania. It is intended to boost the cannabis industry by creating greater access to capital, banking insurance and other business services. Unlike the SAFE Banking Act (which specifically addresses banking services for the cannabis industry), the CLIMB Act was introduced “to permit access to community development, small business, minority development and any other public or private financial capital sources for investment in and financing or cannabis-related legitimate businesses.”

Rep. Troy A. Carter, Sr.

Currently, the cannabis industry faces a serious dilemma with regard to accessing not only traditional banking services, but also essential capital and financing sources. The latest member of the cannabis bill alphabet soup attempts to remedy this by addressing two key issues.

First, the CLIMB Act would permit access to key “business assistance” programs from various financial institutions by prohibiting any federal agency from bringing any civil, criminal, regulatory or administrative actions against a business or a person simply because they provide “business assistance” to a cannabis state-legal company. The CLIMB Act defines “business assistance” broadly to include, among other things, management consulting work, accounting, real estate services, insurance or surety products, advertising, IT and other communication services, debt or equity capital services, banking or credit card services and other financial services.

This provision of the CLIMB Act would immediately create more access to traditional insurance, lending and credit. This broad protection would not only apply to private entities providing “business assistance,” but arguably means that the U.S. Small Business Administration (SBA) could not be penalized by Congress or another government agency for providing loans to state-legal cannabis companies. Moreover, currently the cannabis industry does not have access to use credit cards, as major credit card companies refuse to permit such transactions. The CLIMB Act could pave the way for major credit card providers to begin permitting cannabis transactions. Permitting the use of major credit cards like American Express, Mastercard and Visa could result in an increase in sales for cannabis retailers.

The second, and possibly the most important, aspect of the CLIMB Act is that it would amend the Securities and Exchange Act of 1934 to create a “safe harbor” for national securities exchanges like Nasdaq and the New York Stock Exchange (NYSE) to list cannabis companies and would permit the trading of these cannabis businesses stock. Currently, plant-touching cannabis companies with operations in the U.S. can only be listed on a Canadian-based exchange and can also only be traded in the U.S. via the over-the-counter (OTC) markets. Trading securities on the OTC markets does not provide the same level of security as securities traded on a national exchange like Nasdaq or NYSE. Specifically, the CLIMB Act delineates that the federal illegality of cannabis is not a bar to listing or trading of securities for legitimate cannabis-related businesses.

Rep. Guy Reschenthaler

This provision of the CLIMB Act has two immediate effects. First, the CLIMB Act would allow for U.S. cannabis companies currently listed in Canada to list on the Nasdaq or NYSE. Second, this provision would allow more traditional, “blue-chip” industry companies currently listed on Nasdaq or the NYSE who haven’t been able to operate within the cannabis industry as a plant-touching entity, to enter the cannabis industry as an active participant.

In announcing the CLIMB Act, Representative Reschenthaler stated that “American cannabis companies are currently restricted from receiving traditional lending and financing, making it difficult to compete with larger, global competitors. The CLIMB Act will eliminate these barriers to entry, and provide state-legal American cannabis companies, including small, minority, and veteran-owned businesses, with access to the financial tools necessary for success.”

It is important to note that the CLIMB Act, like the SAFE Banking Act, only represents one small, but important step toward cannabis reforms. Neither proposal would legalize, de-schedule or reschedule cannabis. Rather, the CLIMB Act addresses very real-world, operational issues facing the cannabis industry. With that in mind, the CLIMB Act would certainly provide much needed clarity for issues facing all cannabis companies.

Passage of the CLIMB Act is not a forgone conclusion, but rather is quite uncertain. Other pieces of cannabis-related legislation, like the SAFE Banking Act, have passed the House of Representatives multiple times without the U.S. Senate taking any action. Moreover, the CLIMB Act was introduced with only two legislative supporters.

By Tamara L. Kolb, Amy Bean, Caitlin Strelioff No Comments

As the legal cannabis market expands, banks and nonbank financial institutions (NBFIs) across the United States continue to explore how to safely provide banking and other financial services to cannabis-related businesses (CRBs) and other CRB ecosystem players. At the same time, these organizations are taking into account changes they might need to consider relative to their Bank Secrecy Act ( BSA), anti-money laundering (AML) and related compliance programs.

Regulatory conundrum

The Controlled Substances Act (CSA) identifies the cannabis plant and all its derivatives as a Schedule 1 controlled substance. Schedule 1 controlled substances have a “high abuse potential with no accepted medical use,” and they cannot be “prescribed, dispensed, or administered.” Because cannabis remains classified as a Schedule 1 controlled substance, the CSA “imposes strict controls on possession, manufacturing, distribution, and dispensing” of cannabis.

Under the Money Laundering Control Act of 1986 (MLCA) and the BSA as amended, covered banks and NBFIs are prohibited from providing financial services to businesses that are engaged in illicit activities. Because federal law prohibits the distribution and sale of cannabis, financial transactions involving CRBs are therefore deemed to be transactions that involve funds derived from illegal activities.

As of Feb. 3, 2022, 18 states, two territories, and the District of Columbia have enacted legislation to regulate cannabis for adult use. Thirty-seven states, the District of Columbia and four territories have approved comprehensive, publicly available medical and cannabis programs. Eleven states allow for the use of low-THC, high-CBD substances for medical reasons in limited situations or as a legal defense.

The growing divide between federal prohibition and state legalization of the cannabis industry creates a precarious position for federally regulated banks and NBFIs with the main concern involving exposure to legal, operational and regulatory risk. The situation begs the question: How might the federal government and regulators pursue and prosecute players in the legal cannabis industry?

The current economic trajectory predicts that retail sales of legal cannabis products in the U.S. will surpass an estimated $41.5 billion annually by 2025, and many banks and NBFIs are eagerly awaiting the federal green light to do business with CRBs without fear of prosecution or legal ramifications.

From 2018 forward, Congress has made several attempts to pass legislation that would protect CRBs when cultivating, distributing, marketing, and selling cannabis products in their state-legalized form. These efforts to declassify cannabis-related activity as a specified unlawful activity have thus far been unsuccessful.

The House passing the MORE Act back in 2020

Passage of the Secure and Fair Enforcement Banking Act of 2021 (SAFE Banking Act) and the Marijuana Opportunity Reinvestment and Expungement Act of 2021 (MORE Act) would enable banks and NBFIs to provide financial services to CRBs. The SAFE Banking Act would provide a safe harbor for banks and NBFIs that provide financial services to CRBs. The MORE Act would deschedule cannabis from the CSA entirely.

Questions to ask

Banks and NBFIs interested in providing financial services to CRBs should ask these questions:

Do we adequately understand our risk, and what are the implications for our organization? How should we augment our risk assessment process and our controls?

To what extent are we willing to accept the risk of banking CRBs? Do we have the ability to identify CRB customers, and if so, do we have any?

How should we advise the board of directors about setting risk appetite?

What customer due diligence (CDD) and enhanced due diligence (EDD) will we need to safely continue with existing customers and onboard new ones?

How will we monitor for unusual and suspicious activity? What will be the alerting and judgmental criteria?

How will our resource needs change so that we stay abreast of new processes and controls?

Risk appetite considerations

In order to determine whether to accept or prohibit CRBs, banks and NBFIs should identify the level of acceptable risk they are willing to take on. Several key components need to be considered, such as:

The board of directors’ stance on legal cannabis, given that good governance recommends and regulators expect that the board sets risk appetite

Cannabis laws in states within the customer footprint and the impact on customers’ communities

Risk profile, customer base, geographic location, products, and services

Relationship with regulators and any recent deficiencies or weaknesses in the BSA and associated compliance programs

Ability to implement appropriate controls and staffing

Developing a strategic road map

If the decision is made to bank CRBs, banks and NBFIs should perform an assessment of compliance maturity for existing BSA/AML program processes and controls to identify potential gaps and develop a strategic road map that helps the organization achieve its vision for future state compliance and sustainable operations.

A well-developed and well-articulated strategic road map visualizes what actions or key outcomes are needed to help organizations achieve their long-term goals. When creating the road map, banks and NBFIs need to demonstrate a keen understanding of their desired strategy, outcomes, markets, and products for onboarding and banking CRB customers. Specifically, banks and NBFIs need to define and explain how desired outcomes and business strategies create risk and exposure.

In addition to a road map, banks and NBFIs should develop and document a detailed risk-based approach that is aligned to the organization’s risk tolerance to determine necessary compliance steps when banking CRB customers.

Specifically, the following activities should be considered when developing a CRB banking program that meets regulatory expectations:

Identifying BSA/AML control gaps related to CRB risk identification and mitigation and formulating a plan to address them

Updating a board-approved policy framework

Updating detailed operating policies and procedures

Planning for capacity, developing job descriptions, and onboarding new personnel

Training for all three lines of defense, senior management, and the board

Developing and documenting a phased or full approach to acceptance of CRB customers

Developing and documenting a CRB program oversight policy

This framework is intended to help banks and NBFIs differentiate types of CRBs and their corresponding risks, and it separates CRBs into three tiers and details risks for each tier. The following exhibit summarizes the approach:

Risk framework by tier

Level

Risk

Tier 1

Direct

Tier 2

Indirect with substantial revenue from Tier 1

Tier 3

Indirect with incidental revenue from Tier 1

Source: CRB Monitor

Even the most conservative of risk appetites equivalent to outright prohibition is not devoid of significant risk considerations. Residual risk frequently encompasses a large number of indirect connections in the total CRB ecosystem. Common examples are printers, lawyers, accountants, landlords, and even utilities and taxing authorities, and all of these are subject to regulatory scrutiny and, importantly, visibility to law enforcement. Also, policies to prohibit or restrict will be audited and examined for compliance, and exceptions will require explanations.

This panorama necessitates expertise and prudence in identifying and evaluating risks within the many layers of CRBs. For example, consider a bank or NBFI that banks a CRB’s employee or vendor. If a bank fails to properly implement controls that would allow it to identify and mitigate risk associated with banking CRBs, it will be susceptible to severe violations of the BSA, including civil money penalties, criminal penalties, and regulatory enforcement actions.

Implementing necessary precautions

A well-developed road map should consider and implement the following activities:

Understanding the most current state and federal cannabis laws and regulations to ensure the bank or NBFI’s compliance

Understanding the local, state, or tribal program to ensure CRB customers are compliant with the program

Implementing a CRB risk assessment

Implementing executive approval practices for direct CRBs

Developing adequate risk ratings (possibly through a risk-based, tiered approach) and corresponding monitoring for CRB customers that includes:

Integrating various customer onboarding and AML solutions at both onboarding and periodic levels

Scheduling regular reviews to include recurring enhanced due diligence, site visits, and transaction monitoring

Monitoring for suspicious activity, including red flags, via open sources for adverse information about the CRB customers and related parties such as beneficial owners

Performing adequate CDD and EDD that will validate that the CRB-offered products, services, and programs are compliant with most current state laws and regulations by:

Collecting appropriate documentation as evidence of compliance, perhaps including a comprehensive onboarding questionnaire, beneficial ownership information, and contracts for the growing, harvesting, transporting and processing of the product

Reviewing applications and supporting documentation used to obtain a legal cannabis state license

Understanding the normal and expected activity of the organization’s CRB customers and their product usage

Developing adequate training programs and governance and oversight programs to address this customer type by:

Updating existing policies and procedures to review inherent risk presented by banking CRB customers

Updating annual training for employees

Auditing initial program design and periodic operational effectiveness

Moving forward cautiously

The ins, outs, and unknowns of cannabis banking are complex, and they require banks and NBFIs to be extremely vigilant with current policy and aware of new developments. Overall, the idea of creating a cannabis program might seem like a daunting task, but with appropriate guidance and care, organizations can provide services in compliance with laws and regulations.

Crowe disclaimer: Qualified organizations only. Independence and regulatory restrictions may apply. Some firm services may not be available to all clients. Given the continued evolution and inconsistency of various state and federal cannabis-related laws, any company should seek competent legal advice relating to its involvement in the cannabis industry, including when considering a potential public offering as a cannabis-related company.

Federal regulations have made compliant credit processing in the cannabis industry difficult to achieve. As a result, most cannabis retailers operate a cash-only model, limiting their ability to upsell customers and placing a burden on customers who might rather use credit. While some dispensaries offer debit, credit or cashless ATM transactions, regulators and traditional payment processors have been cracking down on these offerings as they are often non-compliant with regulations and policies.

Two companies, KindTap Technologies and Aeropay, are addressing the cannabis industry’s payment processing challenges with innovative digital solutions geared towards retailers and consumers.

We interviewed both Cathy Corby Iannuzzelli, president at KindTap Technologies and Daniel Muller, CEO at Aeropay. Cathy co-founded KindTap in 2019 after a career in the banking and payments industries where she launched multiple financial and credit products. Daniel founded AeroPay in 2017 after a career in digital product innovation, most recently at GPShopper (acquired by Financial), where he oversaw the design and development of over 300 web and mobile applications for large scale Fortune 500 companies.

Green: What is the biggest challenge your customers are facing?

Cathy Corby Iannuzzelli, co-founder and president at KindTap Technologies

Iannuzzelli: Our customers include both cannabis retailers and their end consumers. As long as cannabis is illegal at the federal level, normal payment solutions such as debit and credit cards cannot be accepted for cannabis purchases. This has resulted in heavy cash-based sales and unstable, transient work-around ATM payment solutions that can be ripped out with little notice, disrupting the entire business. The lack of a mature payment network to support retail payments for cannabis purchases is a huge challenge for all stakeholders. Cannabis retailers bear the high cost and safety issues of operating a heavily cash-based retail business. Consumers encounter several friction points that require them to change their behavior when purchasing cannabis relative to how they purchase everything else.

Muller: Our cannabis business customers have faced a constantly changing and, frankly, exhausting financial services environment. From the need to move and manage large amounts of cash, to card workarounds, added to the disappointment from legislation around the SAFE Banking Act, these inconsistencies have acted as a roadblock to their potential growth and profitability. Aeropay is in the position to be a stable, long-term, reliable payments partner ready to help them scale their businesses. We believe these opportunities are limitless.

Green: What geographies have got your attention and why?

Daniel Muller, CEO and founder of Aeropay

Iannuzzelli: KindTap’s focus is on the U.S. market where federal policy has created the need for alternatives to traditional payment networks. KindTap is available in every U.S. state where cannabis is legally sold. In terms of our distribution channels, KindTap’s digital payment solution was brought to market during the COVID-19 pandemic when curbside pick-up and delivery became critically important. These channels are where the exchange of cash at pick-up posed the greatest security risk to employees and customers. Our early integrations were with e-commerce platforms focused on delivery and pick-up orders, and our integration partners have strong customer bases in California and the northeast. So, while KindTap can provide its “Pay Later” lines of credit and “Pay Now” bank account solutions anywhere, we have heavier penetration in those regions.

Muller: California, for its established tech culture and how it plays into the cannabis industry – your product simply has to live up to their tech standards to be heard. Also, Chicago, our headquarters, with its newly emerged commitment to financing the cannabis industry and bringing with it a more traditional business approach. In Chicago, you have to have elevated standards of professional practices in any industry you enter. And of course, we love to watch emerging markets like New York and Florida as they head towards adult-use and what shape cannabis and payments will take.

Green: What are the broader industry trends you are following?

Iannuzzelli: We continue to see a strong transition from cash and ATM transactions over to digital payments. Since KindTap has a fully-integrated payment “button” on e-commerce checkout screens, the adoption rate of end consumers to that one-click experience is quite strong. We are also seeing trends of more “express lines” in the retail environment – for those KindTap users who paid online/ahead – and faster/safer delivery experiences to people’s homes since there is no longer the need to collect any payment upon delivery. We are firm believers in the delivery/digital payments combination and a strong increase of that trend as more states allow for delivery.

Muller: The cannabis industry is starting to normalize payments and mirror traditional online and brick-and-mortar. With bank-to-bank (ACH) payments, cannabis businesses can now offer modern customer shopping experiences including pre-payment for delivery orders without the need for a cash exchange at the door, offering the option to buy online pickup in-store and contactless in-store QR scan-to-pay customer experiences. With these familiar and customer-driven options now available, we are seeing widespread adoption, as well as meaningful increases in spend and returning customers.

Green: Thank you both. That concludes the interview!

About KindTap: KindTap Technologies, LLC operates a financial technology platform that offers credit and loyalty-enabled payment solutions for highly-regulated industries typically driven by cash and ATM-based transactions. KindTap offers payment processing and related consumer applications for e-commerce and brick-and-mortar retailers. Founded in 2019, the company is backed by KreditForce LLC plus several strategic investors, with debt capital provided by U.S.-based institutions. Learn more at kindtaptech.com.

About AeroPay: AeroPay is a financial technology company reimagining the way money is moved in exchange for goods and services. Frustrated with the current, antiquated payments landscape, we believe there is a better way to pay and a better way to get paid. AeroPay set out to build a payments platform that works for all- businesses, consumers, and their communities. Learn more at aeropay.com.

The cannabis industry is approaching a crossroads. While cultivators must ensure they are getting the greatest yield per square foot, an increasingly competitive landscape and sophisticated consumer means growers must also balance the need for volume with quality, consistent and award-winning cannabis strains.

Tissue culture propagation represents a significant leap forward in cannabis cultivation, ultimately benefiting both the grower and the consumer. The proprietary technology behind our sterilization and storage process results in the isolation of premium cannabis genetics in a clean, contaminant-free environment. Since our inception, we’ve been focused on setting a higher standard in medical (and one day adult use) cannabis by growing craft cannabis on a commercial scale through utilization of this cutting-edge cultivation technique. When taken in total, Maitri boasts access to a library of 243 unique cannabis strains, one of the largest collections in the U.S.

Trouble with Traditional Cultivation

Pathogens, insects and cross contamination all threaten the viability and value of cannabis plants. In many ways, current cannabis cultivation techniques compound these issues by promoting grams per square foot above all else and packing plants into warehouse sized grows where issues can quickly spread.

In these close quarters, pests can swiftly move from plant to plant, and even from generation to generation when propagating from clones or growing in close quarters. Similarly, pathogens can leap between susceptible plants, damaging or killing plants and cutting into a cultivator’s bottom line.

Hemp tissue culture samples

Of particular concern is hop latent viroid. Originally identified in hops, a genetic relative of cannabis, this infectious RNA virus has torn through the cannabis industry, endangering genetics, causing sickly plants and reducing yields. Plants cloned using traditional methods from an infected mother are vulnerable to the disease, making hop latent viroid a generational issue.

Minimizing or even eliminating these threats helps to protect the genetic integrity of cannabis strains and ensures they can be enjoyed for years to come. That is where the sterilization stage in tissue culture cultivation stands out.

Like cloning, tissue culture propagation offers faster time to maturity than growing from seed, allowing for a quicker turnaround to maximize utility of space, without overcrowding grow rooms. However, it also boasts a clean, disease-free environment that allows plants to thrive.

Tissue Culture Cultivation

Tissue culture cultivation allows for viable plant tissue to be isolated in a controlled, sterilized environment. Flowering plants can then be grown from these stored genetics, allowing for standardization of quality strains that are free of contamination and disease from the very beginning. Tissue culture cultivation also takes up less room than traditional cloning, freeing up valuable square footage.

A large tissue culture facility run in the Sacramento area that produces millions of nut and fruit trees clones a year.

This propagation process begins with plants grown to just before flowering and harvested for their branch tips. These branch tips undergo a sterilization process to remove any environmental contamination. This living plant material (known as explants) gets fully screened and tested for potential contaminants.

If it passes, the sample is stabilized and becomes part of the Maitri genetic library for future cultivation. If any contamination is discovered, the plant is selected for meristem isolation, an intensive isolation technique at the near cellular level.

Once sterilized and verified to be clean, the samples — often just an inch tall — are isolated into individual test tubes in our proprietary nutrient-rich medium for storage indefinitely. The cuttings are held in these ideal conditions until tapped for cultivation. This process allows Maitri to maintain an extensive library of clean, disease-free cannabis genetics ready to be grown.

Benefits for Medical Cannabis Patients

Tissue culture creates exact genetic replicas of the source plant

One of the chief benefits of tissue culture propagation is that it creates exact genetic replicas of the source plant. This allows growers like Maitri to standardize cannabis plants, and thus the cannabis experience. That means patients can expect the same characteristics from Maitri grown strains every time, including effects, potency and even taste and smell. Keeping reliable, top quality strains in steady rotation ensures patients have access to the medicine they need.

Preserving Plant Genetics

Beyond the benefits that tissue culture cultivation provides for the patient, this approach to testing, storing and growing cannabis plants also goes a long way towards protecting cannabis genetics into the future.

Cannabis strains are constantly under assault from pests and disease, potentially destroying the genetics that make these strains so special. Over-breeding and a dwindling demand for heirloom strains also threatens the loss of some individual plant genetics. Having a collection of genetics readily available means we can quickly cultivate strains to best meet consumer demand. Additionally, maintaining a rich seed bank that features both legacy and boutique strains allows us to have options for future tissue culture cultivation or for future new strain development.

Advancing Cannabis Research

Due to federal prohibition, researching cannabis, especially at the university level, can be extremely difficult. Additionally, the cannabis material that researchers have access to is largely considered to be subpar and wildly inconsistent, placing another barrier to researching the physiological effects of the plant. Clean, safe and uniform cannabis is a necessity to generate reliable research data. Utilizing tissue culture cultivation is a smart way to ensure researchers have access to the resources they need to drive our understanding of the cannabis plant.

This website uses cookies so that we can provide you with the best user experience possible. Cookie information is stored in your browser and performs functions such as recognising you when you return to our website and helping our team to understand which sections of the website you find most interesting and useful.

Strictly Necessary Cookies

Strictly Necessary Cookie should be enabled at all times so that we can save your preferences for cookie settings.

We use tracking pixels that set your arrival time at our website, this is used as part of our anti-spam and security measures. Disabling this tracking pixel would disable some of our security measures, and is therefore considered necessary for the safe operation of the website. This tracking pixel is cleared from your system when you delete files in your history.

We also use cookies to store your preferences regarding the setting of 3rd Party Cookies.

If you disable this cookie, we will not be able to save your preferences. This means that every time you visit this website you will need to enable or disable cookies again.

Federal anti-money laundering laws and related record-keeping regulations, such as the Bank Secrecy Act (BSA), have presented complex compliance protocols that prevent banks from meeting the business needs of local growers, manufacturers and dispensaries. Local cannabis business owners are therefore put in a difficult position, as they must balance daily business activity against the potential dangers of operating as a cash-only business.

Federal anti-money laundering laws and related record-keeping regulations, such as the Bank Secrecy Act (BSA), have presented complex compliance protocols that prevent banks from meeting the business needs of local growers, manufacturers and dispensaries. Local cannabis business owners are therefore put in a difficult position, as they must balance daily business activity against the potential dangers of operating as a cash-only business. Policymakers may need to introduce the Act as a stand-alone bill that outlines clear objectives and specifically addresses the issue from a public safety perspective. Cannabis is a hot-button issue, so adding additional legislation will muddy the water and make it easier for Senate members on the fence to vote against the bill.

Policymakers may need to introduce the Act as a stand-alone bill that outlines clear objectives and specifically addresses the issue from a public safety perspective. Cannabis is a hot-button issue, so adding additional legislation will muddy the water and make it easier for Senate members on the fence to vote against the bill.